TL;DR:

- A Chapter 13 repayment plan reorganizes personal debts into manageable monthly payments lasting three to five years. Success requires thorough preparation, accurate income documentation, and strict adherence to court deadlines. Proper planning ensures creditors are paid in order, and assets are protected throughout the process.

Chapter 13 repayment plan setup is the court-approved process of restructuring personal debts into a manageable monthly payment schedule lasting three to five years. Known formally as a “wage earner’s plan” under Title 11 of the U.S. Bankruptcy Code, it lets you keep your home and other assets while catching up on overdue mortgage payments, car loans, and other secured debts. You make a single monthly payment to a court-appointed trustee, who then distributes funds to your creditors in a legally defined order. Getting the structure right from day one determines whether your plan gets confirmed or rejected.

What prerequisites and documentation do you need for a Chapter 13 repayment plan setup?

Preparation is the most underestimated phase of the entire process. Courts reject plans not because filers lack good intentions, but because they arrive without the right paperwork or miss a mandatory legal step.

The first requirement is a credit counseling course from a court-approved provider. This course is mandatory within 180 days before filing and typically runs 60–90 minutes. Skipping it disqualifies your case before it begins.

Beyond counseling, you need to gather the following documents:

- Proof of income: Pay stubs covering the last six months, your two most recent federal tax returns, and documentation of any other income sources such as rental income or self-employment earnings

- Debt records: A complete list of every creditor, the balance owed, and whether each debt is secured (mortgage, car loan), priority (taxes, child support), or unsecured (credit cards, medical bills)

- Asset documentation: Current market values for real estate, vehicles, bank accounts, retirement accounts, and personal property

- Monthly expense records: Utility bills, insurance premiums, food costs, transportation, and childcare

The Chapter 13 filing fee is $313. If you cannot pay it upfront, the court allows installment payments for up to 120 days after filing. That flexibility matters when cash is already tight.

| Document type | What to gather |

|---|---|

| Income proof | Six months of pay stubs, last two tax returns |

| Debt list | Creditor names, balances, and debt classification |

| Asset values | Real estate appraisals, vehicle values, account balances |

| Living expenses | Bills, receipts, and insurance statements |

| Filing fee | $313 total, payable in installments up to 120 days |

Pro Tip: Organize every document into a single folder before you meet with an attorney. Courts and trustees move fast, and missing one item can delay your entire case by weeks.

How do you calculate disposable income and plan length?

Your monthly payment amount and plan duration both flow from one number: your disposable income. Getting this calculation right is the single most important financial task in the entire process.

Calculating current monthly income

Current monthly income (CMI) is the average of your gross income over the six months before filing. You add up all income sources for those six months and divide by six. Accurate income measurement requires six months of pay stubs and tax returns, and trustees specifically exclude one-time bonuses or temporary overtime. That exclusion catches many filers off guard. If your income looks higher on paper because of a seasonal bonus, your CMI will still reflect the lower baseline the trustee uses.

Subtracting allowed living expenses

From your CMI, you subtract “reasonably necessary” living expenses. The IRS National Standards and Local Standards set limits for categories like food, clothing, housing, and transportation. Allowed deductions typically include:

- Rent or mortgage payments

- Utilities and phone

- Health insurance premiums

- Childcare and education costs

- Transportation (car payment plus operating costs)

- Out-of-pocket medical expenses

What remains after subtracting these expenses is your disposable income. That figure is what goes to unsecured creditors each month.

How income relative to state median sets plan length

Income at or below your state median requires a three-year plan. Income above the state median requires a five-year plan, and no plan can legally exceed five years. This rule has a direct financial consequence. A five-year plan spreads payments over more months, which lowers the monthly amount but extends your commitment. A three-year plan costs more per month but ends sooner.

| Income level | Plan length | Key implication |

|---|---|---|

| At or below state median | 3 years | Higher monthly payment, shorter commitment |

| Above state median | 5 years | Lower monthly payment, longer commitment |

| Any level | Max 5 years | No plan can legally run longer |

Pro Tip: Do not include overtime you no longer receive or a second job you recently left. Trustees verify income against actual documents, and overstating your CMI can trigger objections that delay or kill your plan.

