TL;DR:

- Bankruptcy exemptions shield specific property assets from creditor claims, with most Chapter 7 cases retaining all assets. Choosing between federal and state exemptions depends on residency and asset types, affecting protection limits. Properly calculating net equity and avoiding transfers before filing are essential to protect property effectively.

Bankruptcy exemptions protecting assets are legal safeguards defined under federal and state law that shield your equity in specific property from creditor claims during bankruptcy. Under Chapter 7, 96% of cases result in no asset liquidation at all. That number reflects how powerful exemptions are when applied correctly. Your home, vehicle, retirement accounts, and household goods can all survive bankruptcy intact. The key is knowing which exemptions apply to you, how to calculate your equity accurately, and how to avoid the mistakes that cost debtors their property.

How do bankruptcy exemptions work: federal vs. state options?

The U.S. bankruptcy system gives you two sets of exemptions to choose from: the federal scheme under 11 U.S.C. § 522(d) and your state’s own exemption list. You must pick one set entirely. Mixing exemptions from both systems is not allowed.

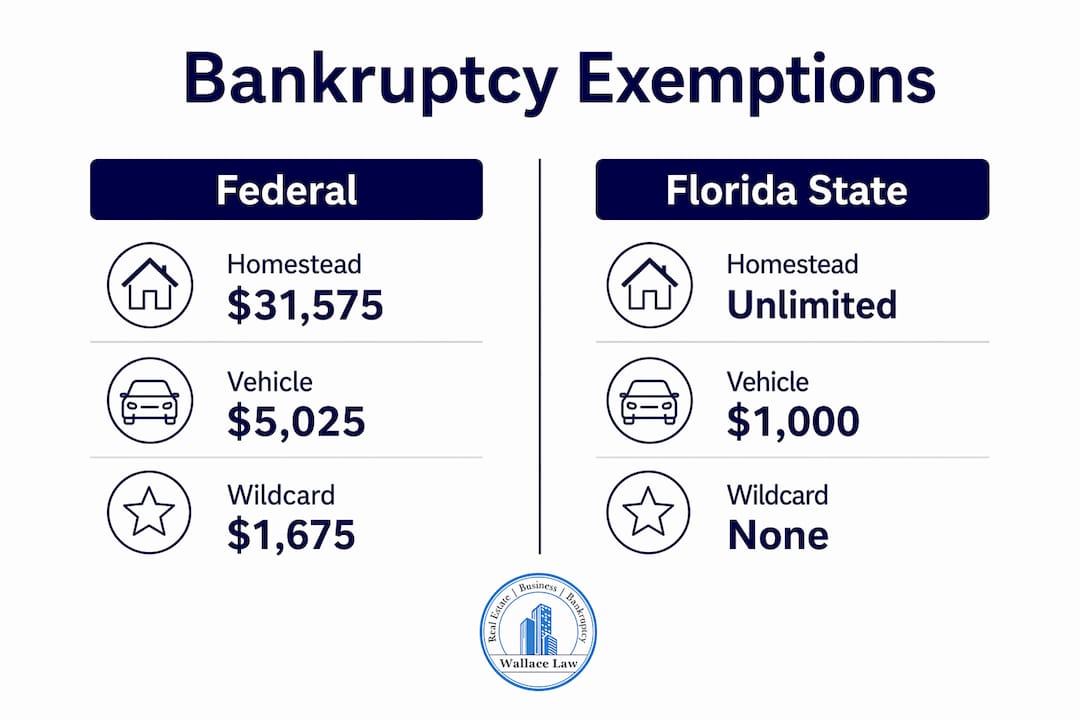

The federal scheme sets specific dollar caps. The federal homestead exemption covers up to $31,575 in home equity. Vehicle equity protection reaches up to $5,025. These federal limits adjust every three years for inflation, with the most recent update in april 2025.

Two-thirds of states require filers to use state exemptions instead of the federal scheme. Florida is one of those states. That matters because state exemptions vary dramatically. Texas and Florida offer unlimited homestead protection by dollar amount, though both states impose acreage and residency requirements. Other states cap homestead protection at a few thousand dollars.

| Exemption type | Federal limit | Florida example |

|---|---|---|

| Homestead equity | $31,575 | Unlimited (with residency rules) |

| Vehicle equity | $5,025 | $1,000 |

| Retirement accounts | Fully protected (ERISA) | Fully protected |

| Wildcard | $1,675 + unused homestead | $4,000 (non-homestead) |

The right choice depends on where you live and what assets you hold. Florida filers with significant home equity almost always benefit from the state scheme. Filers with little home equity but other assets may find the federal wildcard more useful.

Pro Tip: Check how long you have lived in your current state before filing. Federal law requires you to have lived there for at least 730 days to use that state’s exemptions. If you moved recently, a different state’s rules may apply.

How do you calculate equity to apply exemptions correctly?

Exemptions apply to your net equity, not the gross value of your property. Equity equals market value minus any secured liens such as mortgages or car loans. Getting this calculation wrong is one of the most common errors filers make.

