TL;DR:

- Fresh start bankruptcy is a court-supervised process that discharges eligible debts and stops creditor collection efforts. It primarily occurs through Chapter 7 or Chapter 13, helping individuals rebuild finances and gain legal relief from overwhelming obligations. The process involves credit counseling, filing, automatic stay activation, and a final discharge, with some debts like student loans and child support generally remaining.

Fresh start bankruptcy is defined as a court-supervised legal process that discharges eligible debts and immediately stops creditor collection efforts, giving individuals a legal path to rebuild their finances. The term “fresh start” is informal. The recognized legal mechanism is a bankruptcy discharge under the U.S. Bankruptcy Code, achieved primarily through Chapter 7 or Chapter 13. Supreme Court precedents from Local Loan Co. v. Hunt (1934) through Grogan v. Garner (1991) confirm that bankruptcy’s core purpose is giving honest, financially distressed individuals relief from overwhelming obligations. The process is not automatic. It requires court supervision, means testing, and mandatory credit counseling before any debt is erased.

What does fresh start bankruptcy mean, and how is it defined legally?

A bankruptcy discharge is the legal event that ends your personal liability for eligible debts. Once a court issues a discharge order, creditors can no longer legally pursue you for those obligations. The American Bar Association describes fresh start bankruptcy as a court-supervised process offering debt relief through either discharge or restructuring, tailored to each person’s financial situation.

The two primary pathways are Chapter 7 and Chapter 13. Chapter 7 eliminates most unsecured debts through liquidation and typically concludes within 3–6 months. Chapter 13 restructures debt into a supervised repayment plan lasting 3–5 years. Both routes carry the same legal goal: releasing you from debt liability so you can move forward without creditor pressure.

Understanding the fresh start bankruptcy definition matters because the phrase sets expectations. It does not mean all debts vanish overnight. It means the law gives you a structured exit from debts you cannot realistically repay, with specific rules about what qualifies.

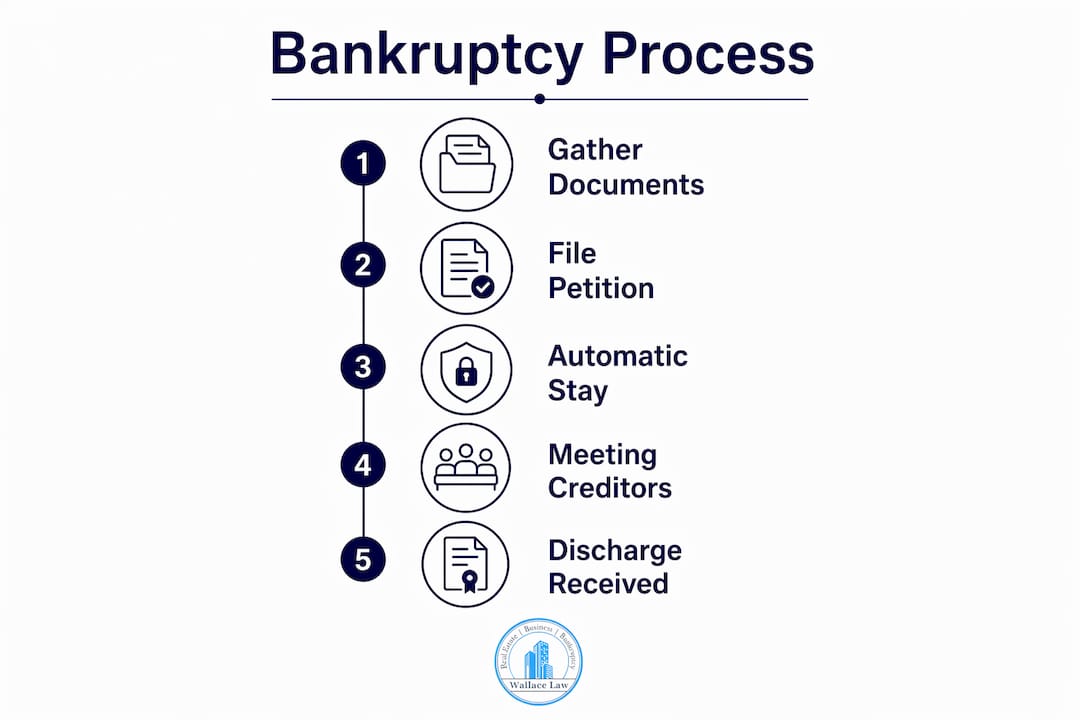

How does the fresh start bankruptcy process work?

The process follows a clear sequence, and knowing each step removes a lot of the fear around filing.

- Complete credit counseling. Federal law requires you to finish an approved credit counseling course within 180 days before filing. Passing this requirement is mandatory to qualify for a fresh start through bankruptcy.

