TL;DR:

- Filing a timely and comprehensive Answer to a foreclosure complaint is crucial to protect your legal rights and prevent a default judgment.

- It must address all allegations, raise applicable defenses like lack of standing or TILA violations, and be properly formatted and served; skipping these steps can result in losing your home.

A foreclosure defense response filing is a formal written Answer you submit to court that directly challenges your lender’s claims and asserts your legal rights to delay or prevent foreclosure. Most homeowners don’t realize they have 20 to 30 days from being served to file this document. Miss that window and the court can enter a default judgment against you, handing the lender a clear path to take your home. The Answer is your first and most powerful legal move. Filing it correctly, with the right defenses included, is what separates homeowners who lose their homes quickly from those who buy time, negotiate, or win outright.

What are the key legal requirements for a foreclosure defense response filing?

The formal industry term for this document is an Answer to Foreclosure Complaint, though homeowners and attorneys also call it a foreclosure defense response. Understanding the difference between judicial and nonjudicial foreclosure is the first thing you need to get right, because it determines whether you file an Answer at all.

In a judicial foreclosure state like Florida, the lender must sue you in court. That lawsuit is your opening. The burden of proof rests on the lender, which means you can force them to prove every claim they make. In a nonjudicial foreclosure state, you bear the burden and must initiate your own lawsuit to challenge the process. Florida homeowners are in a stronger position than most.

Once you are served with the foreclosure complaint, the clock starts immediately. Missing the 20 to 30 day deadline typically results in a default judgment, which eliminates all your defenses and accelerates the sale. That outcome is entirely avoidable with prompt action.

Your Answer must address every numbered allegation in the complaint. You respond to each one by admitting it, denying it, or stating you lack sufficient information to admit or deny. Failing to raise affirmative defenses in the Answer can permanently waive those defenses under 2026 rules. You do not get a second chance to add them later.

Pro Tip: Start a communication log the moment you receive foreclosure papers. Record every call with your servicer, including the date, time, representative’s name, and what was said. These communication logs become critical evidence if your servicer violates federal loss mitigation rules.

Here is a quick reference for what you need to gather before filing:

| Document or Step | Why It Matters |

|---|---|

| Original mortgage and promissory note | Verifies who actually holds your loan |

| All servicer correspondence | Supports defenses based on improper notice or TILA violations |

| Payment history records | Challenges the lender’s claimed default amount |

| Assignment of mortgage documents | Reveals potential standing defects |

| Court filing deadline (from summons) | Determines your Answer due date |

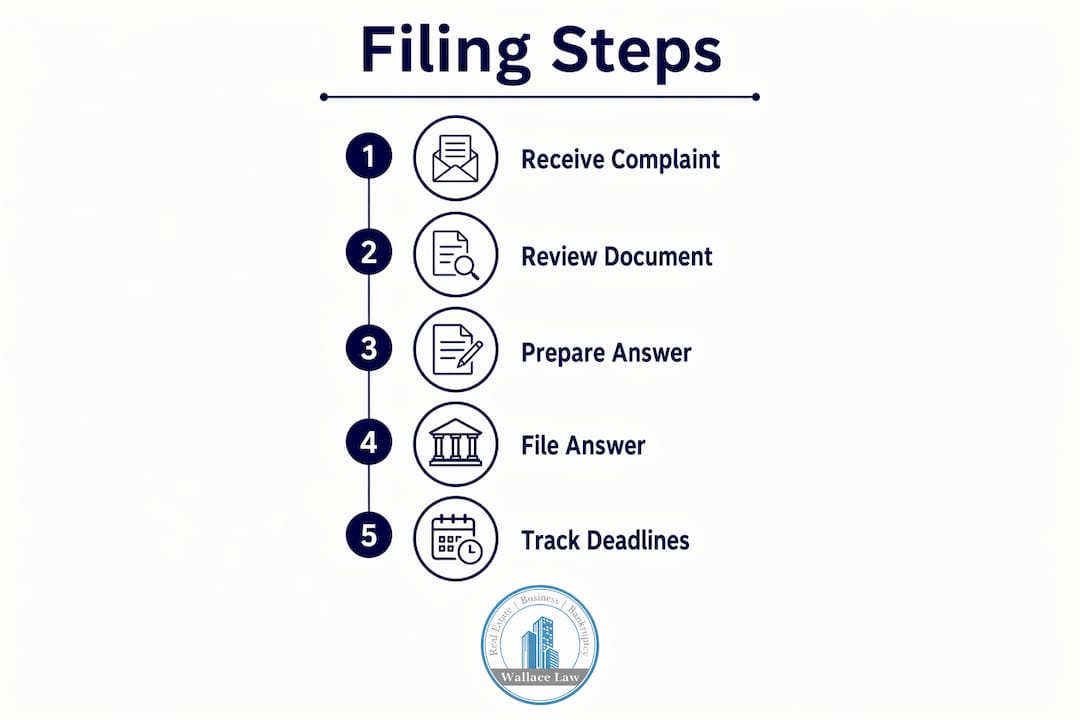

How to draft and file your foreclosure defense Answer step-by-step

Filing a foreclosure defense response is procedural work. Every step matters, and skipping one can cost you the case before it starts.

