TL;DR:

- A bankruptcy petition is a formal legal document that initiates a case in federal court, triggering automatic stay protections against creditors. It involves a detailed packet of forms and disclosures that must be accurately completed and filed within strict deadlines to ensure case success. After filing, a trustee is appointed, the automatic stay takes effect, and a 341 meeting is scheduled to review the debtor’s financial situation.

A bankruptcy petition is the formal legal document that initiates a bankruptcy case in federal court, triggering automatic stay protections the moment it is filed. Most people picture a single form, but the petition is actually the first page of a larger packet containing schedules, financial statements, and certifications that the court requires to administer your case. Understanding what a bankruptcy petition is, what it contains, and what happens after you file gives you a real advantage when you are facing serious debt. This guide covers every stage of the process, from petition types to legal consequences, so you can move forward with clarity instead of fear.

What is a bankruptcy petition, and how does it work?

A bankruptcy petition is a formal request filed with the U.S. Bankruptcy Court that opens your case and places you under the protection of federal bankruptcy law. The moment the court clerk accepts your filing, the automatic stay goes into effect. That means creditors must immediately stop collection calls, lawsuits, wage garnishments, and foreclosure actions. This protection alone is why many people file even before they have gathered every document.

The petition itself identifies who you are, where you live, what chapter of bankruptcy you are filing under, and whether you have filed before. It is signed under penalty of perjury, which makes accuracy a legal obligation, not just a best practice. The bankruptcy petition process is governed by Title 11 of the U.S. Code and the Federal Rules of Bankruptcy Procedure, which set out exactly what must be filed and when.

What are the different types of bankruptcy petitions?

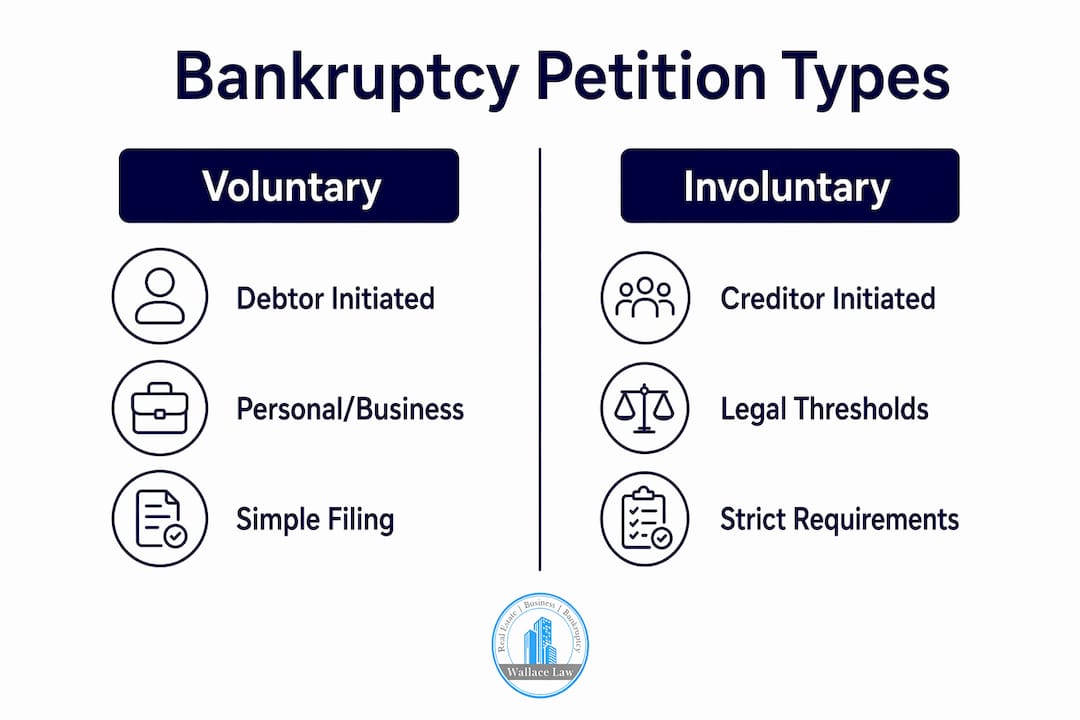

Not every petition looks the same. The type you file depends on who is filing and why. Here is a breakdown of the main petition types:

- Voluntary petition: Filed by the debtor, whether an individual, a married couple, or a business. This is by far the most common type. Individual filers use Official Form 101, which covers personal information, prior filings, and the chapter being requested.

