TL;DR:

- A Florida professional corporation is a specialized entity for licensed professionals, offering limited liability while maintaining strict legal and licensing compliance. Shareholders must hold active licenses in the same profession, and the corporation can only provide the services it was formed to deliver. Proper formation, governance, and buyout agreements are critical to protecting personal assets and ensuring legal accountability.

A professional corporation in Florida is a specialized business entity formed exclusively by licensed professionals to deliver regulated services under Florida Statutes Chapter 621. Known formally as a Professional Association (P.A.), this structure differs from a standard corporation in one critical way: every shareholder must hold an active license in the same profession. Attorneys, physicians, accountants, and architects are among the professionals who use this structure. It provides limited liability protection for general business debts while keeping each professional personally responsible for their own conduct. Understanding what is professional corporation Florida means understanding both its protections and its firm legal boundaries.

What is a professional corporation in Florida?

A Florida professional corporation is defined under Chapter 621 of the Florida Statutes as a corporation organized solely to render professional services by licensed individuals. The law requires that all shareholders be licensed professionals authorized to provide the same category of services. A medical P.A., for example, cannot have a non-physician as a shareholder. This is not a technicality. It is a foundational rule that shapes every aspect of how the entity operates.

The Florida professional corporation definition separates this structure from a general business corporation or a limited liability company. A standard corporation can have any shareholder. A P.A. cannot. This restriction exists because the state wants to preserve professional accountability. Licensing boards retain oversight authority over the entity’s conduct, not just the individual professionals within it. That dual layer of oversight is what makes the P.A. both more regulated and more credible than a sole proprietorship or informal partnership.

Florida law also restricts a P.A. to providing only the licensed service it was formed to deliver. A common misconception is that a professional corporation allows business diversification into unrelated services. It does not. A law P.A. cannot pivot into real estate consulting as a corporate activity. That boundary keeps the entity focused and legally clean.

How to form a professional corporation in Florida

Forming a Florida P.A. follows a defined process. Each step matters because errors in formation can create compliance problems with both the Florida Division of Corporations and the relevant professional licensing board.

-

Search and reserve your corporate name. The name must include “P.A.” or “Professional Association.” The naming requirement signals the entity’s regulated status to clients and the public. Names cannot be misleading about the services offered.

-

Prepare and file Articles of Incorporation. You file these with the Florida Division of Corporations. The state filing fee is approximately $70. Processing is typically fast, but accuracy in the articles is non-negotiable.

-

Appoint a registered agent. Florida law requires every corporation to maintain a registered agent with a physical address in the state. The agent receives legal documents on behalf of the corporation.

-

Establish a principal office. The corporation must have a designated principal place of business in Florida.

-

Draft corporate bylaws. Bylaws govern internal operations, shareholder rights, and meeting procedures. They must align with both Chapter 621 and Chapter 607 of the Florida Business Corporation Act.

-

Obtain licensing board approval. Your relevant professional board may require notification or approval of the entity before it begins operating. Skipping this step is a common and costly mistake.

Pro Tip: Use a Florida business formation checklist to track each filing requirement before you submit anything to the state. Missing one step can delay your ability to practice under the new entity.

Who can own and govern a Florida P.A.?

Ownership eligibility is the most restrictive feature of a Florida professional corporation. All shareholders must be licensed in the same profession and authorized to render the same services. This rule applies at all times, not just at formation.

The professions that most commonly use the P.A. structure in Florida include:

- Medicine and dentistry: Physicians and dentists frequently form P.A.s to separate personal assets from practice liabilities.

- Law: Florida attorneys operating as a firm often use the P.A. designation.

- Accounting: CPAs use P.A.s to formalize their practices and build client credibility.

- Architecture and engineering: Licensed design professionals use P.A.s for project-based liability management.

- Mental health and counseling: Licensed therapists and psychologists use the structure to meet state practice requirements.

Share transfers create the most complex governance challenges. When a shareholder retires, loses their license, or dies, the same profession rule creates immediate complications. Shares cannot simply transfer to a family member or outside investor. Without a shareholder agreement that includes buyout provisions, disputes over share valuation become expensive and legally tangled.

Pro Tip: Draft a shareholder agreement before you file your Articles of Incorporation. Include specific buyout triggers for retirement, license revocation, disability, and death. Fixing this after a dispute starts costs far more than addressing it upfront.

The Florida Business Corporation Act and Chapter 621 both govern the entity, and licensing boards hold authority to regulate conduct tied to professional licenses. Non-compliance can result in penalties against the corporation and against individual license holders within it.

What liability protection does a Florida P.A. actually provide?