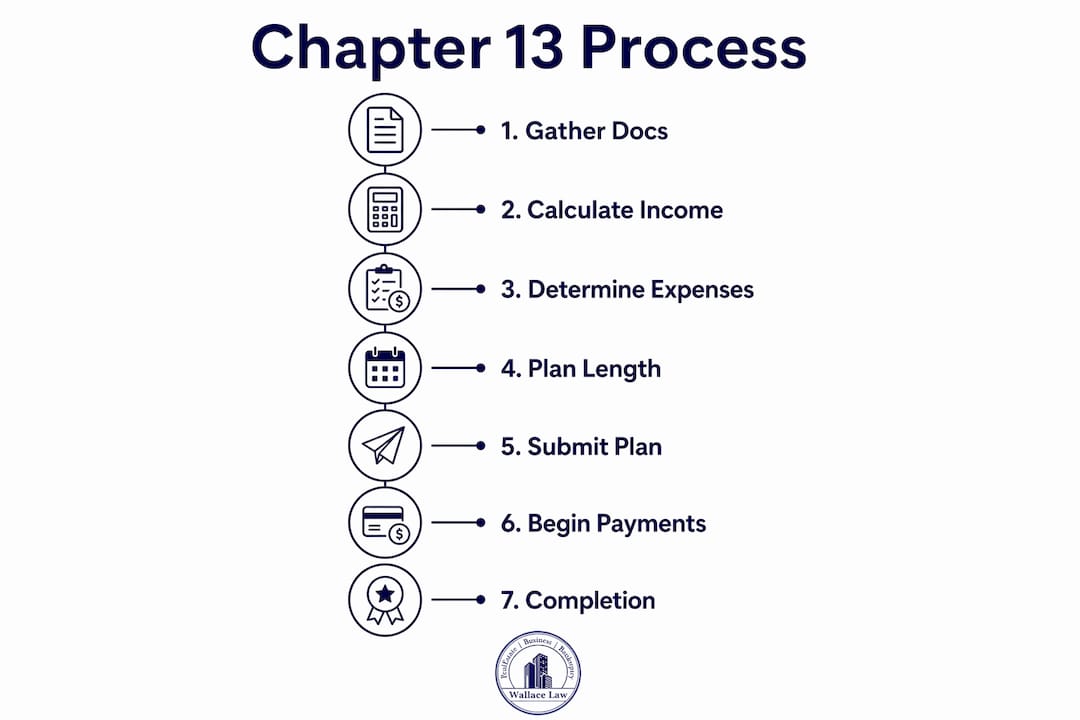

What is the step-by-step process to file a Chapter 13 plan with the court?

Filing is a sequence of timed steps. Missing any deadline can result in dismissal before your plan ever gets a hearing.

- File the voluntary petition. Submit your petition, schedules of assets and liabilities, a statement of financial affairs, and your means test calculation to the bankruptcy court. This officially opens your case and triggers the automatic stay, which stops most collection actions immediately.

- Submit your proposed repayment plan within 14 days. The proposed plan must be filed within 14 days of your petition date. The plan outlines how much you will pay each month, how long the plan runs, and how each class of creditor gets paid.

- Start payments to the trustee within 30 days. You must begin making payments to the trustee within 30 days of filing, even before the court confirms your plan. Missing this first payment is one of the fastest ways to get your case dismissed.

- Attend the 341 meeting of creditors. Roughly 21–40 days after filing, you appear before the trustee (not a judge) to answer questions about your finances under oath. Creditors may attend but rarely do. Bring your photo ID and Social Security card.

- Attend the confirmation hearing. The judge reviews your plan, considers any objections from creditors or the trustee, and decides whether to confirm it. Common objections include:

- Disposable income calculation errors

- Failure to pay priority creditors in full

- Lack of good faith in the plan’s structure

- Undervalued assets that affect unsecured creditor payments

- Respond to objections or modify the plan. If the court does not confirm your plan, you can amend it to address specific objections. Most plans get confirmed after one or two revisions.

The steps in Chapter 13 bankruptcy follow a strict procedural timeline. Staying organized and meeting every deadline is not optional. It is the difference between a confirmed plan and a dismissed case.

How are payments distributed and what happens during the plan term?

Once your plan is confirmed, the trustee takes over payment distribution. You send one monthly payment to the trustee, and the trustee pays your creditors according to a legally defined priority order.

Trustees distribute payments in this sequence: administrative fees first, then priority debts, then secured debts, and finally unsecured creditors. Administrative fees include the trustee’s own compensation and any attorney fees approved by the court. Priority debts include back taxes and domestic support obligations like child support and alimony. Secured debts cover your mortgage arrears and car loans. Unsecured creditors, such as credit card companies, receive whatever disposable income remains.

