TL;DR:

- Chapter 7 eligibility depends primarily on passing the means test, which compares your average monthly income over six months to your state’s median income for your household size. Additional requirements include completing approved credit counseling within 180 days before filing and adhering to restrictions based on previous bankruptcy filings; meeting all procedural prerequisites is essential for a successful case. Proper expense classification using official IRS standards and district-specific multipliers is crucial, as errors can result in a presumption of abuse and case dismissal.

Chapter 7 bankruptcy eligibility is primarily determined by the means test, which compares your average monthly income over the previous six months to your state’s median income for your household size. Passing this test is the central chapter 7 eligibility criteria that courts use to decide whether you qualify for a full discharge of unsecured debts. Beyond income, you must complete approved credit counseling before filing and meet specific filing history requirements. This guide walks you through every chapter 7 bankruptcy requirement so you can assess your position clearly before taking any legal steps.

What is the Chapter 7 means test and how does it determine eligibility?

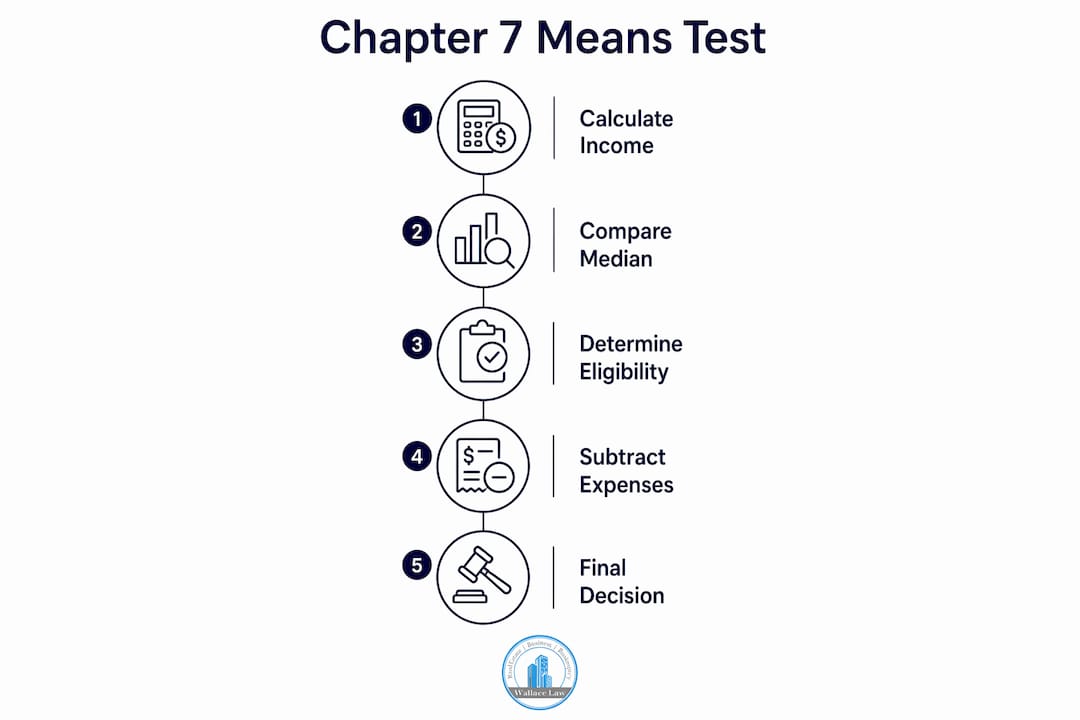

The means test is a two-part calculation established under the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005. It exists to prevent higher-income filers from using Chapter 7 when they could reasonably repay creditors through a Chapter 13 repayment plan. Understanding how it works is the foundation of any chapter 7 bankruptcy eligibility guide.

Part one: income comparison

The means test compares your Current Monthly Income (CMI) to your state’s median income for your household size. CMI is calculated by averaging your gross income over the six full calendar months before your filing date. The U.S. Trustee Program updates median income figures annually using Census Bureau data and Consumer Price Index adjustments. Cases filed on or after April 1, 2026, must use the updated means testing data reflecting the latest CPI adjustments. This means the table that applies to your case depends entirely on when you file, not when you started planning.

If your CMI falls at or below your state’s median income for your household size, you pass the means test automatically. You do not need to complete Part 2 of Form 122A-2, and your filing moves forward on the income question alone.

Part two: disposable income calculation

If your income exceeds the state median, the process continues with Form 122A-2, which subtracts allowable expenses from your CMI to calculate monthly disposable income. This is where many filers are surprised to learn they still qualify. Allowable deductions include housing, transportation, food, healthcare, secured debt payments, and certain priority obligations. The result is your net monthly disposable income after those deductions.

That disposable income figure is then multiplied by 60 to project it over five years. If the 60-month total falls below statutory thresholds, no presumption of abuse arises and you remain eligible. If it exceeds those thresholds, a presumption of abuse is triggered and your case faces additional scrutiny.