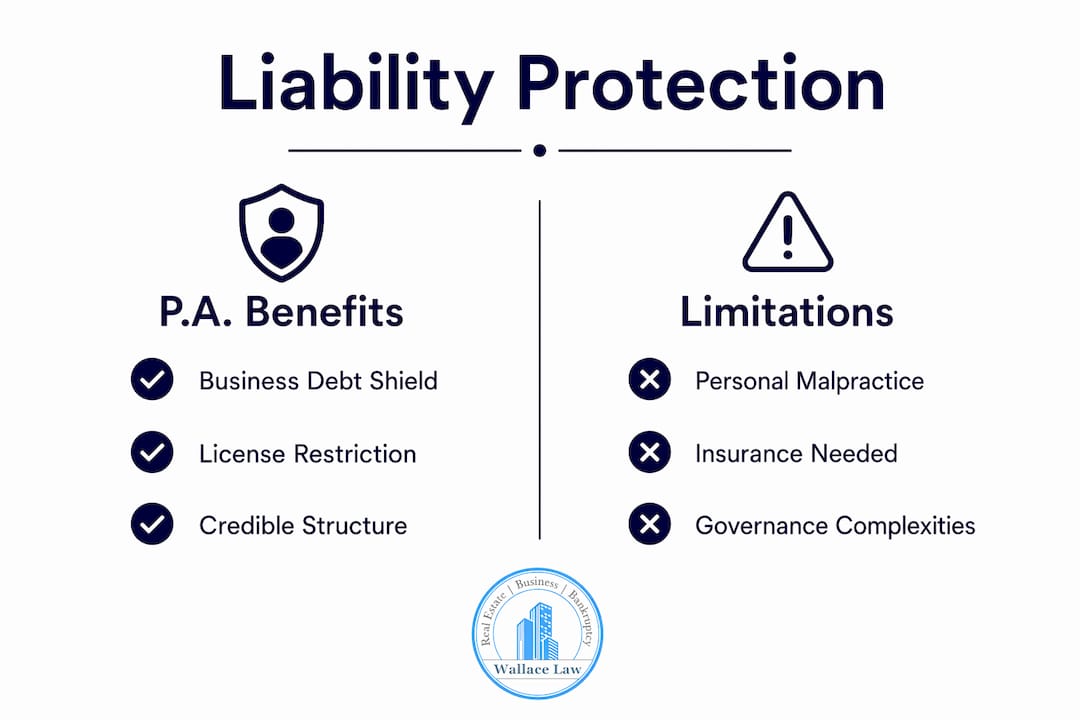

The liability picture for a Florida professional corporation is more limited than most professionals expect. Here is what the structure does and does not protect:

- Protected: Personal assets from general business debts, such as office leases, vendor contracts, and equipment loans.

- Protected: Shareholders from the malpractice of other shareholders, in most circumstances.

- Not protected: Each professional’s personal liability for their own malpractice or negligence.

- Not protected: A supervising professional’s liability for errors made by associates under their direct supervision.

- Not protected: Any conduct that violates professional licensing standards, regardless of corporate structure.

Professional corporations shield personal assets from business liabilities but leave each professional fully exposed for their own errors. That distinction matters enormously when a malpractice claim arrives.

Compared to a sole proprietorship, a P.A. offers meaningful protection for business debts. Compared to an LLC, the protection is similar for business obligations but the regulatory burden is heavier. The professional corporation vs LLC Florida comparison often comes down to licensing board requirements. Some Florida licensing boards require or strongly prefer the P.A. structure for certain professions. An LLC may not satisfy those board requirements even if it offers comparable liability protection.

Adequate professional liability insurance is not optional. The P.A. structure does not replace malpractice coverage. It supplements it by protecting non-malpractice business assets.

Tax treatment for Florida professional corporations

Tax planning is where the P.A. structure offers real financial advantages, but only if you make the right elections at the right time.

-

Default C-corporation status. A Florida P.A. is taxed as a C-corporation by default. That means the corporation pays federal income tax on its profits, and shareholders pay personal income tax on dividends. This double taxation is the primary reason most small professional corporations elect S-corporation status.

-

S-corporation election. You elect S-corp status by filing IRS Form 2553 within 75 days of formation or by march 15 of the following tax year. S-corp status passes income directly to shareholders, avoiding double taxation.

-

S-corp eligibility requirements. The corporation must have 100 or fewer shareholders, all shareholders must be U.S. citizens or residents, and the entity can have only one class of stock. Most small Florida P.A.s qualify easily.

-

Self-employment tax reduction. Under S-corp status, shareholders who work in the business pay themselves a reasonable salary. Profits above that salary pass through as distributions, which are not subject to self-employment tax. This is a meaningful annual savings for high-earning professionals.

