TL;DR:

- A bankruptcy trustee is a court-appointed estate manager whose primary duty is to protect creditors’ interests, not the debtor’s.

- Their responsibilities vary by chapter, including asset liquidation in Chapter 7 and plan management in Chapter 13, with oversight from the U.S. Trustee Program.

A bankruptcy trustee is a court-appointed estate representative who manages the debtor’s assets primarily to protect creditors, not the debtor. This distinction matters enormously if you are considering filing. The trustee operates under the supervision of the U.S. Trustee Program and the bankruptcy court, with statutory authority defined by the Bankruptcy Code. Understanding the role of bankruptcy trustee before you file means fewer surprises, better preparation, and a cleaner path through the process. Whether you are looking at Chapter 7 liquidation or a Chapter 13 repayment plan, the trustee’s presence shapes every stage of your case.

What are the main bankruptcy trustee duties across chapters?

The trustee’s core function shifts depending on which chapter of the Bankruptcy Code governs your case. Trustees exercise statutory powers for unsecured creditors, appointed across Chapter 7, Chapter 12, Chapter 13, and some Chapter 11 cases. That fiduciary duty to creditors is the foundation of every decision the trustee makes.

Chapter 7 trustee responsibilities

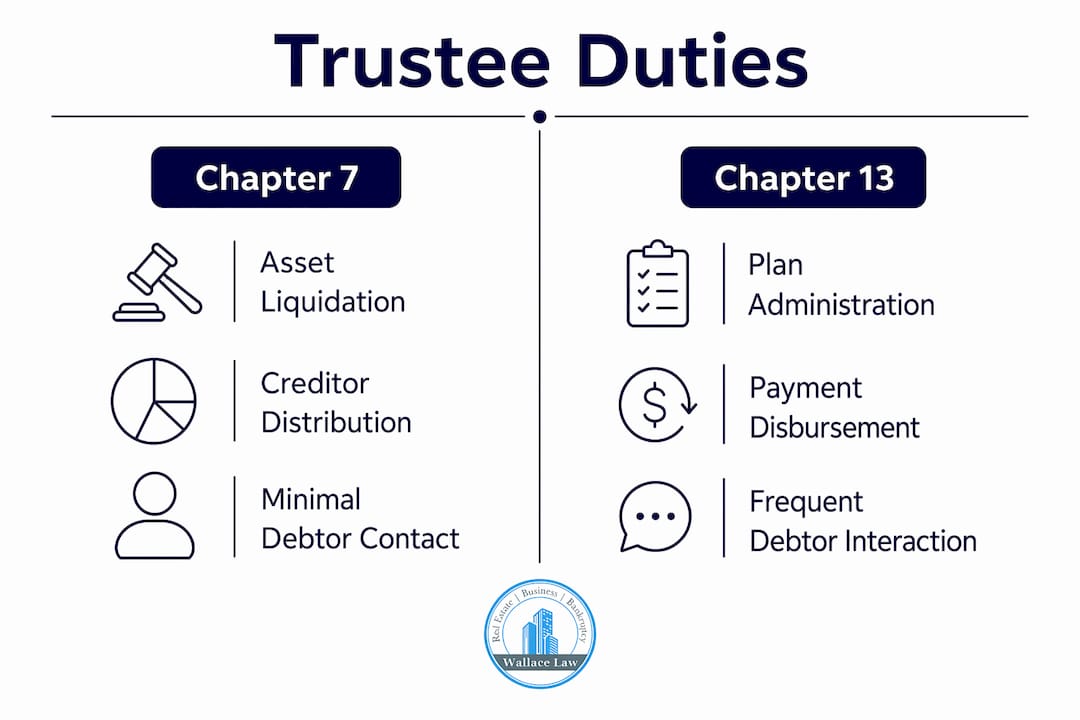

In Chapter 7, the trustee’s job is to liquidate non-exempt assets and distribute the proceeds to creditors according to the priority rules in the Bankruptcy Code. The trustee reviews your schedules, examines your financial history, and recovers any property that is not protected by exemptions. One fact that surprises many filers: the majority of Chapter 7 cases are “no-asset” cases where the trustee finds nothing to sell because all property falls within exemption limits. In those situations, the trustee’s role is largely administrative. You can review the full stages of Chapter 7 to understand how the trustee fits into each phase.

Chapter 13 trustee responsibilities

Chapter 13 trustees operate differently. Their primary function is plan administration and payment disbursement, not liquidation. You submit monthly payments to the trustee, who then distributes those funds to creditors according to your confirmed repayment plan. The trustee also monitors your compliance throughout the three to five year plan period. Missing payments or failing to report income changes can trigger a motion to dismiss or convert your case.

Chapter 12 trustees, used for family farmers and fishermen, follow a structure similar to Chapter 13 but with provisions tailored to seasonal income patterns.

