TL;DR:

- Responding to a foreclosure summons in Florida within 20 days is crucial to protect your legal rights and defenses. Failure to answer results in a default judgment that speeds up foreclosure and limits your options, including contesting claims and negotiating with the lender. Filing a timely response forces the lender to prove their case and keeps your opportunity to challenge or settle open.

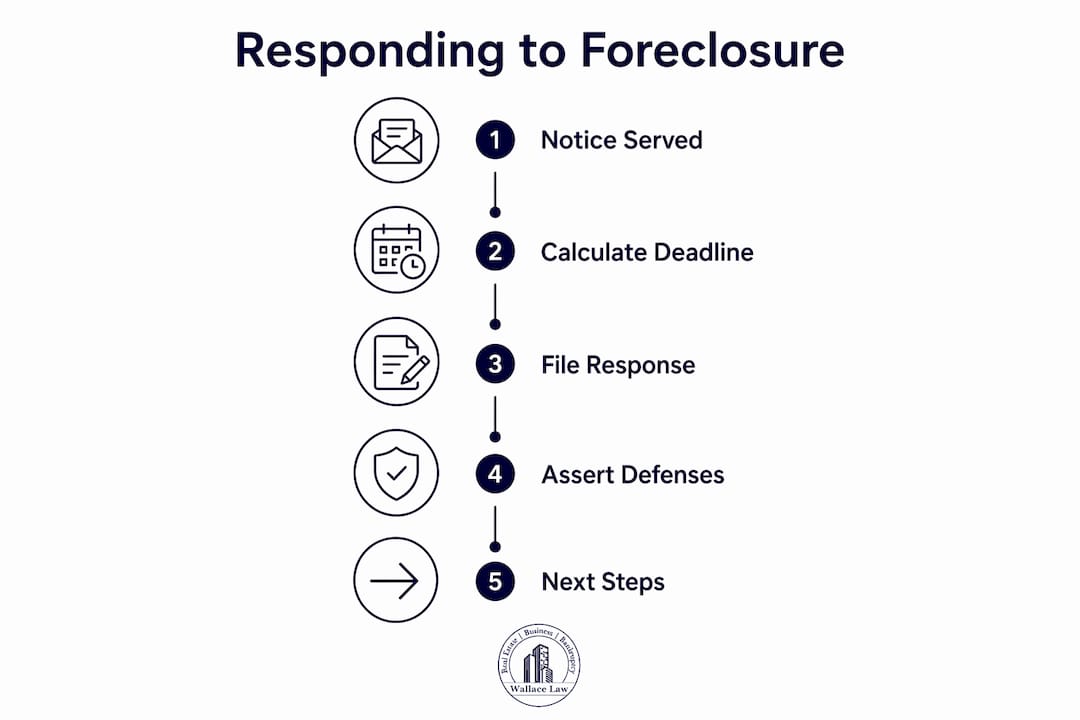

Responding to a foreclosure summons is defined as filing a formal written answer with the court to contest a lender’s claims against your home. Florida law requires homeowners to file this response within 20 calendar days of service. Missing that deadline hands the lender a default judgment, which accelerates the entire foreclosure process and strips you of every legal defense you had. Understanding why respond to foreclosure summons matters is the first step toward protecting your home and your rights.

Why respond to a foreclosure summons in Florida?

Responding to a foreclosure summons is the single most important action a Florida homeowner can take after being served. The moment you file a written answer with the Clerk of the Court, you force the lender to prove every claim in their complaint. Without your response, the court assumes the lender is right about everything.

Florida courts require a written response within 20 calendar days of service. That deadline is strict. Courts do not grant extensions simply because you were confused, overwhelmed, or waiting to hear back from your lender.

A timely response also preserves your legal rights to challenge the lender’s standing, demand documentation, and pursue loss mitigation options like loan modifications. Silence, by contrast, cedes all of that control to the lender.

What happens if you ignore a foreclosure summons in Florida?

Ignoring a foreclosure summons does not pause or delay your case. The lender gains the upper hand immediately.

The default judgment trap

When you fail to respond, the court enters a default judgment against you. A default judgment means the court treats every factual allegation in the lender’s complaint as admitted. You lose the right to dispute the debt amount, challenge mortgage fraud, question the lender’s standing, or raise any affirmative defense. The lender essentially wins without having to prove anything.