-

Review the complaint in full. Read every numbered paragraph carefully. Note the date you were served, the name of the plaintiff (often a bank or loan servicer), and every specific claim they make about your loan, the default, and the amount owed.

-

Draft your responses paragraph by paragraph. For each allegation, write a response that admits, denies, or states insufficient information. Do not leave any allegation unanswered. Courts treat silence as an admission.

-

Identify your affirmative defenses. This is where most homeowners either protect themselves or leave money on the table. Common defenses include lack of standing, improper service of process, Truth in Lending Act (TILA) violations, and statute of limitations. List every defense that applies to your situation, even if you are unsure. An attorney can help you narrow them down.

-

Format the Answer according to court rules. Florida courts require specific formatting, including a caption with the case number, the court name, and the parties’ names. The document must be signed and dated. Check the local court’s self-help resources or the Florida Rules of Civil Procedure for exact formatting requirements.

-

File with the court clerk and serve the lender’s attorney. You file the original Answer with the clerk of court and send a copy to the plaintiff’s attorney by the method specified in the summons (usually certified mail or electronic service). Keep proof of both.

Pro Tip: If you file a motion to dismiss before your Answer, know that motion denials require you to file a formal Answer within 10 to 14 days or risk automatic default. A motion to dismiss pauses the clock but does not replace the Answer.

| Filing Step | Common Mistake to Avoid |

|---|---|

| Responding to allegations | Leaving any allegation unanswered |

| Raising affirmative defenses | Omitting defenses you plan to raise later |

| Formatting the document | Using incorrect case caption or missing signature |

| Filing with the clerk | Filing without keeping a date-stamped copy |

| Serving the lender’s attorney | Using an improper service method |

What are the most effective foreclosure defense strategies?

A well-drafted Answer does more than deny claims. It raises affirmative defenses that put the lender on the defensive and create leverage for negotiation or dismissal. Here are the most effective strategies Florida homeowners use in 2026:

-

Lack of standing. Mortgage servicers sometimes file foreclosure cases with defective paperwork, including invalid assignments and broken endorsement chains. If the plaintiff cannot prove it owns or holds your note, it has no legal right to foreclose. Scrutinizing every assignment document is worth the effort.

-

Loss mitigation application. Under federal mortgage servicing rules, submitting a complete loss mitigation application more than 37 days before a scheduled foreclosure sale legally stops the sale until the servicer completes its review. This is one of the most powerful procedural tools available to homeowners right now.

-

TILA and RESPA violations. If your servicer failed to provide required disclosures or misapplied your payments, those violations can support both a defense and a counterclaim. The Truth in Lending Act and the Real Estate Settlement Procedures Act both create enforceable rights.

-

Dual tracking violations. Federal rules prohibit servicers from advancing a foreclosure while a loss mitigation application is under review. If your servicer did this, you have grounds to challenge the foreclosure timeline directly.

-

FDCPA and TCPA counterclaims. If a debt collector harassed you with repeated calls or used deceptive collection tactics, the Fair Debt Collection Practices Act and the Telephone Consumer Protection Act allow you to file counterclaims. These can shift negotiating power significantly.

-

Bankruptcy protection. Filing for bankruptcy triggers an automatic stay, which immediately halts all foreclosure proceedings. Chapter 13 specifically allows you to propose a repayment plan to catch up on missed payments and keep your home. Learn more about bankruptcy as a defense tool before ruling it out.

Pro Tip: Mortgage servicers prefer to avoid costly foreclosure sales. That gives you real negotiating leverage. Consistent communication and filing complaints with the Consumer Financial Protection Bureau (CFPB) when servicers violate rules can force compliance and open the door to loan modifications.

How to respond if you face a motion for summary judgment

Filing your Answer is not the end of the process. After the Answer, the case moves into discovery, where both sides exchange documents and take depositions. Many lenders then file a motion for summary judgment, arguing there are no disputed facts and they are entitled to win without a trial. This is a critical moment.

To oppose a summary judgment motion, you must submit evidence showing that genuine factual disputes exist. That means affidavits, payment records, correspondence logs, and expert declarations if needed. A bare denial is not enough at this stage. Courts require actual evidence.

