TL;DR:

- Florida business sale taxes mainly apply to tangible assets transferred during a sale rather than the sale proceeds. Sellers benefit from no state income tax on gains but must manage sales and real estate taxes, along with federal obligations, carefully before closing. Early preparation, including obtaining a Tax Clearance Certificate and proper purchase price allocation, is essential to avoid unexpected liabilities and maximize net proceeds.

Florida business sale taxes apply primarily to tangible personal property transferred during a sale, not to the sale proceeds themselves. Understanding how Florida business sale taxes work separates sellers who walk away with maximum net proceeds from those who face unexpected tax bills at closing. Florida imposes no state income tax on business sale gains, but the Florida Department of Revenue, the IRS, and successor liability rules all create real obligations that affect deal structure, timing, and final price. Wallacelawflorida works with Florida business owners to navigate every layer of this process before a deal closes.

How do Florida business sale taxes work?

Florida taxes the transfer of assets in a business sale, not the profit from the sale. That distinction matters more than most sellers realize.

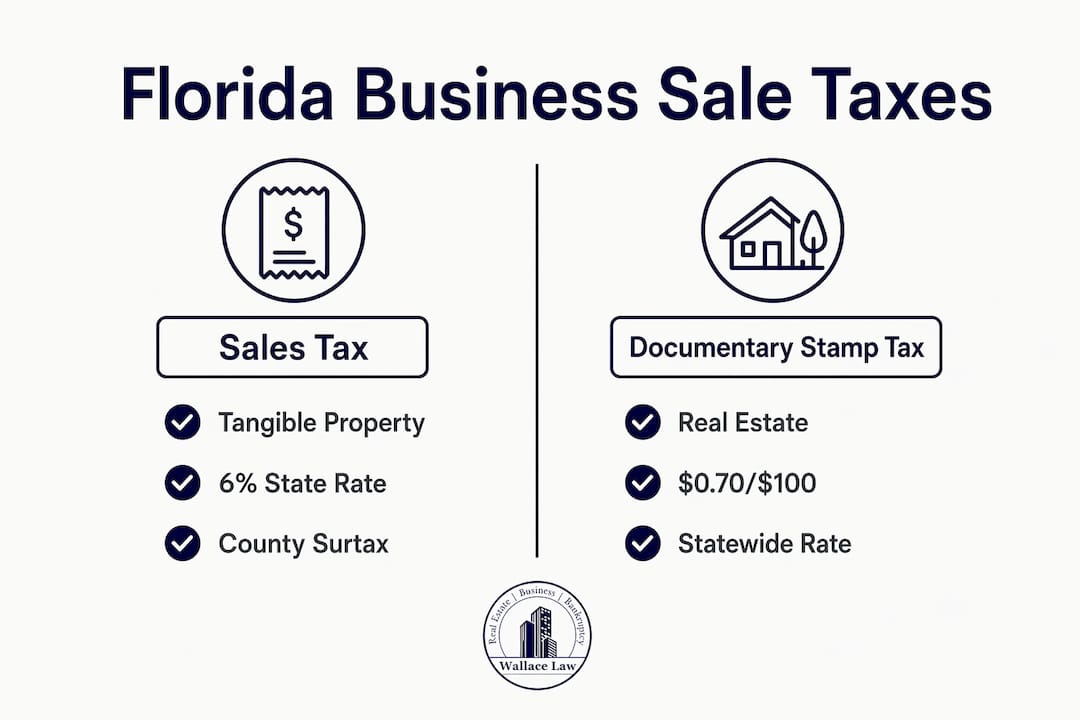

Florida’s base sales tax rate on tangible personal property is 6%, with discretionary county surtaxes added on top based on where the property is delivered or used. That means equipment, inventory, and furniture transferred in a business sale all trigger sales tax. The county surtax varies by location, so a sale in Miami-Dade carries a different total rate than one in Palm Beach County.

Florida does not impose a state income tax on business sale proceeds. That is a genuine advantage for sellers compared to states like California or New York. Federal taxes, however, still apply in full, and they often represent the largest tax burden in any Florida business sale.

Two regulatory bodies govern the process. The Florida Department of Revenue handles sales tax, documentary stamp tax, and tax clearance certificates. The IRS handles federal capital gains, depreciation recapture, and net investment income tax. Sellers who treat these as separate tracks rather than one coordinated plan often pay more than necessary.

What types of Florida taxes apply when selling a business?

Florida business sales can trigger three distinct state-level taxes, each applying to a different part of the transaction.

Sales tax on tangible personal property

Sales tax applies to physical assets: equipment, machinery, vehicles, inventory, and furniture. The state rate is 6%, and county surtaxes vary by destination. The buyer typically pays sales tax at closing, but the seller remains responsible if the buyer fails to remit it.

Intangible assets are exempt. Goodwill, customer lists, non-compete agreements, and intellectual property do not trigger Florida sales tax. That exemption makes purchase price allocation a critical negotiating point, which is covered in detail below.

