TL;DR:

- Secured debt bankruptcy involves filing when debts are backed by collateral like homes or cars. Creditors retain the right to repossess assets through liens even after bankruptcy discharge. Managing secured debts requires timely decisions on reaffirmation, redemption, or surrender to protect assets and avoid loss.

Secured debt bankruptcy is defined as the legal process of filing for bankruptcy when you carry debts backed by collateral, such as a home, car, or boat. The creditor holds a lien on that asset, which means they retain the right to repossess or foreclose even after your bankruptcy case closes. Unlike unsecured debt, where a creditor has no claim to specific property, secured debt ties the loan directly to an asset. That distinction changes everything about how bankruptcy treats the obligation. Knowing the difference between secured and unsecured debt is the first step toward making a sound decision about which bankruptcy chapter fits your situation.

What is secured debt bankruptcy and how does it work?

Secured debt is a loan backed by collateral that a creditor can repossess if you stop making payments. The collateral creates a lien, which is a legal claim attached to the property itself. That lien does not disappear just because you file for bankruptcy.

The most common secured debts include:

- Mortgages: Your home secures the loan. If you default, the lender can foreclose.

- Auto loans: The vehicle is the collateral. Missed payments lead to repossession.

- Boat and RV loans: Financed recreational property works the same way as a car loan.

- Secured personal loans: Some lenders accept savings accounts or other assets as collateral.

Secured creditors are paid first from collateral proceeds before unsecured creditors receive anything. That legal priority explains why mortgage lenders and auto lenders hold so much power in bankruptcy proceedings. Unsecured creditors, such as credit card companies, stand at the back of the line and often collect little or nothing in a Chapter 7 case.

How does Chapter 7 bankruptcy treat secured debts?

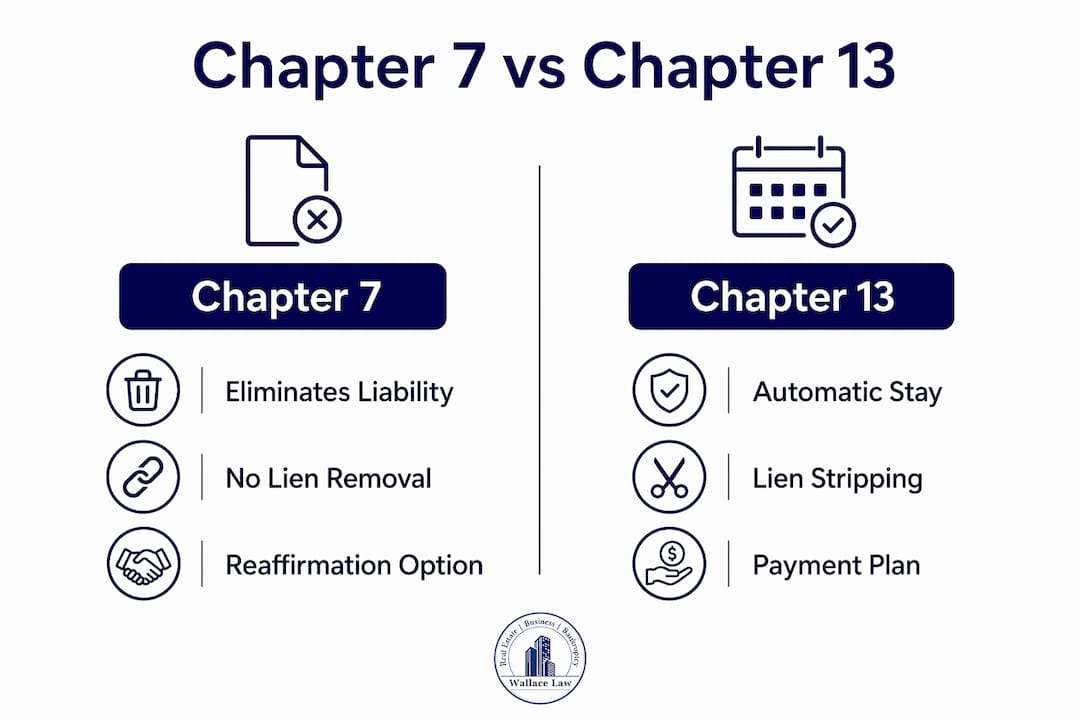

Chapter 7 eliminates your personal liability for most debts, but it does not erase the lien on secured property. That is the single most important fact to understand about Chapter 7 and secured loans. The creditor can still enforce the lien after your discharge if you do nothing about it.

You have three options for each secured debt in Chapter 7:

- Reaffirmation: You sign a new agreement to keep paying the debt under the original terms. The lender keeps the lien, and you keep the asset. If you later default, the lender can repossess and potentially sue you for any remaining balance.

