TL;DR:

- A foreclosure auction is a public sale of a mortgaged property to recover unpaid debt after a borrower defaults. The process involves multiple legal steps, with bidding typically starting at the full loan amount and requiring cash from bidders, to finalize ownership transfer. Homeowners should understand their legal rights, potential liens, and timing options to protect their interests before the auction date.

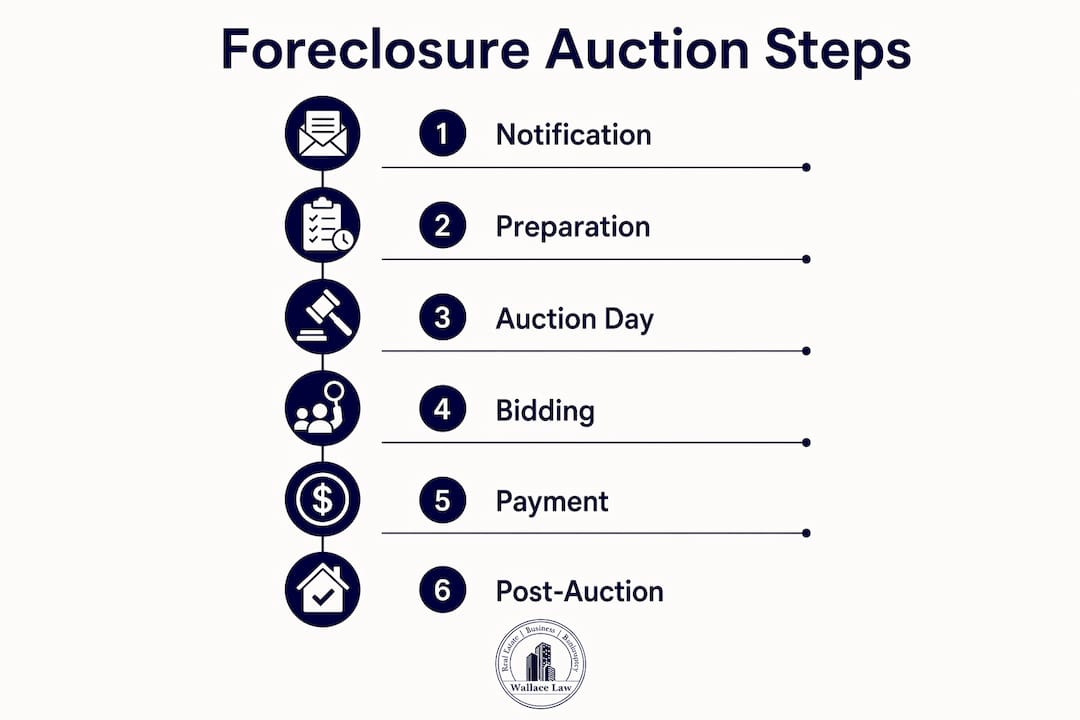

A foreclosure auction is defined as a public sale of a mortgaged property to satisfy a lender’s unpaid debt after a borrower defaults. Understanding how the foreclosure auction process works is the first step toward protecting your rights and making informed decisions before the sale date arrives. The lender, a trustee, third-party bidders, and the borrower all play distinct roles in this process. Knowing each role, and what happens at every stage, gives you real options when time is short.

How does the foreclosure auction process work?

The foreclosure auction process is the legal mechanism lenders use to recover money owed on a defaulted mortgage. The lender files a notice of default, then pursues a sale through either a court or a trustee, depending on state law. The notice of sale must include a legal property description, auction details, lender information, and reinstatement instructions, all published and recorded per state requirements. That notice is your earliest warning that a sale date has been set.

The auction itself is a competitive bidding event, typically held at a courthouse or online. The lender opens bidding with a credit bid representing the full outstanding loan balance, including interest and fees, without paying cash. If no third-party bidder beats that amount, the property becomes real estate owned (REO) and reverts to the lender. If a third party wins, ownership transfers to that buyer.

What are the different types of foreclosure?

Florida and other states use two primary foreclosure methods, and each one shapes the auction timeline and procedure in a significant way.

Judicial foreclosure requires the lender to file a lawsuit and obtain a court judgment before the property can be sold. Judicial sales require court confirmation before ownership transfers, which adds time and procedural steps. This process can take anywhere from six months to over two years, depending on court backlogs and borrower responses. For homeowners, that extended timeline creates more opportunity to explore options like loan modification, short sale, or even bankruptcy to stop the sale.

