TL;DR:

- Foreclosure is the legal process lenders use to recover unpaid mortgage balances through property sale. It starts when borrowers breach the loan terms, usually by missed payments or unpaid taxes, and federal law mandates a 120-day delinquency period before filing. Lenders prefer alternatives like loan modifications to avoid costly foreclosure, which becomes imminent once legal proceedings begin.

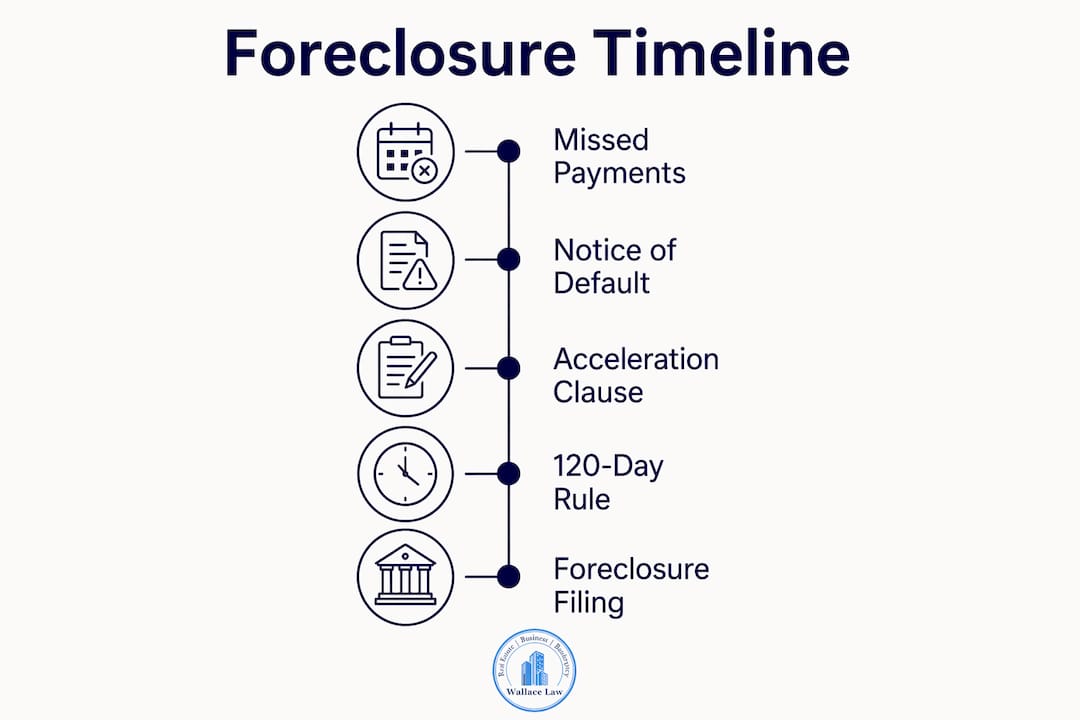

Foreclosure is defined as the legal process a lender uses to recover the unpaid balance of a mortgage loan by forcing the sale of the property used as collateral. Understanding why lenders initiate foreclosure proceedings starts with one fact: the home secures the loan. When a borrower stops meeting the terms of the mortgage contract, the lender’s right to that collateral activates. Federal Regulation X sets the minimum threshold at 120 days delinquent before a servicer can file. Knowing this timeline gives homeowners a real window to act before losing their home.

Why lenders initiate foreclosure proceedings: the contractual triggers

The primary breach triggering foreclosure is failure to make timely monthly mortgage payments. Missed payments disrupt the lender’s cash flow and signal that the borrower can no longer meet the loan’s core obligation. Most mortgage contracts include a grace period of 10–15 days, but consistent nonpayment puts the loan into default status quickly.

Missed payments are not the only trigger. Several other breaches can activate a lender’s foreclosure rights under the mortgage agreement:

- Unpaid property taxes. If property taxes go unpaid, the government can place a tax lien on the home. Most mortgage contracts require borrowers to keep taxes current, and a lapse gives the lender grounds to act.

- Homeowners insurance lapses. Lenders require active insurance to protect the collateral. A policy cancellation breaches the loan agreement directly.

- Covenant violations. Mortgage contracts often include property maintenance requirements. Letting a home fall into serious disrepair can trigger lender action.

- Reverse mortgage defaults. Reverse mortgages carry unique triggers, including failure to occupy the property as a primary residence or failure to maintain it adequately.