Silence in a foreclosure case is not a neutral act. It is a legal concession. The court treats your non-response as an admission of every claim the lender made, including the amount owed, the validity of the mortgage, and your default status.

Once a default judgment is entered, the foreclosure sale can be scheduled quickly. The lender can then pursue enforcement actions including eviction, wage garnishment, and lien placement, all without your input. Ignoring the summons does not make the case disappear. It makes the outcome worse and faster.

Trying to undo a default judgment

Reversing a default judgment is difficult. You must file a formal motion to vacate and prove good cause. Courts accept reasons like a documented medical crisis or military deployment. Being confused or overwhelmed does not qualify. Courts rarely grant these motions without a meritorious defense and a compelling reason for the delay. By that point, the foreclosure sale may already be scheduled.

- You lose the right to challenge the lender’s standing

- You lose the ability to demand proof of debt ownership

- You lose access to loss mitigation negotiations

- You face a faster path to eviction and property loss

- You must clear a high legal bar just to re-enter the case

How and when to respond to a foreclosure summons in Florida

Filing a proper response requires attention to deadlines, format, and procedure. Getting any of these wrong can be as damaging as not responding at all.

The 20-day deadline and how to calculate it

Florida’s 20 calendar day deadline begins on the date you are served, not the date you open the envelope or speak to an attorney. The service date counts as day zero. Day 20 is your filing deadline.

The type of service affects your timeline. Personal service, where a process server hands you the documents directly, triggers the shortest deadline. Service by mail may add a few days depending on court rules, but homeowners frequently miscalculate by ignoring the service date entirely or confusing the method. Document the exact date and method of service the moment it happens.

What your response must include

A formal answer to a foreclosure complaint addresses each allegation in the lender’s complaint one by one. For each claim, you admit it, deny it, or state that you lack sufficient knowledge to admit or deny it. Denying a claim does not mean you are lying. It means you are requiring the lender to prove it.

- Obtain a copy of the lender’s complaint and read every numbered paragraph

- Draft a written answer that responds to each paragraph individually

- Include any affirmative defenses you intend to raise

- Sign the document and make copies for your records

- File the original with the Clerk of the Court in the county where the property is located

- Serve a copy on the lender’s attorney as required by Florida court rules

Pro Tip: Never rely on a verbal promise from your lender or their attorney that they will “pause” the case while you negotiate. Negotiations with lenders do not stop the legal clock. You must still file your formal court answer before the deadline, regardless of any informal agreement.

What legal defenses can you assert when responding?

Responding to a foreclosure summons does not mean admitting the debt or accepting that you will lose your home. It means forcing the lender to prove their case. That distinction matters enormously.

Affirmative defenses in Florida foreclosure cases

An affirmative defense is a legal argument that, if proven, defeats or limits the lender’s claim even if the basic facts of the complaint are true. Responding to the summons is the mechanism that preserves your right to raise these defenses. Without a filed answer, they are waived entirely.

| Defense | Effect | Evidence Required |

|---|---|---|

| Lack of lender standing | Lender must prove they own the loan | Chain of title, assignment records |

| Failure to comply with loss mitigation | Can delay or dismiss the case | Correspondence, denial letters |

| Mortgage fraud or predatory lending | May void or restructure the loan | Loan documents, appraisal records |

| Improper service of process | Can invalidate the summons | Affidavit of service, process records |

| Statute of limitations | Bars stale claims | Loan history, payment records |

- Lack of standing is one of the most powerful defenses in Florida. Mortgages are frequently bought and sold, and lenders sometimes cannot produce a clean chain of title proving they own your loan.

- Loss mitigation failures occur when lenders do not follow federal rules requiring them to review homeowners for alternatives before foreclosing.

- Mortgage fraud covers situations where the original loan was obtained through misrepresentation or predatory terms.

Responding also opens the door to negotiation. While litigation proceeds, you can pursue a loan modification, forbearance, or short sale. The lender has more incentive to negotiate when they know you are actively contesting the case. Asserting these defenses does not guarantee you keep the home, but it buys critical time and creates real leverage.

What are the practical next steps after responding?

Filing your answer is the start of the litigation process, not the end. What you do next shapes how the case unfolds.

Pro Tip: Document every communication with your lender from the day you receive the summons. Save emails, record call dates and summaries, and keep copies of every document you file or receive. Courts and attorneys rely on this paper trail.