Documentary stamp tax on real estate

Documentary stamp tax applies when real estate is part of the business sale. The rate is $0.70 per $100 of consideration. This tax is separate from sales tax and applies only to the real property component of the transaction. A business sale that includes a building or land will trigger this tax on the real estate value assigned in the purchase agreement.

Florida state income tax: the good news

Florida does not tax business sale proceeds as income. Sellers keep 100% of their gain free from state income tax. That benefit applies to asset sales, stock sales, and membership interest transfers alike.

Here is a quick reference for the three Florida-level taxes:

| Tax type | What it applies to | Rate |

|---|---|---|

| Sales tax | Tangible personal property | 6% state + county surtax |

| Documentary stamp tax | Real estate transfers | $0.70 per $100 |

| State income tax | Business sale proceeds | None |

Federal taxes are a separate matter entirely and carry the heaviest financial weight for most sellers.

How does successor liability affect Florida business sales?

Successor liability is one of the most overlooked risks in Florida asset sales. Florida law allows buyers to be held liable for a seller’s unpaid sales taxes when they purchase tangible business assets. The buyer does not have to know about the unpaid taxes. The liability transfers automatically unless the buyer takes specific steps to protect themselves.

The primary protection is the Tax Clearance Certificate issued by the Florida Department of Revenue. This certificate confirms that the seller has no outstanding sales tax obligations. Without it, a buyer who purchases a business with $50,000 in unpaid sales taxes inherits that debt on closing day.

How to obtain a tax clearance certificate

The process follows a clear sequence:

- Submit the application. The seller or their attorney files Form DR-1 with the Florida Department of Revenue, requesting a tax clearance review.

- Provide business records. The Department reviews sales tax returns, payment history, and any open audits or assessments.

- Await the review period. The Department issues either a clearance certificate or a notice of outstanding liability.

- Resolve any open balances. If taxes are owed, they must be paid or formally disputed before the certificate is issued.

- Present the certificate at closing. The buyer’s counsel confirms the certificate before funds are released.

Buyers’ counsel typically requires the application to be filed within 7 days of the Letter of Intent signing. Delays in starting this process are one of the most common reasons Florida business sales miss their closing dates.

Pro Tip: Start the tax clearance application the same week you sign the Letter of Intent. The Florida Department of Revenue review can take several weeks, and waiting until the final stretch of due diligence puts the entire closing at risk.

What is the role of purchase price allocation in Florida business sales?

Purchase price allocation determines how the total sale price is divided among the different asset classes being transferred. That division directly controls which taxes apply and at what rates. This is where sellers and buyers often have directly opposing interests.

Intangible assets like goodwill are exempt from Florida sales tax. Tangible assets are not. A seller who allocates more of the purchase price to goodwill reduces the sales tax burden for the buyer and may shift more of their own gain into long-term capital gains territory, which carries lower federal rates. Buyers, on the other hand, prefer allocations to depreciable assets because those assets generate future tax write-offs.

IRS Form 8594 and consistent reporting

Both parties must report the same allocation on IRS Form 8594. If the buyer and seller file inconsistent allocations, the IRS flags the discrepancy and may audit both returns. The purchase agreement should specify the agreed allocation in writing, and both parties should confirm their Form 8594 filings match before submitting.

Here is how allocation strategy differs by party:

| Party | Preferred allocation | Reason |

|---|---|---|

| Seller | Higher allocation to goodwill | Capital gains rates apply; no Florida sales tax |

| Buyer | Higher allocation to depreciable assets | Faster write-offs reduce future taxable income |

Pro Tip: Negotiate the purchase price allocation as a formal term in the purchase agreement, not as an afterthought. An attorney experienced in Florida business transactions can help you structure the allocation to reduce your total tax exposure while keeping the deal attractive to the buyer.

How do federal taxes impact Florida business sales?

Federal taxes represent the largest financial variable in most Florida business sales. Florida’s lack of a state income tax does not reduce federal obligations by a single dollar.

The key federal taxes that apply to Florida business sellers include:

- Long-term capital gains tax. Profits on assets held longer than one year qualify for long-term rates. Federal long-term capital gains combined with the Net Investment Income Tax can reach an effective rate of 23.8% for high earners. That rate applies to goodwill and other capital assets.

- Depreciation recapture. Equipment and real estate that were depreciated over time generate recapture income when sold. The IRS taxes recapture as ordinary income, not capital gains. For sellers with heavily depreciated assets, this can be a significant surprise.

- Net Investment Income Tax (NIIT). The NIIT adds 3.8% on top of capital gains for sellers whose income exceeds the applicable thresholds. This tax applies regardless of how the business is structured.

- Ordinary income tax on certain assets. Inventory and accounts receivable are taxed as ordinary income, not capital gains. Allocation of purchase price to these assets increases the seller’s ordinary income tax burden.

