If you’ve missed a mortgage payment and fear losing your home, understanding what is foreclosure process Florida involves can be the difference between panic and a plan. Florida led the nation in new foreclosure starts in April 2026 with 3,505 filings, meaning you are far from alone in this situation. The good news is that Florida law actually gives homeowners more time and more legal protections than most people realize. This guide walks you through every stage of the process, your rights at each step, and what you can do right now to protect your home.

Table of Contents

- Key Takeaways

- What is the foreclosure process in Florida, step by step

- Your legal rights during Florida foreclosure

- Factors that can speed up or delay your timeline

- Practical steps to take right now

- My honest take after years of watching homeowners navigate this

- How Wallacelawflorida can help you protect your home

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Florida requires a lawsuit | Every foreclosure must go through circuit court, giving you time and legal rights to respond. |

| 120-day federal buffer | Lenders cannot file a foreclosure lawsuit until you are at least 120 days behind on payments. |

| You have 20 days to respond | After being served, you have 20 days to file a legal response and avoid a default judgment. |

| No redemption after auction | Once the property sells at auction, you cannot buy it back, making early action critical. |

| Multiple alternatives exist | Loan modification, short sale, deed in lieu, and bankruptcy can all stop or delay foreclosure. |

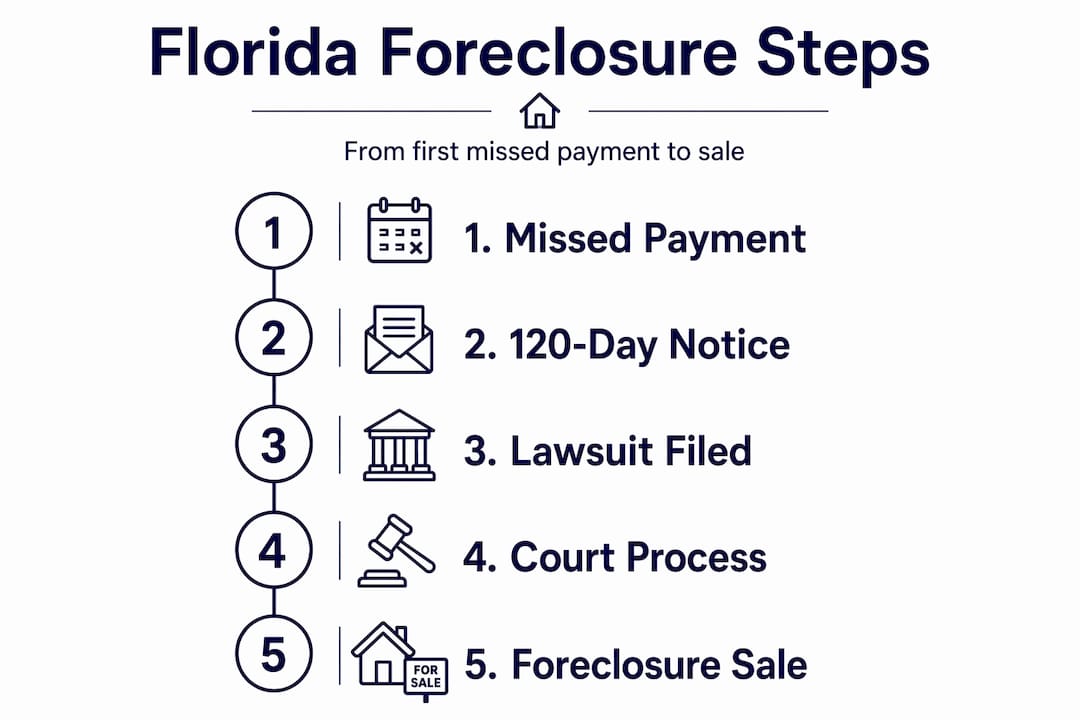

What is the foreclosure process in Florida, step by step

Florida is a judicial foreclosure state. That means your lender cannot simply take your home. They must file a lawsuit, go through the court system, and get a judge’s approval before any sale can happen. That legal requirement is actually your greatest protection.

Here is how the foreclosure timeline stages explained in order:

- Missed payments begin. The clock starts when you stop making mortgage payments. Most lenders will not take legal action after just one missed payment. They typically wait until you are significantly behind before moving forward.