- Involuntary petition: Filed by creditors against a debtor who owes them money. Creditors must meet strict legal thresholds under 11 U.S.C. to force a debtor into bankruptcy. This route is rare and typically reserved for business debtors.

- Joint petition: A married couple may file a single petition together if their debts are primarily shared. This can reduce court fees and simplify the process.

- Chapter-specific petitions: The chapter you choose, whether Chapter 7, Chapter 11, or Chapter 13, determines the form used and the rules that apply. You can review the key differences between Chapter 7 and Chapter 13 to decide which fits your situation before you file.

Voluntary and involuntary petitions carry different legal requirements. Involuntary petitions require creditors to prove the debtor is generally not paying debts as they come due, a threshold that courts take seriously. For most individuals reading this, the voluntary petition under Chapter 7 or Chapter 13 is the relevant path.

What documents and information does a bankruptcy petition require?

People often mistake the bankruptcy petition as a single form, but it is really a packet that includes many schedules and financial disclosures essential for case administration. Getting this packet right is where most filers run into trouble.

Here is what the full petition packet typically includes:

- Official Form 101 (or the applicable chapter form): Your name, address, Social Security number, prior filings, and the chapter requested.

- Schedules A through J: These cover real property, personal property, secured claims, unsecured claims, executory contracts, income, and monthly expenses.

- Statement of Financial Affairs (SOFA): A detailed history of your financial transactions, income sources, and any property transfers in the past two years.

- Means Test (Chapter 7 only): Form 122A determines whether your income qualifies you for Chapter 7 relief.

- Credit counseling certificate: Proof that you completed an approved counseling session within 180 days before filing. Credit counseling is mandatory and must come from a U.S. Trustee-approved provider.

- Statement of Social Security Number: Filed separately and kept confidential by the court.

Under FRBP Rule 1007, most of these documents must be filed either with the petition or within 14 days of filing. Missing that 14-day window puts your case at serious risk of dismissal. The court does not chase you for missing paperwork. The obligation is entirely yours.

| Document | Deadline |

|---|---|

| Official Form 101 (petition) | At filing |

| Credit counseling certificate | At filing (completed within 180 days prior) |

| Schedules A through J | At filing or within 14 days |

| Statement of Financial Affairs | At filing or within 14 days |

| Debtor education certificate | Before discharge (post-filing) |

Pro Tip: Start gathering bank statements, tax returns, pay stubs, and property records at least 30 days before you plan to file. The biggest source of delay is not the court. It is the debtor scrambling to find documents at the last minute.

You can use the 2026 bankruptcy filing checklist from Wallacelawflorida to track every required document before you submit anything to the court.

What happens after filing a bankruptcy petition?

Filing the petition is the starting gun, not the finish line. Here is what the process looks like after your case number is assigned:

- Case number and trustee assignment: The court clerk assigns a case number immediately. A bankruptcy trustee is appointed to administer your case and review your documents.

- Automatic stay: Creditor actions stop by law. This includes foreclosures, repossessions, lawsuits, and wage garnishments. The stay is one of the most powerful protections in federal law.

- Section 341 meeting of creditors: The 341 meeting is scheduled 21 to 40 days after filing. You appear before the trustee, answer questions under oath, and confirm the accuracy of your petition. Creditors may attend but rarely do in consumer cases.

- Trustee review: The trustee compares your petition and schedules with your statements at the 341 meeting. Discrepancies cause delays and can trigger deeper scrutiny of your finances.

- Discharge or repayment plan: In Chapter 7, most unsecured debts are discharged within three to six months of filing. In Chapter 13, you enter a three to five year repayment plan before receiving a discharge.

Pro Tip: Bring your government-issued photo ID and your Social Security card to the 341 meeting. The trustee is required to verify your identity, and showing up without these documents will get your meeting rescheduled and your case delayed.

The debtor education course is a separate requirement you must complete after filing but before your discharge is granted. Missing it means your debts will not be discharged, even if everything else goes perfectly.

What are the legal risks of filing a bankruptcy petition?

Signing the bankruptcy petition is not a formality. You are signing under penalty of perjury, which means every statement in the document carries legal weight.

“False statements on a bankruptcy petition can result in fines up to $250,000 and imprisonment up to 5 years under federal bankruptcy fraud statutes.” — Nolo

Bankruptcy fraud is prosecuted by the U.S. Department of Justice. Common triggers include hiding assets, transferring property to family members before filing, and understating income on the means test. These are not technicalities. Courts and trustees are trained to spot inconsistencies between your petition, your schedules, and your testimony at the 341 meeting.

