TL;DR:

- The automatic stay stops most creditor calls immediately after filing for bankruptcy by issuing a federal court order.

- Creditors must receive actual notice of the filing to be legally bound and stop collection efforts.

The automatic stay is a federal court order that stops creditors from calling you the moment you file for bankruptcy. Defined under 11 U.S.C. § 362, this legal protection covers credit card companies, medical providers, mortgage servicers, and most other creditors simultaneously. Understanding why creditors stop calling in bankruptcy, and what happens when they do not, puts you in control of your own financial recovery. This guide explains the legal mechanics, the exceptions, and the practical steps that protect your peace of mind from day one.

Why creditors stop calling after bankruptcy filing

The automatic stay is the direct answer to why creditors stop calling in bankruptcy. Filing your petition triggers the stay instantly, without any additional court action required on your part. It covers phone calls, emails, letters, wage garnishments, and active lawsuits in one sweeping federal order.

The stay applies broadly. Credit card issuers, hospital billing departments, auto lenders, and personal loan companies all fall under its reach. The only major exceptions involve domestic support obligations like child support, certain tax proceedings, and criminal restitution. For the vast majority of consumer debts, the automatic stay functions as an immediate legal wall between you and every collector.

What makes this protection powerful is its federal status. No state law or creditor contract can override it. A creditor who continues collection activity after receiving notice of your filing is not just being aggressive. That creditor is breaking federal law.

How creditors are legally required to stop contacting you

A creditor becomes legally bound by the automatic stay only after receiving actual notice of your bankruptcy filing. The bankruptcy court mails notices to every creditor listed in your petition schedules. This is why listing every creditor with a current, accurate mailing address is not optional. It is the mechanism that activates your protection.

Here is what the notice and compliance process looks like in practice:

- Court notification: The bankruptcy clerk sends a formal notice to each listed creditor, usually within a few days of filing.

- Creditor obligation: Once a creditor receives that notice, all collection activity must stop immediately.

- Legal consequences: Under 11 U.S.C. § 362(k), a creditor who willfully violates the stay faces actual damages, attorney fees, and punitive sanctions.

- Punitive damages: Courts have awarded significant punitive damages in cases where creditors showed deliberate disregard for the stay.

The word “willful” matters here. A creditor who calls you after receiving notice cannot claim it was a mistake. Courts treat that as a knowing violation, and the financial penalties reflect that standard.

Pro Tip: Double-check every creditor’s address before your attorney files your petition. A single outdated address can delay notice and leave you unprotected from that creditor’s calls for days or even weeks.

Accurate creditor schedules are the single most important preparation step for stopping collection calls quickly. Wallacelawflorida attorneys review these schedules carefully before filing to close that gap.

Why creditors might still call after you file

Most creditor calls after filing are not deliberate harassment. Automated billing systems create a lag between when the court mails notice and when a creditor’s internal records are updated. A robo-dialer does not check the federal court docket before placing a call.

Common reasons calls continue after filing include:

- Processing delays: Large creditors with centralized call centers may take several days to update account status after receiving court notice.

- Debt transfers: If your account was sold to a third-party collector before you filed, that collector may not have received notice yet.

- Claimed non-receipt: Some creditors dispute receiving the court notice, particularly if your petition listed an outdated address.

- New debt buyers: Debts sold after your filing date may land with collectors who have no knowledge of your case.

The difference between an original creditor and a third-party debt collector also matters here. The Fair Debt Collection Practices Act, known as the FDCPA, governs third-party collectors specifically. Original creditors operate under different rules. Both are stopped by the automatic stay, but your legal remedies against each may differ depending on the circumstances.

Pro Tip: Log every call you receive after filing. Write down the date, time, caller ID, and what was said. This documentation is your evidence if you need to pursue a stay violation claim.

If calls continue after your attorney has confirmed notice was sent, report it immediately. Your attorney can send a direct cease communication letter to that specific creditor and, if needed, file a motion for sanctions with the bankruptcy court. Courts take these violations seriously, and documenting contacts gives your attorney the evidence needed to act.