- 120-day federal waiting period. Under federal RESPA regulations, lenders cannot file a foreclosure lawsuit until you are at least 120 days delinquent. During this window, your servicer is legally required to explore loss mitigation options with you. This is your best window to negotiate.

- Lender files a complaint. Once the 120-day period passes without resolution, the lender files a foreclosure complaint in circuit court. At the same time, a lis pendens is recorded in the public records. This document alerts the world that your property is involved in active litigation.

- You are served with a summons. A process server delivers the lawsuit documents to you. From the date you are served, you have 20 days to respond to the complaint in writing.

- Response or default. If you respond, the case moves into active litigation. If you do not respond, the lender can request a default judgment, which speeds the entire process up significantly and removes most of your options.

- Court proceedings. The judge reviews the case. In an uncontested case, the typical timeline runs 6 to 18 months. A contested case, where you actively fight the foreclosure, can extend to 18 to 36 months or longer.

- Final judgment and auction scheduling. If the court rules in the lender’s favor, a final judgment is entered. The auction is then scheduled 20 to 35 days after that judgment.

- Foreclosure auction. The property is sold at a public auction, usually through an online bidding platform. Florida has no post-sale redemption period, meaning once the gavel falls, the sale is final.

Pro Tip: The 120-day pre-foreclosure period is not dead time. Use it immediately to call your servicer, request a loss mitigation application, and gather your financial documents. This window closes faster than most homeowners expect.

Your legal rights during Florida foreclosure

Understanding how judicial foreclosure works in Florida means understanding that the court process is not just a formality. It is a genuine legal proceeding where you have real rights.

- Right to notice and response. You must be properly served with the complaint. You have the right to respond, raise defenses, and contest the lender’s claims in court.

- Homestead protections. Florida’s homestead exemption is strong against unsecured creditors like credit card companies. However, it does not protect you from a mortgage foreclosure because the lender holds a lien directly on the property.

- Lis pendens impact. Once recorded, the lis pendens clouds your title. You cannot refinance or sell the property cleanly until the litigation is resolved. Buyers and new lenders will see it immediately in a title search.

- Deficiency judgment risk. If the auction sale price does not cover your full loan balance, the lender may pursue a deficiency judgment against you personally. Florida law gives lenders one year after the sale to file for a deficiency.

- Loss mitigation rights. Federal law requires your servicer to evaluate you for all available loss mitigation options before proceeding. This includes loan modifications, forbearance plans, and repayment agreements.

- Mediation programs. Many Florida circuits offer foreclosure mediation programs where you can negotiate directly with the lender under court supervision. This can result in a loan modification or repayment plan that keeps you in your home.

Pro Tip: Even if you believe you cannot afford an attorney, many Florida legal aid organizations offer free or low-cost foreclosure defense assistance. Getting legal advice before the 20-day response deadline can fundamentally change your outcome.

Factors that can speed up or delay your timeline

Not every Florida foreclosure follows the same path. Several factors can push the process faster or slower, and knowing which applies to your situation helps you plan.

Factors that extend the timeline:

- Actively contesting the foreclosure in court can push the process past 36 months in counties with heavy court backlogs.

- Filing for bankruptcy triggers an automatic stay that immediately halts all foreclosure proceedings. A Chapter 7 bankruptcy stay typically lasts several months, while Chapter 13 allows you to propose a multi-year repayment plan to catch up on arrears and keep your home.

- Participating in mediation adds time to the process but often produces better outcomes than litigation alone.

Factors that speed up the timeline:

- Failing to respond to the complaint results in a default judgment, which can compress the entire timeline dramatically.

- Properties that are vacant or abandoned are subject to expedited foreclosure procedures under Florida law, moving much faster than occupied homes.

- Lenders can request summary judgment hearings when there are no genuine factual disputes, shortening the court phase.

| Scenario | Estimated Timeline |

|---|---|

| Uncontested foreclosure | 6 to 18 months |

| Contested foreclosure | 18 to 36+ months |

| Default judgment (no response) | As fast as 3 to 6 months |

| Bankruptcy Chapter 13 filed | Pause plus 3 to 5 year plan |

| Vacant/abandoned property | Expedited, often under 6 months |

One factor many homeowners overlook is the financial stacking effect. Rising insurance premiums, property taxes, and HOA fees are pushing Florida homeowners into foreclosure even when they originally qualified for their loans comfortably. Pandemic-era buyers in particular are facing homes worth less than their purchase price while carrying dramatically higher monthly costs. Recognizing this pattern early, before you are 120 days behind, is the key to preserving your options.