Non-judicial foreclosure uses a power of sale clause already written into the mortgage or deed of trust. No court involvement is required, which means the process moves much faster.

Key differences between the two methods:

- Timeline: Judicial foreclosure takes 6 months to over 2 years; non-judicial can close in as little as 3 months.

- Location: Judicial sales often occur at a courthouse; non-judicial sales may happen at the property or a designated public location.

- Notice requirements: Both require published notices, but the content and timing vary by state law.

- Sale confirmation: Judicial sales need court approval; non-judicial sales do not.

- Borrower protections: Judicial foreclosure gives borrowers more time and legal avenues to challenge the process.

Florida is a judicial foreclosure state. That means every foreclosure here goes through the court system, and homeowners have more time and legal standing than in many other states. Understanding the Florida foreclosure process specific to your situation is critical before any auction date is set.

How does the foreclosure bidding process work step by step?

The foreclosure bidding process follows a defined sequence. Each step carries legal weight, and missing any one of them has serious consequences for both bidders and homeowners.

- Auction announcement. The lender publishes a notice of sale with the date, time, location, and opening bid amount. This notice is recorded with the county and published in a local newspaper per state law.

- Bidder registration. Third-party bidders register before the auction, often providing proof of funds. Online platforms may require pre-approval or a deposit to participate.

- Opening bid. The lender places a credit bid equal to the debt owed, covering principal, interest, and fees, without paying cash. This sets the floor for all other bids.

- Competitive bidding. Third-party bidders raise the price above the credit bid. No mortgage financing is allowed. All bids must be backed by cash or certified funds.

- Winning bid and deposit. The highest bidder wins and must pay a deposit of 5%–10% of the bid immediately at the auction.

- Final payment. The remaining balance is typically due within 24–48 hours, though some states allow longer windows.

- Deed transfer. Once full payment clears, the deed is recorded and ownership transfers to the winning bidder.

Pro Tip: Experienced bidders bring multiple cashier’s checks in smaller denominations rather than one large check. This lets you meet the exact deposit amount without overpaying or scrambling for change at the auction.

Auction formats vary. In-person courthouse auctions are common in judicial foreclosure states like Florida. Online platforms have grown significantly and operate similarly, but they often add a buyer’s premium of 1%–5% on top of the winning bid. That premium is not optional. Factor it into your maximum bid before you raise your hand or click submit.

Failing to complete payment by the deadline is not a minor mistake. Nonpayment causes deposit forfeiture and can expose the bidder to legal liability if the property resells at a lower price. Winning a foreclosure auction creates a binding legal contract with strict deadlines and real financial consequences for default.

What are the key risks at a foreclosure auction?

Foreclosure auctions carry risks that catch unprepared buyers off guard. Homeowners watching their property go to auction face a different set of concerns, but both groups benefit from understanding these realities.

- As-is sales. Foreclosed properties sell as-is with no interior inspection rights. Buyers assume full responsibility for hidden damage, deferred maintenance, and structural issues discovered after the sale.

- Surviving liens. Junior liens, tax liens, and HOA liens may survive the foreclosure sale depending on their priority and the type of foreclosure. A title search before the auction is not optional. It is the only way to know what debt you are inheriting.

- Occupant eviction. If the former owner or a tenant still occupies the property, the new owner must handle eviction through the court system. That process adds time and legal costs.

- No financing allowed. Bidders wrongly assume mortgage financing is permitted; virtually all foreclosure auctions require cash or pre-approved hard money funding. Showing up without liquid funds means you cannot bid.

- Buyer’s premiums on online platforms. Online auctions commonly add 1%–5% to the final price. Many bidders calculate their maximum offer without accounting for this fee and end up overpaying.

Pro Tip: Run a title search through your county’s public records before the auction date. Many title defects and lien issues are visible in public filings and can save you from a costly surprise after the sale.

For homeowners facing the auction, the risks are different but equally serious. Your credit score takes a significant hit after a foreclosure sale. Any deficiency balance (the gap between the sale price and what you owed) may still be pursued by the lender in some states. Knowing your rights before the auction date is the most effective protection you have.

What happens after a foreclosure auction?

The auction closing triggers a chain of legal events that affects both the winning bidder and the former homeowner.

- Payment completion. The winning bidder pays the remaining balance, typically within 24–48 hours for courthouse auctions. Some states allow longer payment windows, but the deadline is always firm.

- Deed recording. Once full payment is received, the trustee or court officer records the deed. Ownership transfers officially at that point.

