TL;DR:

- Medical debt can be fully discharged through Chapter 7 or Chapter 13 bankruptcy, with no amount limit. Filing creates an automatic stay that stops collection efforts immediately and can protect assets using exemptions. Timing the filing after treatment ends improves the chances of a successful discharge and asset protection.

Medical debt is fully dischargeable in bankruptcy, most commonly through Chapter 7 or Chapter 13 filings, with no dollar cap on the amount eliminated. Under federal bankruptcy law, medical debt is classified as unsecured, non-priority debt, placing it in the same legal category as credit card balances and utility bills. The moment you file, the automatic stay under 11 U.S.C. 362 activates, immediately halting collection calls, lawsuits, and wage garnishments. This medical debt bankruptcy discharge guide walks you through every step, from choosing the right chapter to protecting your assets and timing your filing correctly.

What types of bankruptcy eliminate medical debt?

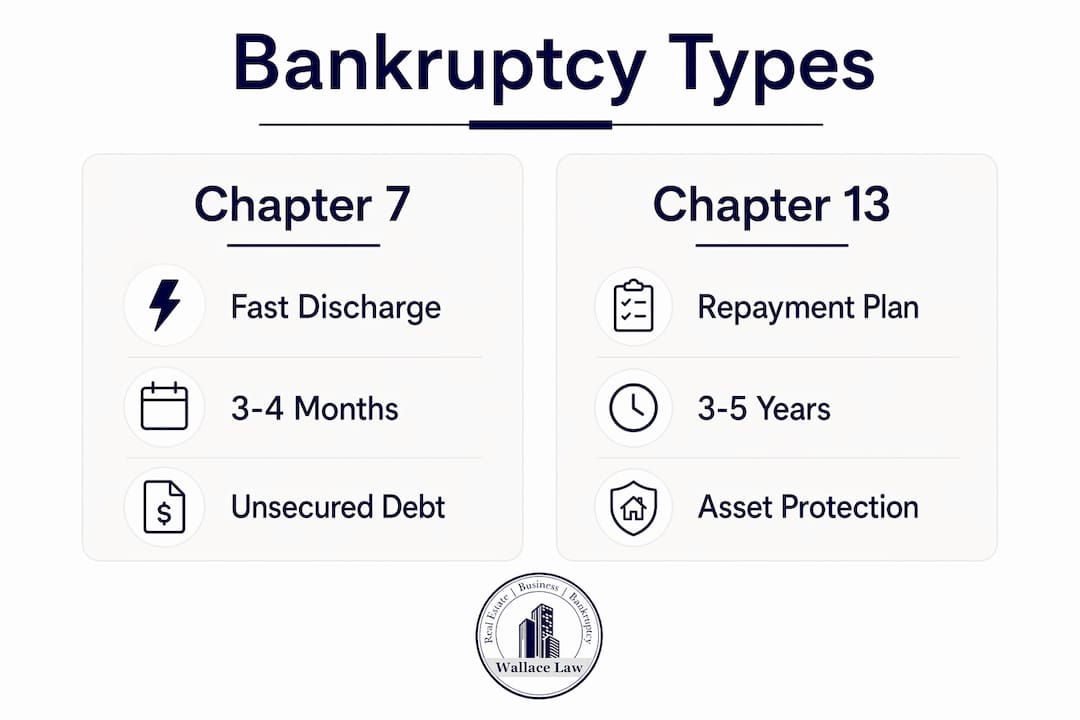

Chapter 7 and Chapter 13 are the two bankruptcy chapters available to individuals seeking to discharge medical bills. Each works differently, and choosing the right one depends on your income, assets, and goals.

Chapter 7 is the faster option. It eliminates medical debt in 3–4 months and wipes out qualifying unsecured debt entirely. You must pass the means test, which compares your income to the Florida median. If you own significant non-exempt assets, a trustee may liquidate them to pay creditors. For most people with primarily medical debt and limited assets, Chapter 7 is the most direct path to a fresh start.

Chapter 13 takes longer, typically 3–5 years, but offers stronger asset protection. You propose a repayment plan based on your disposable income. At the end of the plan, any remaining medical debt is discharged. This chapter suits people who earn too much to qualify for Chapter 7 or who want to keep property that would otherwise be liquidated.

One critical point: there is no separate “medical bankruptcy” chapter under U.S. law. Medical debt follows the same discharge rules as all other unsecured debt. That misconception causes many people to delay filing when they could act sooner.

| Feature | Chapter 7 | Chapter 13 |

|---|---|---|

| Timeline | 3–4 months | 3–5 years |

| Medical debt outcome | Fully discharged | Discharged after repayment plan |

| Means test required | Yes | No, but income limits apply |

| Asset risk | Non-exempt assets may be liquidated | Assets generally protected |

| Best for | Low income, limited assets | Higher income, significant assets |

Key benefits of bankruptcy for medical bills include:

- No cap on the dollar amount of medical debt discharged

- Immediate stop to wage garnishments and collection lawsuits

- Protection of exempt assets including retirement accounts

- A defined legal endpoint with a discharge order

For a deeper look at how these two chapters compare, the Chapter 7 vs. Chapter 13 breakdown from Wallacelawflorida covers qualification criteria and asset protection in detail.