Practical steps to take right now

If you are facing foreclosure or worried it is coming, the steps you take in the next few weeks matter more than anything else. Florida’s judicial process gives you time, but only if you use it.

- Call your servicer today. Ask specifically about forbearance, repayment plans, and loan modification programs. Get any offer in writing before agreeing to anything.

- Respond to every legal notice. Missing the 20-day response deadline after being served is one of the most damaging mistakes homeowners make. Even a basic response preserves your rights and buys time.

- Explore a short sale. If you owe more than the home is worth, a short sale lets you sell for less than the balance owed with lender approval. It avoids foreclosure on your credit record and eliminates most deficiency risk.

- Consider a deed in lieu. You voluntarily transfer the property to the lender in exchange for release from the mortgage debt. This avoids the public auction and can be negotiated to waive deficiency.

- Look at bankruptcy options. Chapter 13 in particular is designed to help homeowners catch up on missed mortgage payments over time. Understanding your foreclosure defense bankruptcy options early gives you the most flexibility.

- Sell before the auction. You retain the right to sell your property after the lis pendens is recorded, right up until the auction date. A cash sale can stop foreclosure by paying the lender in full and releasing the lis pendens.

- Get legal representation. An attorney who knows Florida foreclosure laws can identify procedural defects in the lender’s case, negotiate with the servicer on your behalf, and make sure you do not miss a single critical deadline.

My honest take after years of watching homeowners navigate this

I’ve seen the same pattern repeat itself more times than I can count. A homeowner misses a payment, gets scared, and does nothing. They assume the worst is already decided. They stop opening mail. They avoid phone calls. By the time they reach out for help, the 20-day response window has closed, a default judgment is entered, and the auction is weeks away.

What I’ve learned is that Florida’s judicial foreclosure process is genuinely designed with homeowner protections built in. The mandatory lawsuit requirement, the 120-day federal buffer, the mediation programs, the right to respond and contest. These are not technicalities. They are real opportunities. But they only work if you engage with the process instead of retreating from it.

The clients I’ve seen come out of this in the best shape are not necessarily the ones with the strongest legal cases. They are the ones who acted early, asked for help, and stayed in communication with their servicer and their attorney. The economic stress driving Florida foreclosures right now is real and widespread. You are not a failure for being in this situation. You are a homeowner who needs a plan, and the law gives you more runway than you probably think.

— Steven

How Wallacelawflorida can help you protect your home

Facing foreclosure is stressful, but you do not have to figure out Florida’s court system on your own. Wallacelawflorida has helped homeowners across Boynton Beach and South Florida understand their rights, respond to lawsuits, and find real alternatives to losing their homes.

Whether you need to understand your legal options to save your home, explore whether bankruptcy is the right move, or simply need someone to review what the lender sent you, Wallace Law provides the kind of personal, attentive service that larger firms cannot match. Their attorneys know Florida foreclosure laws from the inside and work directly with clients to identify every available defense and alternative. If you are behind on payments or have already been served, now is the time to act. Reach out to Wallace Law’s foreclosure attorneys before the deadline passes and your options narrow.

FAQ

What is the foreclosure process in Florida?

Florida requires lenders to file a lawsuit in circuit court to foreclose on a property. The process involves serving the homeowner, a court hearing, a final judgment, and then a public auction, typically taking 6 to 18 months for uncontested cases.

How long does the Florida foreclosure timeline take?

The timeline depends on whether you contest the case. Uncontested foreclosures take 6 to 18 months, while contested cases can run 18 to 36 months or longer due to court proceedings and potential mediation.

Can I stop a foreclosure after the lawsuit is filed?

Yes. You can stop or delay foreclosure by responding to the complaint, applying for a loan modification, filing for bankruptcy, completing a short sale, or selling the property before the auction date.

What happens if I don’t respond to the foreclosure complaint?

If you do not respond within 20 days of being served, the lender can request a default judgment. This removes most of your legal options and significantly accelerates the foreclosure timeline toward auction.

Does Florida have a redemption period after the foreclosure sale?

No. Florida does not have a post-sale redemption period. Once the property is sold at auction, the sale is final and you cannot reclaim the home by paying off the debt afterward.