TL;DR:

- Chapter 13 bankruptcy is a court-supervised repayment plan allowing individuals with regular income to retain property while reordering and repaying debts over three to five years. Eligibility requires stable income, debt limits, tax compliance, credit counseling, and no recent dismissals, with plan duration depending on income relative to the median. The process involves filing, trustee assignment, creditor meeting, plan confirmation, monthly payments, and discharge, with different debts treated variably to protect assets and stop foreclosure.

Chapter 13 bankruptcy is a court-supervised repayment plan that allows individuals with regular income to reorganize their debts and repay them over three to five years while keeping property like homes and vehicles. Known formally as the “wage earner’s plan,” it sits under Title 11 of the U.S. Bankruptcy Code and differs fundamentally from Chapter 7, which liquidates assets to settle debts. If you are facing foreclosure, mounting credit card balances, or car loan arrears, Chapter 13 offers a structured path forward without surrendering what you own. This guide covers eligibility, the filing process, how different debts are treated, and what separates Chapter 13 from other options.

What is Chapter 13 bankruptcy and who qualifies?

Chapter 13 bankruptcy is defined as a reorganization bankruptcy, not a liquidation bankruptcy. You keep your assets, but you commit to a court-approved repayment plan funded by your disposable income. The U.S. Bankruptcy Code sets firm eligibility boundaries, and understanding them before you file saves time and avoids dismissal.

To qualify, you must meet all of the following conditions:

- Regular income: This includes wages, self-employment earnings, rental income, Social Security, and pension payments. The income must be stable enough to fund a multi-year repayment plan.

- Debt limits: Unsecured debt below $526,700 and secured debt below $1,580,125 at the time of filing. These figures adjust periodically, so confirm current limits before proceeding.

- Tax compliance: You must have filed required federal and state tax returns for the previous four years. Missing returns can disqualify your case.

- Credit counseling: You must complete an approved credit counseling course within 180 days before filing. A second debtor education course is required before discharge.

- No recent dismissals: If a prior bankruptcy case was dismissed within the last 180 days due to willful failure to follow court orders, you cannot refile immediately.

Unlike Chapter 7, Chapter 13 does not use a means test to determine eligibility based on income level. Instead, your income level determines the length of your repayment plan. If your income falls below your state’s median, your plan runs three years. If it exceeds the median, the plan runs five years.

Pro Tip: Before filing, use the bankruptcy filing checklist from Wallacelawflorida to confirm you have all required documents, including tax returns and proof of income, organized in advance.

How does the Chapter 13 bankruptcy process work?

The process moves through six distinct stages, each with specific deadlines and requirements. Missing any one of them can delay or dismiss your case.

- File the petition. You submit a bankruptcy petition, schedules of assets and liabilities, a statement of financial affairs, and your proposed repayment plan to the federal bankruptcy court. Filing triggers an automatic stay that immediately halts foreclosure, wage garnishment, vehicle repossession, and most creditor collection actions.

- Trustee assignment. The court appoints a Chapter 13 trustee who reviews your plan, collects your monthly payments, and distributes funds to creditors. The trustee does not represent you. Their role is neutral administration.

- Meeting of creditors (341 meeting). This occurs 21 to 50 days after filing. You answer questions under oath from the trustee and any creditors who attend. Most creditors do not appear.

- Plan confirmation hearing. Held 20 to 45 days after the creditors meeting, this is where the judge approves or rejects your repayment plan. Creditors may object. Your attorney addresses those objections before or during the hearing.

- Monthly payments. Once confirmed, you make regular payments to the trustee, who distributes them to creditors according to the plan’s priority structure. This continues for the full plan duration.

- Discharge. After completing all plan payments and the required debtor education course, the court issues a discharge order eliminating remaining eligible debts.

| Stage | Timeline |

|---|---|

| Automatic stay | Effective immediately upon filing |

| 341 meeting of creditors | 21 to 50 days after filing |

| Plan confirmation hearing | 20 to 45 days after 341 meeting |

| Plan duration | 3 years (below median income) or 5 years (above median) |

| Discharge issued | After final payment and education course |

Pro Tip: Start making plan payments immediately after filing, even before confirmation. Courts expect payment consistency from day one, and gaps in payment history can trigger dismissal before your plan is even approved.

For a detailed walkthrough of each stage, the steps in Chapter 13 bankruptcy resource from Wallacelawflorida breaks down what to expect at each court appearance.

How are different debts treated under Chapter 13?