How do you file for bankruptcy to discharge medical bills?

Filing bankruptcy to discharge medical debt follows a clear sequence. Skipping steps or filing out of order creates delays and can jeopardize your case.

-

Gather all medical bills and request itemized statements. Contact every provider and get a line-by-line breakdown of charges. Medical billing errors appear in most hospital statements, and disputing incorrect charges can reduce your total debt before you even file.

-

Negotiate or apply for financial assistance. Before filing, contact providers about payment plans or charity care. Most nonprofit hospitals are required to offer financial assistance programs, and qualifying can eliminate a portion of your debt outright.

-

Complete mandatory credit counseling. Federal law requires you to complete an approved credit counseling course within 180 days before filing. Keep your completion certificate. You will need it.

-

Choose Chapter 7 or Chapter 13 based on eligibility. Run the means test for Chapter 7. If you do not qualify, or if you have assets you want to protect, Chapter 13 is your path. Consulting a bankruptcy attorney at this stage prevents costly mistakes.

-

File your bankruptcy petition listing all debts. Your petition must include every creditor, including all medical providers. Omitting a creditor can leave that debt non-discharged.

-

Attend the 341 meeting of creditors. This is a short hearing where the trustee asks questions about your finances. Medical creditors rarely appear. Answer honestly and bring your identification and Social Security card.

-

Receive your discharge order. In Chapter 7, this arrives roughly 60 days after the 341 meeting. In Chapter 13, it comes after you complete your repayment plan.

Pro Tip: If a wage garnishment is imminent, you can file a skeleton petition with just the basic paperwork and your credit counseling certificate. This triggers the automatic stay immediately and buys you time to complete the full filing.

How to protect assets and time your bankruptcy filing

Timing your bankruptcy filing correctly is one of the most overlooked factors in a successful discharge. Filing too early can leave you responsible for bills not yet issued. Filing too late can mean losing assets you could have protected.

The single most important timing rule: file after your treatment ends to capture all medical debt in one case. Any charges incurred after your filing date are your responsibility and cannot be discharged in the same case.

Common exemptions that protect assets in Florida bankruptcy cases include:

- Homestead exemption: Florida’s homestead exemption is among the strongest in the country, protecting your primary residence with no dollar cap in most cases.

- Retirement accounts: 401(k), IRA, and pension accounts are generally fully exempt under federal and Florida law.

- Vehicle exemption: Florida protects up to $1,000 in vehicle equity, with higher protection available under the wildcard exemption.

- Wages: A portion of earned wages may be exempt from garnishment even outside bankruptcy.

For a full breakdown of what you can keep, Wallacelawflorida’s guide on assets protected during bankruptcy covers Florida-specific exemptions in detail.

Filing a skeleton petition can immediately stop wage garnishments or property sales with minimal upfront paperwork. Submitting the basic petition with your credit counseling certificate triggers the automatic stay, giving you time to complete the full filing without losing income or property.

Liens placed by medical creditors on your property are a separate concern. In some cases, you can file a motion to avoid a lien that impairs an exempt asset, effectively stripping the lien through the bankruptcy process. This is a technical step that requires legal guidance but can protect your home or other exempt property from creditor claims.

What alternatives should you consider before filing bankruptcy?

Bankruptcy is a last resort after exhausting other relief options. Attorneys consistently recommend working through these alternatives first, both to reduce debt and to strengthen your position if you do eventually file.

Practical alternatives to bankruptcy for medical bills include:

- Negotiate directly with providers. Hospitals and clinics frequently accept lump-sum settlements below the full balance. Debt settlement options often accept 50%–70% of the original balance, but typically require you to be behind on payments and owe at least $5,000–$10,000.

- Apply for hospital charity care. Nonprofit hospitals are required to offer financial assistance. Eligibility is usually income-based. Apply early, before the account goes to collections.

- Hire a medical billing advocate. These professionals review your statements for errors, negotiate on your behalf, and often recover significant reductions. Given how frequently billing errors appear, this step alone can cut your balance substantially.

- Understand your judgment-proof status. If your income is below the garnishment threshold and you own no significant assets, creditors may be unable to collect from you regardless of the debt amount. Filing bankruptcy in this situation may not be necessary.

- Check the statute of limitations. Medical debt has a statute of limitations that varies by state. Once it expires, creditors cannot sue to collect. Knowing this timeline affects whether bankruptcy is worth pursuing.

Pro Tip: Before filing, request a free consultation with a nonprofit credit counseling agency approved by the U.S. Trustee Program. They can assess whether a debt management plan or direct negotiation resolves your medical debt without the long-term credit impact of bankruptcy.

For a structured look at non-bankruptcy paths, Wallacelawflorida’s resource on debt relief alternatives outlines options that work alongside or instead of bankruptcy. You can also find broader debt relief strategies through resources like crushing debt without bankruptcy that complement the legal options covered here.