Two tools within Chapter 13 can reduce what you owe on secured debts:

- Cramdown: Reduces the principal on a secured loan to the current market value of the collateral. This applies to car loans and investment properties but not to your primary residence mortgage.

- Lien stripping: Removes a junior mortgage (such as a second mortgage or home equity loan) when the home’s value is less than what you owe on the first mortgage. This converts that debt to unsecured status.

Missing payments or failing to file required forms on time can lead to dismissal or conversion to Chapter 7. Conversion to Chapter 7 means losing the protection that Chapter 13 provides for assets like your home. If your financial situation changes during the plan, you can request a modification, a hardship discharge, or conversion. Early payoff requires paying all debts in full plus interest and fees, which often costs more than simply completing the remaining scheduled payments.

Pro Tip: Set up automatic bank transfers for your trustee payment the moment your plan is confirmed. A single missed payment puts your entire case at risk, and “I forgot” is not a defense the court accepts.

After completing the plan, the court discharges most remaining unsecured debts. However, certain debts survive discharge, including domestic support obligations, most student loans, some tax debts, criminal fines, and damages from intentional injury. Finishing the plan does not erase these obligations.

Key Takeaways

A successful Chapter 13 repayment plan requires accurate income documentation, realistic expense budgeting, and strict adherence to court deadlines from the first payment through final discharge.

| Point | Details |

|---|---|

| Credit counseling is mandatory | Complete a court-approved course within 180 days before filing or your case is disqualified. |

| Plan length depends on income | Earners at or below state median get a 3-year plan; above median requires a 5-year plan. |

| Payments start before confirmation | You must pay the trustee within 30 days of filing, before the court approves your plan. |

| Trustee pays creditors in priority order | Administrative fees, priority debts, secured debts, and unsecured creditors are paid in that sequence. |

| Some debts survive discharge | Student loans, domestic support, and certain taxes remain after plan completion. |

What I’ve learned about building a Chapter 13 plan that actually gets confirmed

The plans that fail almost always fail for the same reason: the numbers look good on paper but do not reflect real life. Filers undercount their monthly expenses because they forget irregular costs like car repairs, medical copays, or annual insurance premiums. Then the trustee runs the numbers, finds the disposable income is higher than reported, and objects to the plan.

Good faith is the standard courts use to measure whether a plan deserves confirmation. Under Section 1325(a)(3) of the Bankruptcy Code, misrepresenting income or assets does not just delay your case. It can result in dismissal or revocation of a confirmed plan. The court takes this seriously, and so should you.

Filing without an attorney is legally allowed but strongly discouraged by legal professionals. Chapter 13 involves managing creditor objections, court hearings, and monthly payments over years. One procedural error can unravel months of work. The cost of an attorney is almost always less than the cost of a dismissed case and a second filing.

My honest advice: budget conservatively, document everything, and treat every court deadline like it is the only one that matters. Because in Chapter 13, it is.

— Steven

Wallacelawflorida can help you build a plan that holds up in court

Filing a Chapter 13 plan is not just paperwork. It is a legal commitment that runs for years, and the details matter from day one.

Wallacelawflorida works with individuals in Boynton Beach and across South Florida who need a Chapter 13 bankruptcy plan that is accurate, realistic, and built to get confirmed. The firm prepares income calculations, expense documentation, and creditor schedules with the precision that trustees and courts expect. Wallacelawflorida also guides clients through the 341 meeting, confirmation hearings, and any plan modifications that arise along the way. If foreclosure is on the table, acting quickly with the right legal support can make the difference between keeping your home and losing it. Reach out to Wallacelawflorida to get your plan started on solid legal ground.

FAQ

What is the Chapter 13 filing fee?

The Chapter 13 filing fee is $313. The court allows you to pay it in installments for up to 120 days after filing if you cannot pay the full amount upfront.

How long does a Chapter 13 repayment plan last?

Plan length depends on your income relative to your state’s median. Filers at or below the median complete a three-year plan; those above the median must complete a five-year plan, which is the legal maximum.

When do Chapter 13 payments start?

Payments to the trustee must begin within 30 days of filing your petition, before the court confirms your plan. Missing this first payment can result in case dismissal.

What debts are not discharged after completing Chapter 13?

Domestic support obligations, most student loans, certain tax debts, criminal fines, and damages from intentional injury all survive Chapter 13 discharge and remain your responsibility after the plan ends.

Can you file Chapter 13 without an attorney?

Filing without an attorney is legally permitted but strongly discouraged. The procedural complexity of managing creditor objections, court hearings, and multi-year payment schedules makes legal counsel a practical necessity for most filers.