Once a borrower misses the cure deadline, most mortgage contracts include an acceleration clause. This clause makes the entire remaining loan balance due immediately, not just the missed payments. That shift from “catch up on payments” to “pay the full balance” is what forces foreclosure proceedings forward.

Pro Tip: If you receive a breach letter from your lender, the cure deadline listed in that letter is your most important date. Missing it triggers acceleration and shrinks your options fast.

How does the timing and legal process of foreclosure vary by state?

The foreclosure timeline is not the same everywhere. State law determines whether a lender must go through the courts or can proceed outside of them. Both paths follow federal minimums, but the speed and homeowner rights differ significantly.

The 120-day federal rule

Federal Regulation X prohibits servicers from filing for foreclosure until a borrower is more than 120 days delinquent. This mandatory waiting period exists so servicers must first evaluate the borrower for loss mitigation options. That four-month window is not a grace period in the casual sense. It is a federally protected opportunity to negotiate.

Judicial vs. non-judicial foreclosure

The two main foreclosure paths differ in speed, cost, and homeowner protections:

| Feature | Judicial foreclosure | Non-judicial foreclosure |

|---|---|---|

| Court involvement | Required | Not required |

| Typical timeline | 6–24 months | As short as 37 days to 6 months |

| Legal instrument | Mortgage | Deed of trust |

| Homeowner defense | Stronger, court-based | Limited, faster process |

| Common states | Florida, New York, Illinois | California, Texas, Georgia |

Judicial foreclosure requires the lender to file a lawsuit. The borrower receives a summons and has the right to respond in court. This process takes longer, which gives homeowners more time to mount a legal defense or negotiate. Florida uses the judicial process, which means Florida homeowners have more procedural protections than borrowers in non-judicial states.

Non-judicial foreclosure moves through a deed of trust arrangement. The lender follows a statutory notice process without court supervision. Timelines can be dramatically shorter, which is why early action matters even more in those states.

Notice of default and notice of sale

A Notice of Default is the formal public document that starts the foreclosure clock. It informs the borrower that the loan is in default and sets a deadline to cure the debt. After that deadline passes without resolution, the lender issues a Notice of Sale, which schedules the auction date. The gap between these two notices is often the last practical window for negotiation.

Pro Tip: In Florida, you have the right to file a legal response after receiving a foreclosure summons. Filing that response, even a simple denial, buys time and preserves your right to contest the case.

Why do lenders prefer to avoid foreclosure when possible?

Lenders do not want to foreclose. Foreclosure is costly and time-consuming for the institution, and a vacant property on a lender’s books generates no income while accumulating maintenance costs, legal fees, and market risk. A performing loan, even a modified one, is worth more to a lender than a foreclosed property.

This reality creates genuine room for negotiation. When borrowers communicate early with lenders, they trigger access to loss mitigation programs that servicers are required to evaluate under Regulation X. Common alternatives include:

- Loan modification. The lender restructures the loan terms, lowering the interest rate, extending the repayment period, or adding missed payments to the back end of the loan.

- Forbearance agreement. The lender temporarily reduces or pauses payments, giving the borrower time to recover from a financial hardship like job loss or medical emergency.

- Repayment plan. The borrower catches up on missed payments over a set period by adding a portion of the arrears to each monthly payment.

- Short sale. The lender agrees to accept less than the full loan balance from a property sale, avoiding the full foreclosure process.

- Deed in lieu of foreclosure. The borrower voluntarily transfers the property title to the lender, avoiding a public foreclosure sale.

The key insight here is that lenders open these doors when borrowers reach out first. Silence is the worst response to a missed payment. A borrower who calls their servicer after the first missed payment has far more options than one who waits until a foreclosure summons arrives.

What are the practical implications for homeowners when proceedings begin?

Once foreclosure proceedings formally begin, the consequences for homeowners are serious and time-sensitive. Acting fast is not optional. Here is what homeowners face once the process starts:

- Loss of ownership rights. After a foreclosure sale, the homeowner loses all rights to the property. In most states, the new owner can begin eviction proceedings within days of the sale.

- Deficiency judgments. In some states, if the foreclosure sale price does not cover the full loan balance, the lender can pursue the borrower for the remaining amount. This is called a deficiency judgment, and it can follow a homeowner for years.

- Credit damage. A completed foreclosure stays on a credit report for seven years and severely limits access to future mortgage financing.