-

Financial planning discipline required. The S-corp structure requires payroll setup, quarterly tax deposits, and annual corporate tax returns. The administrative cost is real. For most professionals earning above a moderate income threshold, the tax savings outweigh the added overhead.

| Tax classification | Double taxation | Self-employment tax on distributions | Complexity |

|---|---|---|---|

| C-corporation (default) | Yes | No | Moderate |

| S-corporation (elected) | No | No | Higher |

| Sole proprietorship | No | Yes (on all income) | Low |

The tax implications of professional corporations in Florida reward professionals who plan early. Waiting until year two to elect S-corp status means paying C-corp taxes in year one unnecessarily.

Key Takeaways

A Florida professional corporation provides limited liability for business debts and a credible legal structure, but it does not protect professionals from personal malpractice liability and requires strict compliance with Chapter 621 and professional licensing board rules.

| Point | Details |

|---|---|

| Ownership restriction | All shareholders must hold an active license in the same profession at all times. |

| Formation cost | Filing Articles of Incorporation with the Florida Division of Corporations costs approximately $70. |

| Liability boundary | A P.A. protects personal assets from business debts but not from personal malpractice claims. |

| Tax election deadline | File IRS Form 2553 within 75 days of formation to elect S-corporation status and avoid double taxation. |

| Shareholder agreement | A buyout agreement is critical before formation to handle retirement, death, or license loss. |

Why most professionals misread what a P.A. actually does for them

The biggest mistake I see professionals make is treating the P.A. as a liability shield in the same way a tech entrepreneur treats an LLC. It is not. The credibility and structure a P.A. provides are real and valuable, but the malpractice exposure never goes away. Professionals who form a P.A. and then reduce their malpractice insurance coverage are taking on more risk, not less.

The second mistake is underestimating the governance complexity. Florida P.A.s must align their corporate documents with both Chapter 621 and Chapter 607 simultaneously. Most attorneys who draft generic corporate bylaws miss the Chapter 621 overlay entirely. That gap creates compliance exposure that only surfaces during a licensing board audit or a shareholder dispute.

The third mistake is skipping the shareholder agreement. I have seen practices dissolve messily because one partner retired and no one had planned for share transfer. The “same profession” rule makes this a uniquely sharp problem for P.A.s. A well-drafted agreement with clear buyout triggers and valuation methods prevents that outcome. Professionals who invest in ADA compliance and regulatory alignment from the start build practices that survive transitions.

The strategic upside of the P.A. structure is real. It signals to clients that your practice operates under formal legal and regulatory oversight. That perception builds trust in ways that a sole proprietorship simply cannot match. For new Florida professionals considering formation, my recommendation is straightforward: get the shareholder agreement right before you file anything else.

— Steven

How Wallacelawflorida helps Florida professionals get formation right

Florida professionals forming a P.A. face a layered set of requirements that generic online filing services cannot address. Wallacelawflorida works directly with business owners and licensed professionals in Boynton Beach and surrounding areas to handle entity formation with the precision Florida law demands.

The team at Wallacelawflorida understands the intersection of Chapter 621 compliance, licensing board requirements, and corporate governance. Whether you are forming a new P.A. or correcting a compliance gap in an existing one, the firm’s business law services cover the full formation process, from Articles of Incorporation through shareholder agreements and ongoing regulatory compliance. Personal attention from attorneys who know Florida’s professional corporation rules is the difference between a properly formed entity and one that creates problems at the worst possible moment.

FAQ

What does P.A. stand for in Florida business law?

P.A. stands for Professional Association, which is the Florida term for a professional corporation formed under Chapter 621 of the Florida Statutes. It is functionally equivalent to a professional corporation (P.C.) in other states.

Can a non-licensed person own shares in a Florida P.A.?

No. All shareholders must hold an active professional license in the same field as the corporation’s services. A non-licensed investor cannot hold equity in a Florida P.A.

How does a professional corporation differ from an LLC in Florida?

A P.A. restricts ownership to licensed professionals in the same field and faces oversight from professional licensing boards, while an LLC has no such ownership restrictions. Some Florida licensing boards require the P.A. structure for specific professions, making the LLC an ineligible option in those cases.

Does forming a P.A. eliminate malpractice liability?

No. A professional corporation does not protect individual professionals from personal malpractice claims. Each professional remains personally liable for their own errors and, in some cases, for errors made by supervised associates.

What happens if a Florida P.A. shareholder loses their license?

The shareholder must transfer or surrender their shares because unlicensed ownership violates Chapter 621. A shareholder agreement with buyout provisions is the standard mechanism for managing this transition without litigation.