- File your petition. You submit a bankruptcy petition, schedules of assets and liabilities, and a statement of financial affairs to the federal bankruptcy court.

- Automatic stay activates. The moment you file, the automatic stay triggers instantly, stopping creditor lawsuits, wage garnishments, and collection calls. This protection is immediate and applies to virtually all collection activity.

- Means test evaluation. For Chapter 7, the court applies a means test to confirm your income falls below the state median or that your disposable income is insufficient to repay debts. Failing the means test redirects you to Chapter 13.

- Trustee review. A court-appointed trustee reviews your assets. In Chapter 7, non-exempt assets can be liquidated to pay creditors. In practice, most Chapter 7 cases are no-asset cases, meaning debtors keep 100% of their exempt property, including primary vehicles and household goods.

- Discharge order issued. In Chapter 7, the discharge typically arrives 3–6 months after filing. In Chapter 13, it comes after you complete the repayment plan.

Pro Tip: Gather all financial documents, including pay stubs, tax returns, and a complete list of creditors, before you file. Incomplete filings delay the process and can jeopardize your discharge.

The difference between Chapter 7 and Chapter 13 comes down to speed versus asset protection. Chapter 7 is faster but may expose non-exempt property. Chapter 13 takes longer but lets you catch up on mortgage arrears and keep assets that would otherwise be liquidated.

What types of debts can be eliminated through bankruptcy?

Not every debt qualifies for discharge, and this is where many people get surprised. The fresh start bankruptcy process eliminates most unsecured debts but leaves certain obligations intact.

Debts typically dischargeable in bankruptcy:

- Credit card balances

- Medical bills

- Personal loans

- Utility arrears

- Most civil court judgments

Debts that generally survive bankruptcy:

- Child support and alimony

- Most student loans

- Recent income tax debts

- Debts from fraud or intentional wrongdoing

- Criminal fines and restitution

| Debt Type | Dischargeable? |

|---|---|

| Credit card debt | Yes |

| Medical bills | Yes |

| Personal loans | Yes |

| Student loans | Generally no |

| Child support | No |

| Recent tax debts | Generally no |

| Mortgage balance | No (lien survives) |

| Alimony | No |

Common exceptions include certain taxes, student loans, and child support obligations. These debts survive bankruptcy regardless of which chapter you file under. Knowing this before you file prevents the painful surprise of completing the process and still owing significant amounts.

Co-signers face a separate reality. If a friend or family member co-signed a loan with you, your discharge does not protect them. The creditor can still pursue your co-signer for the full balance. Chapter 13 includes a “co-debtor stay” that temporarily protects co-signers, which Chapter 7 does not.

Pro Tip: Before filing, categorize every debt as dischargeable or non-dischargeable. This single exercise clarifies whether bankruptcy actually solves your specific problem or whether another debt relief path fits better.

How does Chapter 7 compare to Chapter 13 for a fresh start?

The two chapters serve different financial situations, and choosing the wrong one costs time, money, and sometimes assets. Here is a direct comparison.

| Feature | Chapter 7 | Chapter 13 |

|---|---|---|

| Process type | Liquidation | Repayment plan |

| Timeline | 3–6 months | 3–5 years |

| Means test required | Yes | Yes (income cap) |

| Asset risk | Non-exempt assets sold | Assets generally protected |

| Mortgage arrears | Not cured | Can be cured through plan |

| Co-signer protection | No | Yes (co-debtor stay) |

| Discharge timing | After case closes | After plan completion |

| Best for | Low income, few assets | Higher income, assets to protect |

Chapter 7 offers liquidation and fast discharge, while Chapter 13 provides a supervised repayment plan over 3–5 years. Approximately 70% of consumer bankruptcy filings are Chapter 7, reflecting its appeal as the faster route to debt elimination.

Chapter 13 suits people who earn too much to pass the Chapter 7 means test, own a home with equity they want to protect, or have fallen behind on a mortgage and need time to catch up. The repayment plan consolidates debts into one monthly payment to the trustee, who distributes funds to creditors. Completing the plan earns a discharge on remaining eligible balances.

The means test is the deciding factor for most people. It compares your average monthly income over the past six months to your state’s median income. If you fall below the median, Chapter 7 is available. If you exceed it, you must pass a second calculation measuring disposable income. Failing both calculations means Chapter 13 is your path.

What happens after bankruptcy discharge?

Discharge ends your personal liability, but it does not erase the bankruptcy from your financial record. A bankruptcy discharge removes personal liability but stays on your credit report for 7–10 years. Chapter 7 remains for 10 years; Chapter 13 remains for 7 years.