- Shrinking legal options. Legal defenses in foreclosure are time-sensitive. Waiting until the sale date to contest the process typically forfeits the right to challenge it effectively.

- Redemption periods. Some states allow a post-sale redemption period during which the borrower can reclaim the property by paying the full debt. Florida does not have a post-sale redemption right, making pre-sale action the only real opportunity.

Homeowners should seek HUD-approved counseling as soon as financial hardship begins. HUD counselors are free, federally certified, and can help borrowers understand their options before the situation escalates. Federal programs like the Homeowner Assistance Fund also provide direct financial relief for eligible borrowers. Knowing these resources exist and using them early makes a measurable difference in outcomes.

Key takeaways

Lenders initiate foreclosure proceedings when borrowers breach the mortgage contract, most often through missed payments, and federal law requires a 120-day waiting period before any filing can occur.

| Point | Details |

|---|---|

| Primary foreclosure trigger | Missed mortgage payments breach the loan contract and activate the lender’s right to foreclose. |

| Federal 120-day rule | Regulation X bars servicers from filing until the borrower is more than 120 days delinquent. |

| State process differences | Judicial foreclosure takes 6–24 months; non-judicial foreclosure can close in as little as 37 days. |

| Lenders prefer alternatives | Loan modifications, forbearance, and repayment plans cost lenders less than a full foreclosure. |

| Early action is critical | Legal defenses and loss mitigation options shrink significantly once a foreclosure sale is scheduled. |

What I’ve learned after years of watching homeowners navigate this process

Most homeowners who end up losing their homes to foreclosure had options they never used. That is the uncomfortable truth I keep coming back to. The lender’s goal is not to take your house. It is to recover money. A house sitting empty costs the lender money every single month. That shared interest in avoiding foreclosure is real leverage for any borrower willing to use it.

The biggest misconception I see is that once a Notice of Default arrives, the fight is over. It is not. In a judicial state like Florida, the foreclosure process involves a court case. You have the right to respond to the foreclosure filing and raise defenses. Procedural errors by the lender, improper notice, or failure to follow Regulation X requirements can all slow or stop a foreclosure. But those defenses only work if you raise them on time.

The other mistake I see constantly is waiting. Every week of silence after a missed payment is a week of options disappearing. The 120-day federal window exists precisely because Congress recognized that borrowers need time and a real chance to find solutions. Use that time. Call your servicer. Contact a HUD counselor. Talk to a foreclosure defense attorney before the summons arrives, not after. The homeowners who come out of this with their homes intact are almost always the ones who acted before the situation became a crisis.

— Steven

How Wallacelawflorida helps homeowners facing foreclosure

Facing a foreclosure notice is one of the most stressful situations a homeowner can experience. Wallacelawflorida works directly with homeowners in Boynton Beach and across Florida to evaluate every available option before a foreclosure sale occurs.

The attorneys at Wallacelawflorida understand Florida’s judicial foreclosure process in detail, from reviewing lender compliance with Regulation X to filing timely legal responses that preserve your rights. Whether the goal is a loan modification, a forbearance agreement, or a full foreclosure defense strategy, the firm provides personal attention and clear guidance at every step. If you are behind on payments or have already received a Notice of Default, the time to get legal advice is now. Contact Wallacelawflorida to schedule a consultation and understand exactly where you stand.

FAQ

What triggers a lender to start foreclosure proceedings?

The most common trigger is missed mortgage payments, which breach the loan contract. Other triggers include unpaid property taxes, lapsed homeowners insurance, and covenant violations under the mortgage agreement.

How long does a lender have to wait before filing for foreclosure?

Federal Regulation X requires servicers to wait until a borrower is more than 120 days delinquent before filing for foreclosure. This period must include an evaluation of loss mitigation options.

Can a homeowner stop foreclosure after proceedings begin?

Yes. In judicial foreclosure states like Florida, homeowners can file a legal response, raise defenses, and negotiate with the lender even after proceedings begin. Acting quickly is critical because legal defenses are time-sensitive.

Why would a lender agree to a loan modification instead of foreclosing?

Lenders prefer loan modifications because foreclosure is expensive and time-consuming. A modified loan that performs generates more value for the lender than a vacant property sold at auction.

What happens to a homeowner after a foreclosure sale?

After a foreclosure sale, the homeowner loses all rights to the property and may face eviction. In some states, the lender can also pursue a deficiency judgment for any remaining loan balance not covered by the sale price.