Here is a simplified view of how the two-part test flows:

- Calculate your CMI by averaging gross income over the prior six months.

- Compare CMI to your state’s median income for your household size.

- If CMI is at or below median, you qualify automatically.

- If CMI exceeds median, complete Form 122A-2 to subtract allowable expenses.

- Multiply monthly disposable income by 60 and compare to abuse thresholds.

- If the result is below the threshold, you qualify. If above, a presumption of abuse arises.

Pro Tip: Always use official Forms 122A-1 and 122A-2 approved by the Judicial Conference. Third-party calculators frequently use outdated median income tables or miss district-specific expense multipliers, which can produce inaccurate results.

What are the prerequisites and filing restrictions for Chapter 7?

Passing the means test is necessary but not sufficient on its own. Several additional chapter 7 bankruptcy requirements apply before your petition can proceed.

Credit counseling

Consumer credit counseling from an agency approved by the U.S. Trustee Program is mandatory for virtually all individual filers. The session must occur within 180 days before you file your petition, and you must attach the completion certificate to your filing documents. This requirement under Section 109(h) of the Bankruptcy Code is strictly enforced. Missing it results in outright dismissal regardless of how well you performed on the means test. The counseling session typically takes 60 to 90 minutes and can be completed online or by phone through approved providers. You can find a list of approved agencies through the U.S. Trustee Program’s website or through resources like Miracle Financial for credit-related guidance.

Filing history restrictions

The following restrictions apply based on your prior bankruptcy history:

- You cannot file Chapter 7 if you received a Chapter 7 discharge within the past eight years.

- You cannot file Chapter 7 if you received a Chapter 13 discharge within the past six years, with limited exceptions for cases where creditors were paid in full.

- If a prior bankruptcy case was dismissed within the last 180 days due to willful failure to comply with court orders or voluntary dismissal after a creditor sought relief, an automatic stay may not apply to your new filing.

- You must not have had a Chapter 7 or Chapter 13 case dismissed for abuse within the prior 180 days.

The 341 meeting of creditors

Once you file, you are required to attend a 341 meeting under Bankruptcy Code Section 341. At this meeting, the trustee and any attending creditors can question you under oath about your finances and the accuracy of your petition. Failure to appear risks dismissal of your case. Most 341 meetings last only 10 to 15 minutes when the paperwork is in order, but preparation matters. Bring your government-issued ID, Social Security card, and any supporting financial documents the trustee requests in advance.

How do expenses affect your Chapter 7 means test calculation?

The expense side of Form 122A-2 is where qualifying for Chapter 7 becomes more nuanced than most people expect. Allowable expenses are not what you actually spend each month. They are standardized amounts set by IRS National and Local Standards, supplemented by district-specific administrative expense multipliers published by the U.S. Trustee Program.

The table below compares how allowable expenses differ from actual spending in practice:

| Expense category | Allowable deduction | Actual spending |

|---|---|---|

| Food and clothing | IRS National Standard by household size | Your real grocery and clothing bills |

| Housing and utilities | IRS Local Standard by county | Your actual rent or mortgage payment |

| Transportation | IRS Local Standard for ownership/operating | Your real car payment and fuel costs |

| Out-of-pocket healthcare | IRS standard by age group | Your actual medical expenses |

| Secured debt payments | Actual contractual payment amounts | Same as allowable in most cases |

For housing and transportation, you use the IRS Local Standard for your county, not your actual payment, unless your actual payment is lower. For secured debts like a mortgage or car loan, you deduct the actual contractual payment. This distinction matters because overestimating allowable deductions is one of the most common errors that leads to case dismissal.

The 60-month multiplier built into Form 122A-2 amplifies even small differences in expense classification. A $200 per month difference in allowable deductions translates to a $12,000 difference in the 60-month projection. That gap can determine whether a presumption of abuse is triggered. Courts apply specific formulas and multipliers per judicial district, so the same income and expense profile can produce different results depending on where you file.

Pro Tip: Review the administrative expense schedules published for your judicial district before completing Form 122A-2. These schedules contain the exact multipliers used in your jurisdiction and are updated with each new means-testing data release.

Priority debts, including recent tax obligations and domestic support arrears, are also deductible on Form 122A-2. These are divided by 60 and subtracted as a monthly amount. Including them accurately can meaningfully reduce your projected disposable income and improve your eligibility outcome.

What happens if your Chapter 7 filing triggers a presumption of abuse?

A presumption of abuse does not automatically end your case. It triggers a formal review process under 11 U.S.C. §707(b), and you retain the right to rebut the presumption with evidence of special circumstances.

The procedural steps that follow a presumption of abuse include:

- The U.S. Trustee or bankruptcy trustee reviews your means test results and files a motion to dismiss or convert your case.

- The court schedules a hearing with notice provided to you, the trustee, and the U.S. Trustee as required under Federal Rule of Bankruptcy Procedure 1017.