Common challenges when discharging medical debt in bankruptcy

Several issues catch filers off guard. Knowing them in advance prevents costly surprises.

- Post-filing medical bills are not dischargeable. Any treatment you receive after your filing date creates new debt. That debt is entirely your responsibility.

- Wage garnishments stop immediately, but past garnishments are not refunded. The automatic stay halts garnishments the moment you file. Wages already taken before filing are typically not recoverable.

- Bankruptcy stays on your credit report for 7–10 years. Chapter 7 remains for 10 years; Chapter 13 for 7 years. Credit recovery is possible within that window with consistent, responsible financial behavior.

- Emergency rooms cannot deny you treatment. Federal law requires emergency rooms to provide care regardless of past bankruptcy. Private practices can decline non-emergency appointments, though many accept upfront payment arrangements.

- Liens require separate legal action. A judgment lien from a medical creditor does not automatically disappear with discharge. You must file a motion to avoid the lien if it impairs exempt property.

Credit recovery after bankruptcy moves faster than most people expect. Financial counselors note that with proper planning, many filers rebuild their credit scores significantly within two to three years of discharge.

Key Takeaways

Discharging medical debt through bankruptcy requires choosing the right chapter, timing your filing after treatment ends, and exhausting alternatives like charity care and negotiation before you file.

| Point | Details |

|---|---|

| Medical debt is fully dischargeable | Chapter 7 and Chapter 13 both eliminate medical bills with no dollar cap. |

| Timing your filing matters | File after all treatment ends to capture every bill in a single case. |

| Automatic stay protects you immediately | Collection calls, lawsuits, and garnishments stop the moment you file. |

| Alternatives come first | Charity care, negotiation, and billing advocacy can reduce debt without bankruptcy. |

| Credit recovery is realistic | Chapter 13 leaves your report in 7 years; disciplined behavior speeds rebuilding. |

What I’ve learned after years of medical bankruptcy cases

The clients who get the best outcomes from medical debt bankruptcy share one trait: they consult an attorney before they do anything else. Not after they’ve already tried to negotiate, not after a garnishment starts, and not after they’ve filed on their own using an online form. Before.

The reason is timing. Filing too early, while you’re still in active treatment, is one of the most common and costly mistakes I see. You discharge what exists today, then spend the next year accumulating new bills that are entirely your responsibility. The financial relief you expected turns into a new debt cycle. Filing after treatment ends, with every bill documented, is the move that actually works.

I also want to be direct about credit. Yes, bankruptcy stays on your report for 7–10 years. But the people I’ve worked with who commit to rebuilding, opening a secured credit card, paying every bill on time, keeping balances low, often see meaningful credit score improvement within two to three years. The bankruptcy is visible on paper, but lenders look at the full picture. A clean record after discharge carries real weight.

My honest advice: exhaust every alternative first. Apply for charity care. Dispute billing errors. Try negotiating a settlement. If none of those options resolve the debt, and the amount is large enough to justify the process, bankruptcy is a legitimate, legal tool designed exactly for this situation. Use the bankruptcy attorney consultation guide from Wallacelawflorida to prepare for your first meeting. Walking in prepared makes the entire process faster and less stressful.

— Steven

How Wallacelawflorida helps with medical debt bankruptcy

Wallacelawflorida handles Chapter 7 and Chapter 13 bankruptcy filings for individuals in Boynton Beach and throughout South Florida. The firm’s attorneys understand Florida-specific exemptions, emergency filing procedures, and lien avoidance strategies that protect your assets while eliminating medical debt.

If you are facing wage garnishment, mounting hospital bills, or uncertainty about which chapter fits your situation, Wallacelawflorida offers personalized consultations to evaluate your options. The attorneys work directly with each client, not through paralegals or intake staff, so you get clear answers from experienced legal counsel. Visit the bankruptcy practice area to learn about available services or to schedule a consultation. You can also download the free Florida bankruptcy eBook for a plain-language overview of the full process before your first meeting.

FAQ

Is medical debt dischargeable in bankruptcy?

Medical debt is fully dischargeable in both Chapter 7 and Chapter 13 bankruptcy, with no cap on the amount. It is classified as unsecured, non-priority debt under federal bankruptcy law.

How long does it take to discharge medical debt in bankruptcy?

Chapter 7 discharges medical debt in approximately 3–4 months from filing. Chapter 13 requires completing a 3–5 year repayment plan before the remaining balance is discharged.

Can I keep my home and car if I file bankruptcy for medical bills?

Florida’s homestead exemption protects your primary residence with no dollar cap in most cases, and retirement accounts are fully exempt. Vehicle equity protection is limited but available, and a bankruptcy attorney can identify all exemptions that apply to your situation.

What happens to medical bills incurred after I file bankruptcy?

Any medical charges you incur after your filing date are not covered by your bankruptcy case. They remain your full responsibility, which is why timing your filing after treatment ends is critical.

Will bankruptcy stop a wage garnishment for medical debt?

The automatic stay under 11 U.S.C. 362 stops wage garnishments immediately upon filing. Wages already garnished before you file are typically not recoverable, but all future garnishments halt the moment your petition is submitted.