Steps to protect your fresh start after discharge:

- Review all three credit reports (Equifax, Experian, TransUnion) within 30 days of discharge. Discharged debts must show a zero balance, not an open collection status.

- Send a written dispute to any creditor that continues reporting a balance on a discharged debt. The discharge injunction prohibits collection on those debts.

- Open a secured credit card or credit-builder loan to begin rebuilding your credit history. Consistent on-time payments are the fastest legal path to credit recovery.

- Build an emergency fund before taking on new credit. Three months of expenses in savings prevents the cycle from restarting.

- Consult an attorney immediately if a creditor contacts you about a discharged debt. That contact likely violates the discharge injunction and may entitle you to damages.

Pro Tip: Set a calendar reminder to pull your credit reports at 30 days, 6 months, and 12 months post-discharge. Errors on credit reports after bankruptcy are common and correctable, but only if you catch them.

The exemptions that protected your property during bankruptcy continue to matter afterward. Florida, for example, offers a homestead exemption that protects unlimited home equity in a primary residence. Understanding which exemptions apply to your estate planning and asset protection strategy is a smart next step after discharge.

Key Takeaways

Fresh start bankruptcy is a legal discharge of eligible debts under court supervision, achieved through Chapter 7 or Chapter 13, with immediate creditor protection and long-term credit reporting consequences.

| Point | Details |

|---|---|

| Legal discharge ends liability | A court discharge order stops creditors from collecting on eligible debts permanently. |

| Automatic stay is immediate | Filing triggers instant protection from lawsuits, garnishments, and collection calls. |

| Not all debts are dischargeable | Student loans, child support, and recent taxes typically survive bankruptcy. |

| Chapter 7 vs. Chapter 13 | Chapter 7 discharges in 3–6 months; Chapter 13 restructures debt over 3–5 years. |

| Post-discharge monitoring matters | Review credit reports within 30 days to catch and correct errors on discharged accounts. |

What I’ve learned from watching people go through this process

Most people who walk into a bankruptcy consultation carry two things: shame and misinformation. The shame is understandable but misplaced. The misinformation is the real problem.

The biggest misconception I see is that bankruptcy means losing everything. The data tells a different story. The vast majority of Chapter 7 cases are no-asset cases. People keep their cars, their furniture, and their homes. What they lose is the crushing weight of debt they were never going to repay anyway.

The second misconception is that bankruptcy is a last resort for people who failed. The Supreme Court has said since 1934 that the fresh start is the law’s gift to honest people in genuine financial distress. It is a tool, not a punishment. Using it correctly requires preparation, not desperation.

What I tell people is this: the outcome of your bankruptcy depends almost entirely on the work you do before you file. Incomplete schedules, missed deadlines, and undisclosed assets are the things that derail cases. The law itself is actually quite generous if you follow the rules.

Post-discharge financial discipline is where most people either succeed or slide back. The discharge gives you a clean slate on paper. Building something durable on that slate requires a budget, an emergency fund, and a realistic credit rebuilding plan. The legal process takes months. The financial recovery takes years. Both are worth it.

— Steven

How Wallacelawflorida can help you file with confidence

Facing debt is hard enough without trying to decode federal bankruptcy law on your own.

Wallacelawflorida provides personalized bankruptcy guidance for individuals and families in Boynton Beach and across South Florida. The attorneys at Wallacelawflorida assess your specific income, assets, and debt profile to determine whether Chapter 7 or Chapter 13 fits your situation, then guide you through every filing requirement from the means test to the discharge order. If you are ready to stop creditor calls and start rebuilding, local bankruptcy help from an experienced Florida attorney is the clearest next step. You can also download the free Florida bankruptcy eBook to understand your rights before your first consultation.

FAQ

What does fresh start bankruptcy mean in simple terms?

Fresh start bankruptcy is a legal process that eliminates or restructures your debts through a court discharge, ending creditor collection and releasing you from personal liability for eligible obligations.

How long does a fresh start bankruptcy take?

Chapter 7 typically concludes within 3–6 months from filing to discharge. Chapter 13 takes 3–5 years because it involves a supervised repayment plan before the final discharge is issued.

Will I lose my home or car in bankruptcy?

Most Chapter 7 cases are no-asset cases, meaning debtors keep exempt property including their primary vehicle and household goods. Florida’s homestead exemption also protects primary residence equity in many situations.

Does bankruptcy discharge all my debts?

No. Student loans, child support, alimony, and certain recent tax debts generally survive bankruptcy and remain your responsibility after discharge.

How long does bankruptcy stay on my credit report?

A Chapter 7 bankruptcy remains on your credit report for 10 years from the filing date. Chapter 13 remains for 7 years. Discharged debts must be reported as zero balance during that period.