Key bankruptcy trustee duties by chapter:

- Chapter 7: Review schedules, identify non-exempt assets, liquidate property, distribute proceeds, investigate pre-filing transfers

- Chapter 13: Evaluate proposed repayment plan, collect monthly payments, disburse funds to creditors, monitor ongoing compliance

- Chapter 12: Administer repayment plans for agricultural debtors, similar to Chapter 13 with seasonal income accommodations

- All chapters: Conduct the Section 341 meeting, verify debtor identity and financial disclosures, report fraud to the court

Pro Tip: Before filing, organize bank statements, tax returns, and property records for the past two years. Trustees routinely request these documents, and having them ready reduces delays and signals transparency.

How does the 341 meeting work and what is the trustee’s role?

The Section 341 meeting, often called the “meeting of creditors,” is the one point in most bankruptcy cases where you sit face to face with the trustee. The 341 meeting allows trustees and creditors to question you under oath about your finances, assets, and filings. Despite the formal name, creditors rarely attend. The trustee runs the meeting.

Here is what typically happens at a 341 meeting:

- Identity verification. The trustee confirms your government-issued ID and Social Security card before anything else.

- Oath administration. You are placed under oath, making every answer legally binding.

- Schedule review. The trustee asks about the accuracy of your bankruptcy petition, schedules, and statements of financial affairs.

- Asset and income questions. Expect direct questions about property you own, recent transfers, business interests, and income sources.

- Creditor questions. Any creditor present may ask questions, though this is uncommon in consumer cases.

- Closing or follow-up. The trustee either closes the meeting or requests additional documents if discrepancies arise.

“Discrepancies in debtor disclosures often trigger trustee scrutiny.” The trustee is trained to spot inconsistencies between your schedules and your stated income or lifestyle. A car listed as worth $3,000 that the trustee knows sells for $12,000 in your area will generate questions.

The meeting typically lasts five to fifteen minutes in straightforward consumer cases. The real risk is not the length. It is the legal weight of your answers. Trustees investigate assets and transfers near the bankruptcy filing date specifically to detect fraudulent conveyances or asset concealment. If you transferred property to a family member in the months before filing, expect the trustee to ask about it directly.

What is the oversight structure for bankruptcy trustees?

The U.S. Trustee Program, a component of the Department of Justice, is the administrative backbone of the bankruptcy system. It appoints and supervises private trustees, and it oversees more than 1,000 private trustees who collectively distribute about $8 billion annually. That scale explains why the oversight structure is so formalized.

| Trustee type | Appointment | Primary function |

|---|---|---|

| Private panel trustee | Appointed by U.S. Trustee | Administers individual Chapter 7 and 13 cases |

| Standing Chapter 13 trustee | Appointed by U.S. Trustee | Manages all Chapter 13 cases in a district |

| U.S. Trustee employee | Federal appointment | Supervises trustees, monitors cases, enforces compliance |

Private trustees are not government employees. They are attorneys or accountants who serve on a panel and receive compensation from the estate they administer. The U.S. Trustee Program acts as a watchdog for bankruptcy integrity, monitoring trustee conduct and stepping in when abuse or mismanagement occurs. The Program also litigates to enforce bankruptcy law, filing civil actions against trustees, debtors, or attorneys who violate the Bankruptcy Code.

This layered oversight matters for you as a debtor. It means the trustee assigned to your case is accountable to a federal program with enforcement authority. Trustees cannot favor one creditor over another, cannot accept gifts or payments outside the estate, and must exercise their fiduciary duties under Bankruptcy Code §704(a). That accountability protects you from arbitrary decisions, even though the trustee’s primary loyalty runs to creditors.

Pro Tip: If you believe a trustee is acting improperly or outside their authority, you can raise the issue with the U.S. Trustee’s office in your district. This is a formal complaint channel, not just a suggestion box.

How do trustee duties differ between Chapter 7 and Chapter 13?

The practical experience of dealing with a trustee looks very different depending on which chapter you file under. Understanding those differences helps you set realistic expectations and avoid common mistakes.

| Factor | Chapter 7 trustee | Chapter 13 trustee |

|---|---|---|

| Primary role | Asset liquidation and distribution | Plan administration and payment processing |

| Duration of contact | Brief, mostly at 341 meeting | Ongoing for 3 to 5 years |

| Debtor interaction | Minimal after 341 meeting | Regular, compliance-focused |

| Trustee compensation | Percentage of assets distributed | Percentage of plan payments |

| Outcome focus | Maximize creditor recovery from assets | Monitor plan completion and debtor compliance |

In Chapter 7, most debtors have minimal contact with the trustee after the 341 meeting. If your case is a no-asset case, the trustee files a report and the case moves toward discharge without further involvement. The Chapter 7 basics are worth reviewing if you are still deciding between chapters.

Chapter 13 is a different relationship entirely. The Chapter 13 trustee actively monitors compliance throughout the plan period, which means you will interact with the trustee’s office regularly. A common misconception is that the Chapter 13 trustee is your financial advocate or debt counselor. The trustee is not. Their job is to administer the plan and protect creditor interests. Effective communication with the trustee’s office, reporting income changes promptly and responding to document requests quickly, is what keeps your case on track.