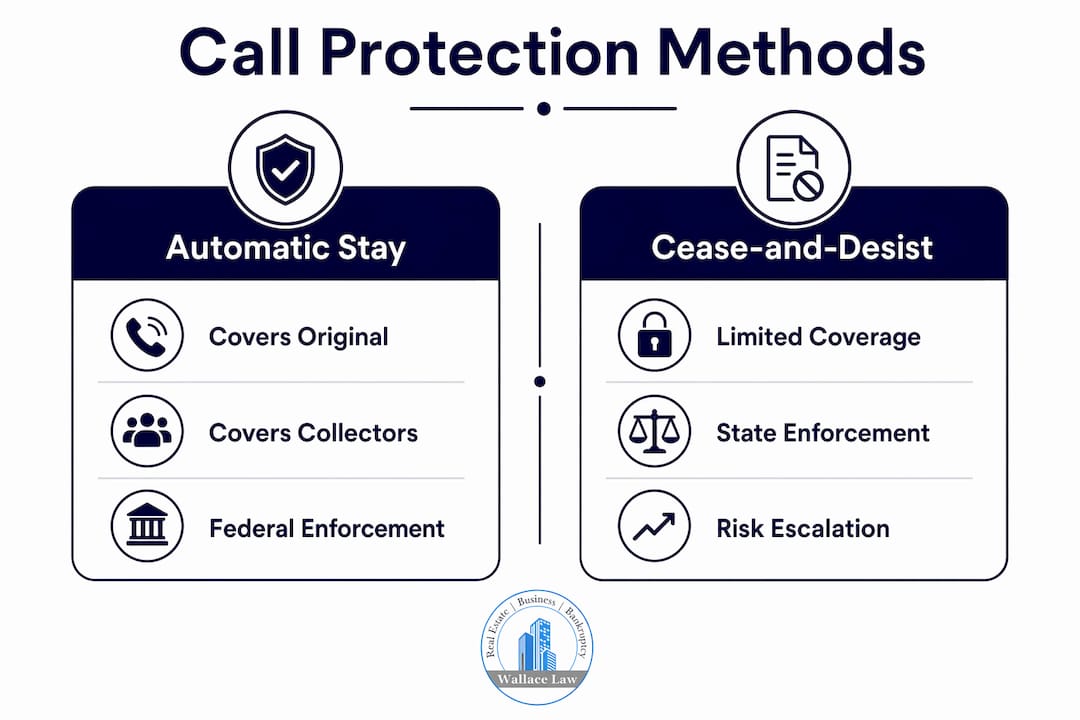

Automatic stay vs. cease-and-desist letters: which actually stops calls?

Many people try sending cease-and-desist letters before considering bankruptcy. The FDCPA does allow consumers to stop third-party collector calls with a written letter. The problem is that this protection covers only debt collectors, not original creditors like your bank or hospital.

| Protection method | Covers original creditors | Covers third-party collectors | Federal enforcement | Risk of escalation |

|---|---|---|---|---|

| Cease-and-desist letter | No | Yes | No | High |

| Bankruptcy automatic stay | Yes | Yes | Yes | None |

A cease-and-desist letter sent to an original creditor carries real risk. That creditor is not required to stop calling. Worse, the letter can signal that you are aware of the debt and unwilling to pay, which sometimes prompts a lawsuit rather than silence. Original creditors can sue to collect, and a judgment against you opens the door to wage garnishment and bank levies.

The automatic stay functions as a nationwide federal injunction. It covers every creditor, original or third-party, without exception for most consumer debts. No letter you write carries that authority. The stay is court-ordered, federally backed, and immediately enforceable. That is a fundamentally different level of protection.

What happens after discharge: do creditor calls stop permanently?

The bankruptcy discharge replaces the automatic stay once your case closes. The discharge injunction permanently prohibits creditors from attempting to collect any debt that was included in your bankruptcy. This is a lifetime ban on collection for those specific debts.

Despite that, some creditors continue calling after discharge. The most common reasons include:

- Automated billing errors: A creditor’s system may not have flagged the account as discharged, triggering automated statements or calls.

- New debt buyers: A discharged debt sold to a new collector after your case closed may reach a buyer with no knowledge of your discharge.