- Redemption: You pay the creditor a lump sum equal to the current market value of the collateral, not the full loan balance. This works well when you owe more than the asset is worth, but you must have the cash available.

- Surrender: You give the property back to the creditor. Your personal liability disappears with your discharge, and you walk away without owing anything further.

Each option carries strict deadlines set by the bankruptcy court. Missing a deadline can forfeit your right to keep the property or limit your negotiating position. Timely decisions on reaffirmation are not optional. Courts and creditors move quickly once a case is filed.

Pro Tip: If your car is worth significantly less than what you owe, redemption can save you thousands of dollars. You pay the car’s current market value in one lump sum and own it free and clear. Many debtors overlook this option because they assume they cannot raise the funds, but redemption lenders exist specifically for this purpose.

Reaffirmation is the most common path for debtors who want to keep their home or vehicle and can afford the payments. Surrender suits those who are underwater on an asset and want a clean break. Redemption is the least used option but can be the most financially efficient when the numbers work in your favor.

How does Chapter 13 bankruptcy differ in treating secured debts?

Chapter 13 gives you a structured path to keep secured property even when you are behind on payments. The 3–5 year repayment plan lets you catch up on mortgage arrears or car loan arrears while staying current going forward. That protection against foreclosure and repossession is the defining advantage of Chapter 13 over Chapter 7 for debtors with secured debt problems.

Chapter 13 offers several specific benefits for secured debts:

- Arrearage curing: You spread past-due amounts across your repayment plan, making them manageable without losing the asset.

- Foreclosure protection: As long as you make plan payments, the automatic stay prevents the lender from proceeding with foreclosure.

- Cramdown: For certain secured debts other than primary mortgages, you can reduce the loan balance to the asset’s current market value.

- Lien stripping: If a junior mortgage (a second or third mortgage) is completely underwater, meaning the home’s value does not cover even the first mortgage, Chapter 13 can strip that lien and reclassify it as unsecured debt. That unsecured balance gets discharged at the end of your plan.

Lien stripping is unavailable in Chapter 7. It is one of the most powerful tools in Chapter 13 and a major reason why debtors with multiple mortgages on a property that has dropped in value should consider Chapter 13 seriously.

| Feature | Chapter 7 | Chapter 13 |

|---|---|---|

| Eliminates personal liability | Yes | Yes, after plan completion |

| Removes liens automatically | No | No, but lien stripping is available |

| Allows arrearage curing | No | Yes |

| Prevents foreclosure long-term | No | Yes, with consistent payments |

| Lien stripping for junior mortgages | Not available | Available |

Chapter 13 suits debtors who are behind on secured payments and want to keep their home or other major assets. Chapter 7 suits those who are current on secured payments and simply want to discharge unsecured debt, or those who are ready to surrender secured property and start over.

What practical steps should you take to manage secured debts in bankruptcy?

The most critical step is making a decision about each secured asset before your bankruptcy case progresses. Waiting too long removes options. Courts impose deadlines, and creditors are not required to remind you of them.

Pro Tip: List every secured debt before you meet with your attorney. Write down the asset, the current market value, the loan balance, and whether you are current on payments. That one page of information will shape your entire bankruptcy strategy.

Key steps to protect your position:

- Calculate equity carefully. If your home has significant equity, surrendering it in Chapter 7 could mean the trustee sells it to pay creditors. Florida exemptions protect a portion of that equity, but knowing the numbers matters before you file.

- Negotiate reaffirmation terms. Lenders sometimes accept modified terms during reaffirmation, including lower interest rates or reduced balances. You have more leverage than most debtors realize.

- Understand the impact on your credit. A reaffirmed debt continues to appear on your credit report, which means on-time payments after bankruptcy can help rebuild your score faster.

- Consult a qualified bankruptcy attorney early. The bankruptcy process involves deadlines, exemption calculations, and creditor negotiations that are difficult to manage without legal guidance.

Missing a reaffirmation deadline in Chapter 7 typically means the lender can repossess the property even if you are current on payments. That outcome surprises many debtors who assumed staying current was enough. It is not. The legal paperwork must be filed on time.

What are common misconceptions about secured debt and bankruptcy liens?

The most widespread misconception is that bankruptcy erases all debts, including the lien on secured property. Liens survive discharge unless you take specific steps to address them. Debtors who do nothing about a secured debt during bankruptcy often face repossession months after their case closes, even though they believed the debt was gone.

A few other myths worth correcting:

- “I can keep my car without reaffirming.” Some courts allow this under a “ride-through” approach, but Florida courts generally require formal reaffirmation or redemption to retain secured property.