Asset sale vs. stock sale: the decision that changes everything

The choice between an asset sale and a stock sale fundamentally changes the tax outcome for both parties. In an asset sale, the seller pays tax on each asset class individually, often at mixed rates. In a stock sale, the seller typically pays capital gains on the entire proceeds. Buyers almost always prefer asset sales because they get a stepped-up basis. Sellers often prefer stock sales for the cleaner capital gains treatment.

Planning strategies worth knowing

Several planning tools can reduce the federal tax burden for Florida sellers:

- Installment sales spread the gain over multiple years, potentially keeping the seller in a lower tax bracket each year.

- Qualified Opportunity Zone investments allow sellers to defer and potentially reduce capital gains by reinvesting proceeds into designated Florida zones.

- Timing the close relative to the tax year can shift income and affect which year’s rates apply.

Businesses that prepare 12–24 months ahead of a sale commonly achieve significantly better outcomes, both in sale price and tax efficiency. Early planning gives sellers time to restructure assets, clean up financials, and choose the right sale structure.

Key Takeaways

Florida business sales trigger sales tax on tangible assets at 6% plus county surtax, no state income tax on proceeds, and significant federal tax obligations that require early, coordinated planning.

| Point | Details |

|---|---|

| Sales tax on tangible assets | Florida applies 6% state sales tax plus county surtax to equipment, inventory, and furniture transfers. |

| No Florida state income tax | Sellers owe zero Florida income tax on business sale proceeds, a key advantage over most other states. |

| Successor liability risk | Buyers inherit unpaid seller sales taxes without a Tax Clearance Certificate from the Florida Department of Revenue. |

| Purchase price allocation | Allocating more to goodwill reduces sales tax and may lower federal rates; both parties must file matching IRS Form 8594. |

| Federal taxes dominate | Capital gains, depreciation recapture, and the 3.8% NIIT can combine to reach 23.8% for high earners. |

What I’ve learned from watching Florida sellers leave money on the table

Most sellers I work with understand that Florida has no state income tax. What surprises them is how much the structure of the deal determines their actual tax bill. Two sellers with identical businesses and identical sale prices can walk away with very different net proceeds based entirely on how the purchase price is allocated and whether they chose an asset sale or a stock sale.

The other pattern I see repeatedly is sellers who treat the tax clearance certificate as a formality. It is not. I have watched deals stall for weeks because the seller’s team waited until the final days of due diligence to file with the Florida Department of Revenue. Buyers get nervous when closing timelines slip, and nervous buyers sometimes walk.

The sellers who do best are the ones who start preparing 12 to 24 months before they list. They clean up commingled personal and business expenses, which is one of the first things a buyer’s accountant will flag. They work with a Florida-experienced attorney and a CPA together, not separately. And they negotiate purchase price allocation as a real term in the deal, not as a footnote.

Florida’s tax environment genuinely favors sellers. No state income tax is a real advantage. But that advantage only shows up in your bank account if the deal is structured correctly from the start.

— Steven

Wallacelawflorida: legal support for your Florida business sale

Selling a business in Florida involves more moving parts than most owners expect. Sales tax compliance, successor liability, documentary stamp tax on real estate, and purchase price allocation all require careful legal attention before the deal closes.

Wallacelawflorida helps Florida business owners and buyers handle every legal step of the transaction, from drafting the purchase agreement to securing the Tax Clearance Certificate from the Florida Department of Revenue. The firm’s attorneys are experienced with Florida business law and understand the local regulations that affect deals in Boynton Beach and the surrounding South Florida area. If you are preparing to sell or buy a Florida business, contact Wallacelawflorida for a consultation before you sign anything.

FAQ

Does Florida charge sales tax on all business assets?

Florida sales tax applies only to tangible personal property such as equipment, inventory, and furniture. Intangible assets like goodwill, customer lists, and non-compete agreements are exempt from Florida sales tax.

What is a Tax Clearance Certificate and do I need one?

A Tax Clearance Certificate is a document from the Florida Department of Revenue confirming the seller has no unpaid sales tax obligations. Buyers require it to avoid inheriting the seller’s unpaid tax liability under Florida’s successor liability law.

How do I calculate the sales tax on a Florida business sale?

Apply the 6% Florida state rate plus the applicable county surtax to the value of tangible personal property being transferred. The county surtax is destination-based, so the rate depends on where the assets will be used after the sale.

Does selling an LLC in Florida trigger different taxes?

Selling an LLC through a membership interest transfer is treated as a stock sale for tax purposes, which generally avoids Florida sales tax on the assets. However, federal capital gains and the NIIT still apply to the seller’s gain from the membership interest transfer.

When should I start the tax clearance process?

File the tax clearance application with the Florida Department of Revenue within 7 days of signing the Letter of Intent. Starting early prevents the review period from delaying your closing timeline.