- Hire a foreclosure defense attorney. An experienced attorney can identify defenses you would miss on your own and manage court deadlines. Wallacelawflorida serves homeowners in Boynton Beach and surrounding South Florida communities with exactly this kind of focused representation.

- Pursue loss mitigation immediately. Contact your lender’s loss mitigation department in writing. A loan modification application, if submitted properly, can pause foreclosure proceedings under federal mortgage servicing rules.

- Understand the litigation timeline. After your answer is filed, the case enters the discovery phase. Both sides exchange documents and evidence. This process can take months, giving you time to negotiate or build your defense.

- Prepare for mediation. Florida courts often require foreclosure mediation before trial. Mediation is a structured negotiation with a neutral third party. It is one of the most common paths to a loan modification or settlement.

- Monitor all court deadlines. Missing a court deadline after filing your answer can be just as damaging as missing the original response deadline. Set calendar reminders for every filing date.

If you are also dealing with significant debt beyond the mortgage, bankruptcy options may provide an automatic stay that halts foreclosure proceedings immediately. A property division attorney, such as those at Jeff T. Gorman Law Offices, can also be relevant if marital property disputes are part of your situation.

Key Takeaways

Responding to a foreclosure summons within Florida’s 20-calendar-day deadline is the single most effective action a homeowner can take to preserve legal rights, assert defenses, and create negotiating leverage.

| Point | Details |

|---|---|

| 20-day deadline is absolute | File your written answer within 20 calendar days of service or face default judgment. |

| Silence equals admission | Courts treat every lender allegation as true if you do not respond. |

| Defenses are waived without a response | Affirmative defenses like lack of standing can only be raised if you file an answer. |

| Responding opens negotiation | Active litigation gives you leverage to pursue loan modifications or settlements. |

| Vacating default is very hard | Courts rarely reverse default judgments without proof of serious cause and a valid defense. |

What I’ve seen change when homeowners respond in time

The most common mistake I see is homeowners waiting. They receive the summons, feel paralyzed, and assume that doing nothing buys time. It does the opposite. Every day of silence is a day the lender uses to build an uncontested case.

I have seen cases where a timely response, filed with a clear denial and a standing defense, led to the lender producing incomplete documentation. That gap in their evidence became the foundation for a loan modification the homeowner had been denied twice before. The response did not win the case outright. It forced the lender to engage seriously.

The other misconception I encounter constantly is that responding means admitting you owe the debt. It does not. Filing an answer is a procedural act. It says: “I am here, I contest your claims, and you must prove them.” That posture changes the entire dynamic of the case. Lenders move faster against homeowners who do not show up.

Responding also buys time, and time in foreclosure is genuinely valuable. It gives you space to consult an attorney, gather documents, apply for loss mitigation, and understand your options. None of that is possible once a default judgment is entered. The window closes fast and reopening it is rarely successful.

— Steven

How Wallacelawflorida helps Florida homeowners facing foreclosure

Florida homeowners facing a foreclosure summons need more than general advice. They need an attorney who knows the local courts, the deadlines, and the defenses that actually work in South Florida.

Wallacelawflorida provides focused residential real estate legal help for homeowners in Boynton Beach and surrounding communities. The firm’s attorneys understand Florida’s strict foreclosure timelines and have guided clients through contested foreclosure cases, loan modification negotiations, and court filings. If you have received a summons, the time to act is now. Contact Wallacelawflorida to schedule a consultation and get a clear picture of your options before the deadline passes.

FAQ

What is the deadline to respond to a foreclosure summons in Florida?

Florida homeowners must file a written response within 20 calendar days of the date of service. Missing this deadline allows the lender to seek a default judgment.

What happens if I ignore a foreclosure summons?

The court enters a default judgment, treating every lender allegation as true. This accelerates the foreclosure and removes your right to raise any defense.

Does responding to a summons mean I admit the debt?

No. Responding to the summons compels the lender to prove their claims and preserves your right to raise affirmative defenses. It is not an admission of anything.

Can I negotiate with my lender instead of filing a court response?

Negotiations with your lender do not pause the legal deadline. You must still file a formal court answer within 20 days, even if you are actively discussing a loan modification.

Can I reverse a default judgment if I missed the deadline?

You can file a motion to vacate, but courts require proof of serious cause such as a medical emergency or improper service. Being confused or unprepared does not qualify, and courts rarely grant these motions.