What debtors often misunderstand about trustee involvement:

- The trustee does not negotiate your debts or advise you on financial decisions

- The trustee’s questions at the 341 meeting are not hostile. They are procedural

- In Chapter 13, missing a single payment without communicating with the trustee can trigger a motion to dismiss

- Trustees can and do uncover fraudulent transfers that occurred years before filing, not just recent ones

The differences between Chapter 7 and Chapter 13 extend well beyond trustee contact. But trustee involvement is one of the most practical factors to weigh when choosing a chapter.

Key takeaways

The bankruptcy trustee administers the estate for creditors, not for the debtor, and that single fact determines every interaction you will have throughout your case.

| Point | Details |

|---|---|

| Trustee loyalty runs to creditors | The trustee’s fiduciary duty is to maximize creditor recovery, not to protect debtor interests. |

| Chapter shapes trustee involvement | Chapter 7 trustees focus on liquidation; Chapter 13 trustees manage ongoing plan payments for years. |

| The 341 meeting is legally binding | Every answer you give under oath at the 341 meeting carries legal weight and can trigger further scrutiny. |

| U.S. Trustee Program provides oversight | Over 1,000 private trustees are supervised by the DOJ’s U.S. Trustee Program, which distributes about $8 billion annually. |

| Transparency prevents problems | Accurate, complete disclosures reduce trustee scrutiny and protect your path to discharge. |

What working with trustees taught me about bankruptcy preparation

After years of guiding clients through bankruptcy cases in Florida, I have seen one pattern repeat itself more than any other. Debtors who treat the trustee as an adversary create problems that did not need to exist. The trustee is not your enemy. The trustee is also not your ally. They are a neutral administrator with a specific legal job, and the best thing you can do is make that job easy.

The debtors who struggle are the ones who omit assets thinking the trustee will not notice, or who transfer property to relatives weeks before filing hoping to protect it. Trustees are experienced at spotting exactly these moves. The trustee’s discretion in prioritizing duties means they can dig as deep as the case warrants, and a suspicious schedule gives them every reason to dig.

What I tell every client before their 341 meeting: answer the question asked, nothing more and nothing less. Do not volunteer information that was not requested, but never withhold what is asked. That discipline, combined with complete and accurate schedules, is the single most effective way to move through a bankruptcy case without complications.

The other thing debtors underestimate is how much the trustee’s behavior in Chapter 13 depends on your behavior. Effective debtor-trustee communication prevents plan failures. If your income drops, tell the trustee’s office before you miss a payment. If you receive an inheritance or a tax refund, report it. Trustees who see proactive communication are far less likely to file motions that derail your case.

— Steven

Get expert bankruptcy guidance from Wallacelawflorida

Understanding the trustee’s role is one piece of a much larger puzzle. Filing bankruptcy without legal representation means navigating trustee interactions, exemption planning, and court deadlines on your own, and mistakes at any stage can cost you the discharge you need.

Wallacelawflorida provides personalized bankruptcy representation for individuals and families in Boynton Beach and throughout South Florida. The attorneys at Wallace Law know Florida’s exemption laws, understand how local trustees operate, and will prepare you for every stage of your case, from the 341 meeting to final discharge. Whether you are weighing Chapter 7 or Chapter 13, start with a conversation. Visit the Wallace Law bankruptcy practice page to learn more, or download the free Florida bankruptcy eBook to build your foundation before your first consultation.

FAQ

What is the role of a bankruptcy trustee?

A bankruptcy trustee is a court-appointed administrator who manages the debtor’s estate on behalf of creditors, not the debtor. The trustee’s duties include reviewing financial disclosures, liquidating non-exempt assets in Chapter 7, and overseeing repayment plans in Chapter 13.

Does the bankruptcy trustee represent the debtor?

No. The trustee’s fiduciary duty runs to creditors, particularly unsecured creditors. The trustee administers the estate to maximize creditor recovery and does not provide legal advice or advocacy for the debtor.

What happens at the 341 meeting of creditors?

The trustee places the debtor under oath and asks questions about income, assets, debts, and the accuracy of the bankruptcy petition. The meeting typically lasts five to fifteen minutes, and creditors rarely attend in consumer cases.

How do I choose a bankruptcy trustee?

Debtors do not choose their trustee. The U.S. Trustee Program assigns a private panel trustee or standing trustee to your case based on the district and chapter filed. Your attorney can help you understand who is assigned and what to expect from that trustee’s typical practices.

Can a trustee take all of my property?

A Chapter 7 trustee can only liquidate property that is not protected by state or federal exemptions. Florida offers significant exemptions, including homestead protection. Most consumer Chapter 7 cases are no-asset cases where the trustee sells nothing because all property falls within exemption limits.