- Redemption rights. Some states give the former homeowner a statutory redemption period after the sale. During this window, the borrower can reclaim the property by paying the full sale price plus costs. Florida does not provide a post-sale redemption right in most cases, but the right of redemption exists up until the court confirms the sale.

- Eviction proceedings. If the former owner remains in the property, the new owner must file for eviction. This is a separate legal process and can take weeks or months.

- Credit and deficiency impact. A completed foreclosure sale stays on a credit report for seven years. If the sale price falls short of the loan balance, the lender may pursue a deficiency judgment in states that allow it.

Homeowners who have already reached the auction stage still have options worth exploring. Contacting a foreclosure defense attorney before the sale date can reveal legal grounds to delay or challenge the process. Even after the auction, understanding your redemption rights and deficiency exposure requires legal guidance specific to your state.

Key Takeaways

The foreclosure auction process is a binding public sale governed by strict legal timelines, cash payment requirements, and state-specific rules that homeowners and bidders must understand before the auction date arrives.

| Point | Details |

|---|---|

| Two foreclosure types | Judicial foreclosure takes 6 months to 2+ years; non-judicial can close in 3 months. |

| Lender credit bid sets the floor | Lenders open bidding at the full debt owed without paying cash; no third-party bid means the property becomes REO. |

| Cash is required to bid | No mortgage financing is allowed; bidders must bring certified funds or cash, plus a 5%–10% deposit on the spot. |

| As-is sale with hidden risks | Buyers inherit all property defects, surviving liens, and eviction costs with no right to inspect before purchase. |

| Post-auction rights vary by state | Florida homeowners can redeem the property before court confirmation; post-sale redemption rights are limited. |

What I’ve learned from watching homeowners face the auction clock

Most homeowners I work with arrive at the auction stage believing they have run out of options. That belief is almost always wrong, and it costs them dearly. The foreclosure auction process has built-in timelines that create real legal windows, and the homeowners who use those windows are the ones who come out with the least damage.

The single biggest mistake I see is waiting. Florida’s judicial foreclosure process gives homeowners more time than almost any other state. That time is not a grace period to accept the inevitable. It is a legal runway to negotiate a loan modification, pursue a short sale, or file for bankruptcy protection to halt the sale. Homeowners who engage early, even when the situation feels hopeless, consistently achieve better outcomes than those who disengage.

The second mistake is misunderstanding what the auction actually decides. Winning bidders at auction do not always get a clean property. Surviving liens, occupant issues, and title defects are real. For the homeowner, the auction does not automatically erase a deficiency balance. Both sides of the transaction carry more complexity than the public sale format suggests.

My advice is direct: get legal counsel before the auction date, not after. The options to save your home narrow significantly once the gavel falls.

— Steven

Wallacelawflorida can help you face the auction with clarity

Facing a foreclosure auction without legal guidance is one of the most avoidable financial mistakes a homeowner can make. Wallacelawflorida works with homeowners and real estate clients throughout Boynton Beach and South Florida to cut through the confusion and identify real options before the sale date arrives.

Whether you need to understand your redemption rights, challenge a procedural defect in the foreclosure process, or simply know what comes next, Wallacelawflorida provides the kind of direct, experienced counsel that makes a difference. The firm’s real estate legal services cover foreclosure defense, title issues, and post-auction matters. For investors and buyers, the legal tips every investor should know resource is a strong starting point. Contact Wallacelawflorida to schedule a consultation before the clock runs out.

FAQ

What is a credit bid in a foreclosure auction?

A credit bid is the lender’s opening bid at a foreclosure auction, set at the full amount of the outstanding loan balance including interest and fees, placed without cash. If no third-party bidder exceeds it, the lender takes ownership of the property as REO.

Can a homeowner stop a foreclosure auction after it is scheduled?

Yes, in many cases. Filing for bankruptcy triggers an automatic stay that halts the auction, and Florida’s judicial foreclosure process allows homeowners to raise legal defenses before the court confirms the sale.

Do foreclosure auction buyers need cash?

Foreclosure auction bidders must pay with cash or certified funds. Mortgage financing is not permitted at auction, and most sales require a 5%–10% deposit immediately with the balance due within 24–48 hours.

What liens survive a foreclosure sale?

Tax liens and certain government liens often survive a foreclosure sale regardless of their recording date. Junior mortgage liens are typically extinguished, but HOA liens and IRS liens may survive depending on their priority and the type of foreclosure conducted.

What happens if no one bids at a foreclosure auction?

If no third-party bidder exceeds the lender’s credit bid, the lender takes title to the property. The home then becomes REO and is typically listed for sale through the lender’s asset management process.