Accurate and consistent financial disclosures across all documents are the single most effective way to avoid scrutiny and keep your case moving. If you realize you made an error after filing, you can file an amended schedule. Catching and correcting mistakes proactively is far better than having the trustee find them first.

Emergency or skeleton filings are a legitimate procedural tool when you need the automatic stay to kick in immediately, for example, to stop a foreclosure sale scheduled for tomorrow. Under FRBP Rule 1007, you file a bare-bones petition and then have 14 days to submit the full packet. This is a bridge, not a strategy. Filers who treat skeleton filings as a way to buy time without preparing their documents almost always end up with a dismissed case.

If you have back tax obligations that are part of your debt picture, those require separate attention. Not all tax debts are dischargeable in bankruptcy, and the rules around them are specific to the type of tax and how old the debt is.

Key takeaways

A bankruptcy petition is a legally binding document that opens your case, triggers the automatic stay, and sets every subsequent deadline in motion. Accuracy, completeness, and timing determine whether your case succeeds or gets dismissed.

| Point | Details |

|---|---|

| Petition triggers automatic stay | Legal protections against creditors begin the moment the court accepts your filing. |

| Petition is a full packet | You must file schedules, statements, and a credit counseling certificate, not just one form. |

| 14-day deadline is firm | Missing the window to file supporting documents risks automatic case dismissal. |

| Perjury risk is real | False statements carry fines up to $250,000 and up to 5 years in federal prison. |

| Two education courses required | Credit counseling before filing and a debtor education course after filing are both mandatory for discharge. |

What I have learned from watching clients navigate this process

The clients who come to me most prepared are not the ones who waited until the last minute and filed a skeleton petition to stop a foreclosure. They are the ones who spent two or three weeks pulling together every bank statement, every tax return, and every creditor letter before we ever touched a form. That preparation does not just make the filing cleaner. It makes the 341 meeting almost uneventful, because there are no surprises for the trustee to find.

The piece of advice I give every client that they do not expect: do your credit counseling before you think you need it. The 180-day window sounds generous until you realize you are scrambling to find an approved provider the night before you want to file. The U.S. Trustee Program maintains a list of approved agencies, and the session takes about two hours. There is no reason to leave it to the last minute.

I also want to push back on the anxiety that surrounds bankruptcy. Filing a petition is not an admission of failure. It is a legal tool that Congress created specifically for people in your situation. The automatic stay alone, which stops creditor harassment the moment your case is filed, changes the daily reality for most filers within 24 hours. That is a meaningful result. The process has real requirements and real deadlines, but none of them are designed to trap you. They are designed to give the court a complete and honest picture of your finances so it can give you a fair resolution.

The one thing that derails cases more than anything else is incomplete or inconsistent paperwork. Not bad intentions. Not complicated finances. Just missing documents and mismatched numbers. Get the paperwork right, and the process works the way it is supposed to.

— Steven

How Wallacelawflorida can help you file with confidence

Filing a bankruptcy petition in Florida involves federal rules, local court procedures, and deadlines that do not wait for you to catch up. Wallacelawflorida works with individuals and families in Boynton Beach and throughout South Florida who are ready to take control of their financial situation. The team provides hands-on guidance through every stage, from gathering your documents to representing you at the 341 meeting. You can start with the free Florida bankruptcy eBook for a plain-language overview of the process, or go straight to the bankruptcy practice area to schedule a consultation with an attorney who knows Florida bankruptcy courts personally.

FAQ

What is a bankruptcy petition in simple terms?

A bankruptcy petition is the official legal document you file with a federal bankruptcy court to open your case. It triggers the automatic stay and starts the debt resolution process under U.S. bankruptcy law.

How long does it take to file a bankruptcy petition?

Gathering documents typically takes two to four weeks. The actual filing with the court clerk takes less than a day, and your case number and automatic stay are issued immediately upon acceptance.

What happens if my bankruptcy petition is incomplete?

Under FRBP Rule 1007, you have 14 days to file missing schedules and statements after submitting the petition. If you miss that deadline, the court can dismiss your case without discharging any of your debts.

Can creditors file a bankruptcy petition against me?

Yes. An involuntary petition can be filed by qualifying creditors under 11 U.S.C., but strict legal thresholds apply. This is rare in consumer cases and far more common in business bankruptcy situations.

Do I need a lawyer to file a bankruptcy petition?

You are legally permitted to file without an attorney, which is called filing “pro se.” However, errors in the petition or missing documents are a leading cause of case dismissal, and a bankruptcy attorney significantly reduces that risk.