- Secured debt confusion: Creditors on secured debts, like a mortgage or car loan you reaffirmed, retain collection rights on the collateral, which sometimes causes confusion about what they can and cannot contact you about.

A post-discharge violation is a serious matter. Continuing collection after discharge violates the discharge injunction, and courts can impose sanctions and damages against the offending creditor. Your remedy is to contact your bankruptcy attorney immediately, provide your discharge order, and let your attorney send formal notice. If the calls continue after that, a motion for contempt is the next step. Courts have little patience for creditors who ignore a discharge order.

Key Takeaways

The automatic stay under 11 U.S.C. § 362 stops creditor calls the instant you file for bankruptcy, but its effectiveness depends entirely on accurate creditor listings and timely notice.

| Point | Details |

|---|---|

| Automatic stay is immediate | The stay activates the moment your bankruptcy petition is filed, covering calls, emails, and lawsuits. |

| Notice triggers compliance | Creditors are only legally bound once they receive court notice, so accurate address listings are critical. |

| Willful violations carry penalties | Under 11 U.S.C. § 362(k), creditors who call after notice face damages, attorney fees, and punitive sanctions. |

| Cease-and-desist letters fall short | FDCPA letters stop third-party collectors only; the automatic stay covers all creditors under federal law. |

| Discharge protection is permanent | The discharge injunction permanently bans collection on included debts, even after your case closes. |

What I have learned from watching clients navigate creditor calls

The clients who handle the post-filing period best are the ones who come in prepared. They have a list of every creditor, every account number, and every current mailing address. When the automatic stay kicks in and the calls stop within a week, they are not surprised. They expected it because they understood the mechanism.

The clients who struggle are the ones who listed a creditor with a three-year-old address. That creditor never got court notice. The calls kept coming. The client assumed the stay was not working, panicked, and sometimes made the mistake of calling the creditor directly to explain the situation. That is the wrong move. Every contact you initiate after filing is a potential complication.

The other thing I tell every client: do not assume a call after filing is automatically a violation. Most of the time, it is a system delay. Give it a few days after your attorney confirms notice was sent. If calls continue past that point, document everything and report it. Do not try to handle it yourself by arguing with the collector. That is what your attorney is there for.

The automatic stay is genuinely one of the most powerful tools in consumer law. I have seen it stop wage garnishments, freeze foreclosures, and end years of harassment within 24 hours of filing. But it only works as well as the paperwork behind it. Preparation is not a formality. It is the foundation of your protection.

— Steven

How Wallacelawflorida can help you stop creditor calls for good

Creditor calls are one of the most stressful parts of financial hardship. Wallacelawflorida helps clients in Boynton Beach and across Florida file bankruptcy correctly the first time, with complete creditor schedules that trigger the automatic stay without delay.

The attorneys at Wallacelawflorida verify every creditor address before filing, handle creditor harassment claims when violations occur, and guide you through both Chapter 7 and Chapter 13 processes with clear, direct communication. If creditors are still calling after your filing, the firm can act quickly to enforce your rights. Get the bankruptcy legal help you need from attorneys who know Florida law and treat your case as a priority, not a number.

FAQ

Why do creditors stop calling when you file for bankruptcy?

Filing bankruptcy triggers the automatic stay under 11 U.S.C. § 362, a federal court order that immediately halts all collection activity, including phone calls, from most creditors.

How long does it take for creditor calls to stop after filing?

Most calls stop within a few days of filing once the bankruptcy court mails notice to your creditors. Calls that continue after confirmed notice may constitute a willful stay violation.

Can a creditor still call me if they were not listed in my bankruptcy?

Yes. A creditor must receive actual notice of your filing to be bound by the automatic stay. Unlisted creditors with no notice are not legally required to stop calling.

What should I do if creditors keep calling after my bankruptcy discharge?

Document every call and contact your bankruptcy attorney immediately. Post-discharge collection violates the discharge injunction, and courts can impose sanctions and damages against creditors who persist.

Does a cease-and-desist letter work as well as bankruptcy for stopping calls?

No. A cease-and-desist letter under the FDCPA covers only third-party debt collectors and does not bind original creditors. The automatic stay covers all creditors under federal law and carries court-enforced penalties for violations.