- “Chapter 7 can strip my second mortgage.” It cannot. Lien stripping of underwater junior mortgages is a Chapter 13 tool only.

- “My lender cannot contact me after discharge.” Lenders can still enforce the lien on the property. They cannot pursue you personally for the debt, but they can foreclose or repossess the collateral.

A lien is not a personal obligation. It is a legal claim attached to the property itself. Bankruptcy eliminates your personal liability for the debt, but the lien travels with the asset until it is paid, stripped, or otherwise resolved through the court.

The Uniform Commercial Code sets three requirements for a valid secured lien: value must be given, the borrower must have rights in the collateral, and a signed security agreement must exist. If any of those elements is missing, the lien may be challenged in bankruptcy court. That is a nuance most debtors never explore, but it can matter in cases involving informal loans or disputed collateral.

Key Takeaways

Secured debt bankruptcy requires active decisions about each collateralized asset because liens survive discharge and creditors retain repossession rights unless you reaffirm, redeem, or surrender the property.

| Point | Details |

|---|---|

| Liens survive discharge | Filing bankruptcy eliminates personal liability but does not remove the creditor’s lien from the asset. |

| Chapter 7 offers three paths | Reaffirmation, redemption, and surrender each carry strict court deadlines that must be met. |

| Chapter 13 protects assets | A 3–5 year repayment plan lets you cure arrears and stop foreclosure while keeping secured property. |

| Lien stripping is Chapter 13 only | Underwater junior mortgages can be reclassified as unsecured debt and discharged, but only in Chapter 13. |

| Early legal advice is critical | Exemption calculations, equity analysis, and reaffirmation negotiations require qualified legal guidance before filing. |

What I’ve learned after years of watching debtors handle secured debt in bankruptcy

Most debtors come in focused on the wrong question. They want to know if bankruptcy will “get rid of” their mortgage or car loan. The real question is what they want to do with the asset and whether they can afford to keep it. That reframe changes the entire conversation.

The debtors who struggle most are the ones who wait. They file at the last minute, miss reaffirmation deadlines, and then lose a car they could have kept with a simple agreement. Chapter 13 is consistently underused by people who are behind on their home payments. They assume they cannot afford a repayment plan, but the math often works out better than they expect, especially when lien stripping removes a second mortgage entirely.

I have also seen debtors reaffirm debts they should have surrendered. Keeping an underwater vehicle at a high interest rate because of emotional attachment is a financial mistake that follows people for years. Bankruptcy is one of the few moments where you get to make a clean, strategic choice. Use it deliberately.

The Chapter 7 versus Chapter 13 decision is rarely obvious when secured debts are involved. Anyone with a mortgage in arrears, a second lien, or significant equity in an asset should get a full analysis before filing. The difference between the right chapter and the wrong one can be tens of thousands of dollars.

— Steven

How Wallacelawflorida can help you handle secured debt in bankruptcy

Wallacelawflorida works with individuals across Boynton Beach and surrounding Florida communities who are managing secured debts through bankruptcy. The firm handles reaffirmation negotiations, lien analysis, and Chapter 13 repayment plan structuring with the kind of personal attention that larger firms rarely offer.

Whether you are trying to save your home through a Chapter 13 plan or deciding whether to surrender a vehicle in Chapter 7, the attorneys at Wallacelawflorida give you a clear picture of your options before you commit to anything. You can access local bankruptcy legal help or download the free Florida bankruptcy eBook to get oriented before your first consultation. Wallacelawflorida’s goal is to make sure you walk into bankruptcy court with a plan, not a guess.

FAQ

What is secured debt in bankruptcy?

Secured debt is a loan tied to collateral, such as a home or car, that gives the creditor a lien on the asset. In bankruptcy, that lien survives discharge unless you reaffirm, redeem, or surrender the property.

Does Chapter 7 bankruptcy remove liens on secured property?

Chapter 7 eliminates your personal liability for the debt but does not remove the lien. The creditor retains the right to repossess or foreclose unless you take formal action through reaffirmation or redemption.

Can Chapter 13 bankruptcy stop foreclosure?

Yes. Chapter 13’s repayment plan halts foreclosure through the automatic stay and lets you cure mortgage arrears over 3–5 years, provided you keep up with plan payments going forward.

What is lien stripping in Chapter 13?

Lien stripping allows a completely underwater junior mortgage to be reclassified as unsecured debt and discharged at the end of your repayment plan. This option is not available in Chapter 7.

What happens if I miss a reaffirmation deadline in Chapter 7?

Missing the reaffirmation deadline typically allows the creditor to repossess the secured asset even if your payments are current. Courts require the formal agreement to be filed on time, regardless of payment history.