- You have the opportunity to present documentation of special circumstances, such as a serious medical condition or a significant income reduction that occurred after the filing date.

- If the court finds the presumption unrebutted, it may dismiss your case or convert it to a Chapter 13 repayment plan with your consent.

- If dismissed without prejudice, you may refile under Chapter 13 or address the circumstances that triggered the presumption before attempting another Chapter 7 filing.

Conversion to Chapter 13 is not necessarily a bad outcome. A Chapter 13 plan allows you to repay debts over three to five years while keeping assets you might otherwise lose. For filers with regular income who simply earn too much for Chapter 7, Chapter 13 often provides comparable relief with greater flexibility on secured debts like mortgages.

The key takeaway here is that a presumption of abuse is a procedural trigger, not a final judgment. Responding promptly with accurate documentation and qualified legal representation gives you a real opportunity to address the court’s concerns.

Key takeaways

Chapter 7 bankruptcy eligibility turns on the means test, and passing it requires accurate income reporting, correct expense classification, and compliance with all procedural prerequisites before filing.

| Point | Details |

|---|---|

| Means test is the core filter | Your average monthly income over six months is compared to your state’s median income by household size. |

| Above-median income is not disqualifying | Allowable expense deductions on Form 122A-2 can reduce disposable income below abuse thresholds. |

| Credit counseling is non-negotiable | Complete an approved session within 180 days before filing or face automatic dismissal. |

| Filing timing affects eligibility | Median income tables update with CPI data; the table in effect on your filing date controls your result. |

| Presumption of abuse is rebuttable | Special circumstances evidence can overcome a triggered presumption and preserve your Chapter 7 case. |

Why timing and expense accuracy matter more than most filers realize

Most people approaching Chapter 7 focus almost entirely on whether their income is above or below the state median. That is understandable, but it misses the more consequential part of the analysis. In my experience working with clients in South Florida, the cases that run into trouble are rarely the ones where income is clearly too high. They are the ones where expense reporting is sloppy or where the filer used outdated median income data because they waited too long after their initial consultation to actually file.

The filing date controls which median income table applies, and those tables shift with CPI adjustments every April and October. A client who would have qualified under the prior table may not qualify under the new one, and vice versa. That is not a technicality. It is a real strategic consideration that should factor into your timeline.

On the expense side, the most common mistake I see is treating Form 122A-2 like a personal budget worksheet. It is not. The IRS standards and district multipliers are specific legal inputs, and courts will not accept substitutes. Filers who report their actual grocery spending instead of the IRS National Standard for their household size, or who miss deductible priority debt payments, often end up with a higher disposable income figure than they should have. That error can be the difference between qualifying and triggering a presumption of abuse.

If Chapter 7 turns out not to be the right fit, that is not the end of the road. Chapter 13 offers a structured path to debt relief for filers with regular income, and the requirements for Chapter 7 are worth revisiting after any significant change in income or household size.

— Steven

How Wallacelawflorida can help you file with confidence

Wallacelawflorida works with individuals across Boynton Beach and South Florida who are navigating Chapter 7 eligibility questions and need accurate, personalized guidance. The attorneys at Wallace Law handle means test calculations using current 2026 data, review your expense classifications against IRS and district standards, and prepare your petition using the correct official forms.

If you are unsure whether you qualify or want a clear picture of your options before committing to a filing strategy, the bankruptcy legal services at Wallace Law offer the kind of attentive, one-on-one support that larger firms rarely provide. Whether Chapter 7 is the right path or Chapter 13 better fits your situation, you will get a direct answer grounded in Florida-specific knowledge and current federal requirements.

FAQ

What income level qualifies you for Chapter 7?

Your income must fall at or below your state’s median income for your household size, or your allowable expenses must reduce your monthly disposable income below statutory abuse thresholds when projected over 60 months. There is no single dollar figure because the threshold varies by state and household size.

How is the bankruptcy means test calculated?

The means test calculation averages your gross income over the six months before filing, compares it to the state median, and if above median, subtracts IRS-standardized allowable expenses on Form 122A-2 to determine monthly disposable income. That figure is multiplied by 60 and compared to abuse thresholds.

Is credit counseling required before filing Chapter 7?

Yes. You must complete a credit counseling session from a U.S. Trustee-approved agency within 180 days before filing. Failure to do so results in automatic dismissal of your case under Section 109(h) of the Bankruptcy Code.

Can I refile Chapter 7 after a dismissal?

You can refile after a dismissal, but filing restrictions apply if the prior case was dismissed for abuse or willful noncompliance. The standard waiting period between Chapter 7 discharges is eight years from the date of the prior filing.

What is the 341 meeting and do I have to attend?

The 341 meeting of creditors is a required hearing where the trustee questions you under oath about your finances and petition accuracy. Attendance is mandatory. Missing it without a valid excuse typically results in dismissal of your case.