Watch for these warning signs during litigation:

- The lender files for summary judgment before discovery is complete

- Your servicer produces documents with inconsistent dates or signatures

- The plaintiff’s attorney cannot produce the original promissory note

- You receive court notices at the wrong address, suggesting improper service

If the court denies your defenses or grants summary judgment against you, you still have options. A loan modification can sometimes be negotiated even after judgment. Bankruptcy can still trigger an automatic stay before the sale date. Appeals are available if the court made a legal error. The Florida foreclosure process has multiple intervention points, and understanding the full foreclosure timeline helps you identify each one.

Key takeaways

A complete, timely foreclosure defense response filing that raises all applicable affirmative defenses is the single most effective tool a homeowner has to delay, negotiate, or defeat a foreclosure action.

| Point | Details |

|---|---|

| File within the deadline | Missing the 20 to 30 day Answer deadline results in default judgment and eliminates all defenses. |

| Respond to every allegation | Silence on any numbered allegation is treated as an admission by the court. |

| Raise all defenses upfront | Affirmative defenses not raised in the Answer may be permanently waived under 2026 rules. |

| Use federal protections | A complete loss mitigation application filed 37+ days before sale legally stops the foreclosure clock. |

| Document everything | Communication logs with your servicer are critical evidence for standing and TILA-based defenses. |

What I’ve learned from watching homeowners fight foreclosure

I have seen homeowners walk into consultations holding a foreclosure summons they received three weeks earlier, having done nothing because they were overwhelmed or assumed the bank would work things out with them. That assumption is the most expensive mistake a homeowner can make.

The lender’s attorney filed that complaint on a schedule. They are not waiting for you to feel ready. The 20 to 30 day deadline is real, and courts enforce it without sympathy.

What surprises most people is how much leverage they actually have once they file. Lenders do not want to go to trial. Trials are expensive, slow, and unpredictable. A well-drafted Answer with solid affirmative defenses, especially a standing challenge backed by a defective assignment document, changes the entire dynamic of the case. I have watched servicers offer meaningful loan modifications to homeowners who had been ignored for months, simply because a properly filed Answer forced them to take the case seriously.

The other thing I tell every homeowner: do not treat your defenses as an all-or-nothing bet on winning in court. The real goal is often to buy time, create negotiating leverage, and reach a resolution that lets you stay in your home or exit on your own terms. Combining a strong Answer with a loss mitigation application and a CFPB complaint is not a legal long shot. It is a coordinated strategy that works.

Get an attorney involved as early as possible. Not because the process is impossible to understand, but because the details matter enormously. One missed defense, one improperly served document, one formatting error can cost you rights you cannot recover. The legal strategies available to Florida homeowners in 2026 are genuinely powerful. Use them.

— Steven

How Wallacelawflorida can help with your foreclosure defense

Facing a foreclosure complaint is one of the most stressful legal situations a homeowner can experience. Wallacelawflorida has guided Florida homeowners through exactly this process, from drafting a complete Answer to raising standing defenses and negotiating with servicers in Boynton Beach and across South Florida.

The attorneys at Wallacelawflorida understand local court rules, Florida-specific procedural requirements, and the federal protections that apply to your case in 2026. They work directly with you, not through a rotating team of associates, so you always know who is handling your case. If you are facing a foreclosure complaint and need experienced guidance on your real estate legal options, contact Wallacelawflorida today for a consultation before your deadline passes.

FAQ

What is a foreclosure defense response filing?

A foreclosure defense response filing is a formal Answer submitted to the court in response to a lender’s foreclosure lawsuit. It addresses each allegation in the complaint and raises affirmative defenses to protect your homeowner rights.

How long do I have to file a foreclosure Answer in Florida?

Florida homeowners typically have 20 days from the date of service to file an Answer. Missing this deadline allows the lender to seek a default judgment, which removes all your defenses.

What affirmative defenses can I raise in my Answer?

Common defenses include lack of standing to foreclose, improper service of process, TILA violations, dual tracking, and statute of limitations. Failing to include all defenses in your initial Answer may permanently waive them.

Can bankruptcy stop a foreclosure after I file my Answer?

Yes. Bankruptcy triggers an automatic stay that immediately halts foreclosure proceedings. Chapter 13 allows you to propose a repayment plan to catch up on arrears and keep your home.

What happens if the lender files a motion for summary judgment?

You must respond with actual evidence showing disputed facts exist, including affidavits, payment records, and correspondence. A bare denial is insufficient. Consulting an attorney before responding to a summary judgment motion is strongly recommended.