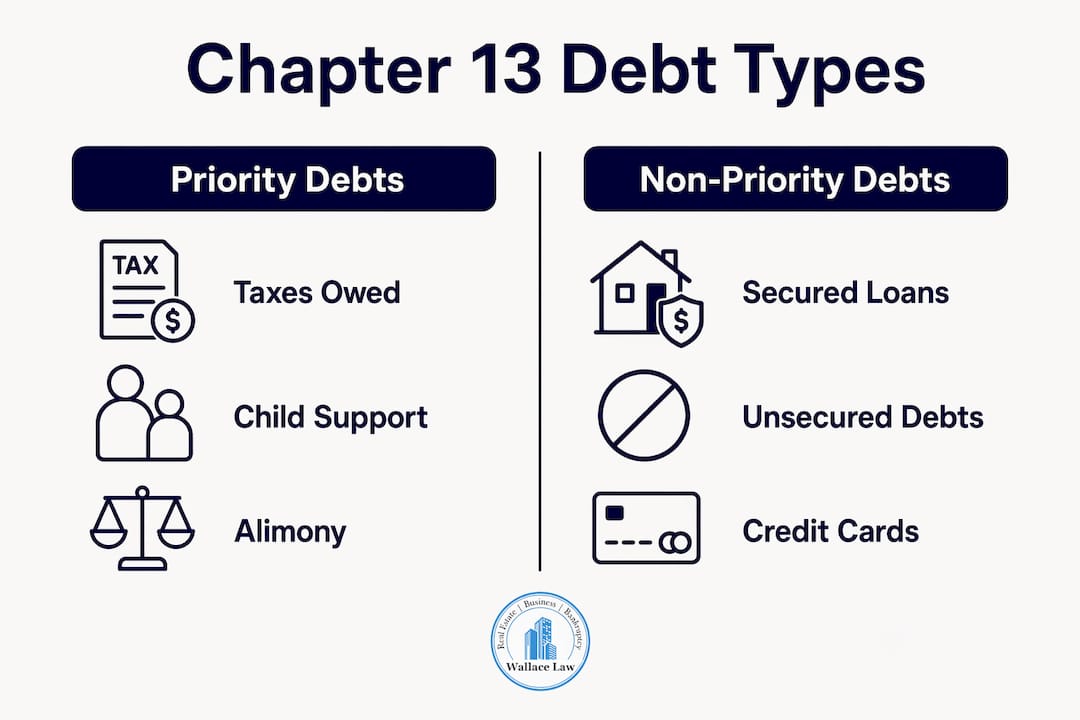

Chapter 13 does not treat all debts equally. The repayment plan divides debts into three categories, each with its own rules.

| Debt type | Treatment under Chapter 13 |

|---|---|

| Priority debts | Paid in full (taxes owed, child support, alimony, certain fines) |

| Secured debts | Ongoing payments continue; arrears caught up through the plan |

| Unsecured debts | Partially repaid based on disposable income; remainder discharged |

Priority debts must be paid in full through the plan. This category includes back taxes owed to the IRS, domestic support obligations like child support and alimony, and certain employee wage claims. There is no flexibility here. If your plan does not fully fund these debts, the court will not confirm it.

Secured debts, such as a mortgage or car loan, require you to continue making regular ongoing payments while also catching up on any arrears through the plan. This is the mechanism that makes Chapter 13 the preferred tool for stopping foreclosure. Homeowners in arrears can spread those missed payments across the full plan term rather than paying them in a lump sum. The foreclosure defense options available through Chapter 13 are one of the most powerful features the law provides.

Unsecured debts, including credit cards, medical bills, and personal loans, receive whatever is left of your disposable income after priority and secured debts are funded. The remaining balance is discharged at the end of the plan. Chapter 13 also offers what attorneys call a “super discharge,” covering certain debts not dischargeable in Chapter 7, including some governmental fines and certain malicious injury claims. This is a meaningful advantage for filers with unusual debt types.

How does Chapter 13 differ from Chapter 7 and what are its benefits?

Chapter 7 and Chapter 13 solve different problems. Choosing between them depends on your income, your assets, and the types of debt you carry.

- Asset protection: Chapter 7 liquidates non-exempt assets to pay creditors. Chapter 13 lets you keep all assets as long as your plan pays creditors at least what they would receive in a Chapter 7 liquidation.

- Duration: Chapter 7 typically concludes in four to six months. Chapter 13 runs three to five years. The longer timeline is the trade-off for keeping property and accessing broader discharge options.

- Co-signer protection: Chapter 13 includes a co-debtor stay that protects co-signers on consumer debts during the active case. Chapter 7 offers no equivalent protection.

- Foreclosure prevention: Chapter 7 can delay foreclosure temporarily through the automatic stay, but it does not provide a mechanism to catch up on mortgage arrears. Chapter 13 does.

- Credit report impact: Chapter 13 stays on your credit report for seven years from the filing date. Chapter 7 stays for ten years. Successful completion of a Chapter 13 plan signals repayment effort, which some lenders view more favorably.

- IRS and tax debt: Chapter 13 can address certain tax debts through the plan, and the automatic stay halts IRS wage garnishment immediately upon filing.

Chapter 13 is the better choice when you own a home with equity you want to protect, when you have non-exempt assets that Chapter 7 would liquidate, or when your income exceeds the Chapter 7 means test threshold. For a direct comparison of both paths, the Chapter 7 vs. Chapter 13 differences guide from Wallacelawflorida lays out the key distinctions clearly.

Key takeaways

Chapter 13 bankruptcy is the most effective tool for individuals with regular income who need to protect assets, stop foreclosure, and repay debts over time under court supervision.

| Point | Details |

|---|---|

| Core definition | Chapter 13 is a 3 to 5 year court-supervised repayment plan, not a liquidation. |

| Eligibility limits | Unsecured debt must be below $526,700 and secured debt below $1,580,125 to qualify. |

| Automatic stay | Filing immediately halts foreclosure, garnishment, and repossession. |

| Debt treatment | Priority debts paid in full; secured arrears caught up; unsecured debts partially discharged. |

| Chapter 13 vs. Chapter 7 | Chapter 13 protects assets and co-signers; Chapter 7 is faster but offers less protection. |

What I’ve learned from watching Chapter 13 cases succeed and fail

Most people who struggle with Chapter 13 do not fail because the law is complicated. They fail because of two or three specific oversights that no one warned them about.

The first is mortgage payments. Ongoing mortgage payments must continue throughout the plan, separate from the arrears being addressed through the trustee. I have seen clients assume the trustee handles everything mortgage-related. The trustee handles only the catch-up amount. Miss two or three current payments during the plan, and you are back in foreclosure territory despite having bankruptcy protection in place.

The second is new debt. Any new debt over $1,000 requires prior written approval from the trustee. A car repair on a new credit card, a medical financing agreement, a furniture purchase on credit. All of it counts. Unauthorized new debt can get your case dismissed, which wipes out years of payments and leaves you unprotected.

The third is the trustee’s fee. Trustee fees typically run 10% of every plan payment before creditors receive a dollar. That means a $1,000 monthly payment sends $900 to creditors and $100 to the trustee. Attorneys who do not account for this when building the plan end up with underfunded creditor distributions and plan confirmation problems.

Chapter 13 works when you go in with realistic numbers, a plan built by someone who knows the local trustee’s expectations, and a clear commitment to staying current on both your plan payments and your ongoing obligations. It is not a passive process. It rewards preparation.

— Steven

How Wallacelawflorida helps you file Chapter 13 with confidence

Facing bankruptcy is stressful enough without trying to decode federal court procedures on your own. Wallacelawflorida works directly with individuals in Boynton Beach and surrounding Florida communities to build realistic Chapter 13 repayment plans, protect homes from foreclosure, and guide clients through every court appearance from filing to discharge.

The attorneys at Wallacelawflorida know Florida’s local trustees, understand what confirmation hearings require, and take the time to explain your options clearly before you commit to anything. You can start with the free bankruptcy eBook to build your foundational knowledge, or go directly to the bankruptcy services page to schedule a consultation. Either way, you will not be navigating this alone.

FAQ

What is the difference between Chapter 13 and Chapter 7?

Chapter 7 liquidates non-exempt assets to pay creditors and concludes in four to six months, while Chapter 13 is a three to five year repayment plan that lets you keep all assets. Chapter 13 also protects co-signers and allows you to catch up on mortgage arrears to stop foreclosure.

How long does a Chapter 13 repayment plan last?

The plan lasts three years if your income falls below your state’s median and five years if it exceeds the median. The maximum permitted duration under the Bankruptcy Code is five years.

What debts cannot be discharged in Chapter 13?

Student loans, most recent tax debts, child support, alimony, and debts from fraud or willful misconduct generally survive Chapter 13 discharge. Chapter 13 does offer a broader “super discharge” than Chapter 7, covering some debts like certain governmental fines that Chapter 7 cannot eliminate.

Does Chapter 13 stop foreclosure immediately?

Yes. Filing Chapter 13 triggers an automatic stay that halts foreclosure proceedings the moment the petition is submitted. The repayment plan then allows you to catch up on mortgage arrears over the plan term while continuing regular monthly mortgage payments.

How does Chapter 13 affect your credit score?

Chapter 13 remains on your credit report for seven years from the filing date, compared to ten years for Chapter 7. Successful completion of the repayment plan demonstrates a commitment to repaying debts, which lenders may view more favorably than a Chapter 7 liquidation.