A concrete example makes this clear. A home worth $200,000 with a $175,000 mortgage carries only $25,000 in equity. That $25,000 is the figure your exemption must cover, not the full $200,000. The same logic applies to vehicles, boats, and any other secured property.

Here is what you need to document before filing:

- Current market value: Get a recent appraisal or use comparable sales data for real estate. Use Kelley Blue Book or a dealer quote for vehicles.

- Outstanding loan balances: Pull payoff statements, not just monthly statements, since payoff amounts differ.

- Other liens: Include tax liens, judgment liens, and second mortgages in your calculation.

- Net equity figure: Subtract all liens from market value. This is the number your exemption must cover.

Trustees use their own valuations, and those sometimes run higher than what filers expect. Documenting your numbers with third-party evidence gives you a defensible position if a trustee challenges your figures.

Pro Tip: For real estate, a licensed appraisal dated within 90 days of filing carries the most weight with trustees. For vehicles, print and save the valuation page from a recognized pricing guide on the day you file.

What assets can you protect, and how do you do it?

Protecting specific asset categories requires matching each asset to the right exemption. The process is methodical, not automatic.

Homestead equity

Florida’s homestead exemption is one of the strongest in the country. It covers unlimited equity in your primary residence, subject to acreage limits: up to half an acre inside a municipality and up to 160 acres outside one. You must have owned the property and used it as your primary home. Recent buyers face an additional rule: if you acquired your home within 1,215 days of filing, your homestead exemption caps at $189,050 under federal law, regardless of state rules. Wallacelawflorida regularly helps clients in Boynton Beach and surrounding areas confirm their homestead eligibility before filing. You can also read more about protecting home equity to understand how this works in practice.

Vehicle equity

Florida’s vehicle exemption covers up to $1,000 in equity. If you use the federal scheme, that rises to $5,025. Filers who own two vehicles should apply the exemption to the one with the higher equity, since only one vehicle exemption applies per filer. If your vehicle equity exceeds the cap, the trustee can sell it, pay off the loan, return your exemption amount, and keep the rest.

Retirement accounts

401(k)s and pensions under ERISA receive full protection with no dollar cap. IRAs and Roth IRAs are protected up to $1,711,975 per person as of 2026. This is one area where most filers have nothing to worry about. Do not withdraw retirement funds to pay debts before filing. That converts a fully protected asset into unprotected cash.

Household goods and personal property

Federal and state exemptions both cover household furnishings, clothing, appliances, and personal items, though dollar limits apply per item and in aggregate. The federal scheme allows up to $700 per individual item in household goods. Jewelry has its own cap of $1,875 under federal rules.

Wildcard exemptions

The federal wildcard covers $1,675 plus any unused portion of the homestead exemption. This flexibility lets you protect cash, a second vehicle, or other property that does not fit neatly into named categories. Florida’s non-homestead wildcard covers up to $4,000 for filers who do not claim the homestead exemption.

| Asset category | Federal exemption | Florida exemption |

|---|---|---|

| Home equity | $31,575 | Unlimited (residency rules apply) |

| Vehicle | $5,025 | $1,000 |

| Retirement (IRA) | $1,711,975 cap | Fully protected |

| Household goods | $700 per item | $1,000 per item |

| Wildcard | $1,675 + unused homestead | $4,000 (non-homestead filers) |

What mistakes can cost you your assets in bankruptcy?

The most damaging errors in exemption planning are predictable. Knowing them in advance gives you a real advantage.

- Confusing total value with equity. Filers who list a $30,000 car and assume it exceeds the exemption often miss that a $26,000 loan leaves only $4,000 in equity, which the federal exemption covers entirely.

- Transferring assets before filing. Moving property to a family member or paying off a relative’s debt within two years of filing can trigger a fraudulent transfer claim. Trustees have broad authority to reverse these transactions.

- Waiting too long to plan. Last-minute exemption planning raises red flags with trustees and courts. Proactive planning, done months before filing, is both legal and effective.

- Ignoring state-specific rules. Florida’s homestead exemption has residency and acreage requirements that catch filers off guard. The Florida-specific exemption rules differ enough from federal defaults that assuming they are the same is a costly mistake.

- Skipping legal consultation. Exemption law intersects with fraudulent transfer law, state property law, and federal bankruptcy code. Getting this wrong without an attorney is a real risk.

“Exemption planning is not about hiding assets. It is about understanding what the law already protects and making sure you claim every dollar of protection you are entitled to. The debtors who lose property are usually the ones who did not know what they had the right to keep.”

For filers navigating property division alongside financial stress, consulting a property division attorney before filing can clarify how marital assets interact with bankruptcy exemptions.

Key Takeaways

Bankruptcy exemptions protect your equity in specific assets, and 96% of Chapter 7 filers keep all their property when exemptions are applied correctly.

| Point | Details |

|---|---|

| Exemptions cover equity, not value | Calculate net equity by subtracting all liens from market value before applying any exemption. |

| Federal vs. state choice is binding | You must choose one full exemption scheme; two-thirds of states, including Florida, require state exemptions. |

| Retirement accounts are largely safe | ERISA-covered plans have no dollar cap; IRAs are protected up to $1,711,975 per person in 2026. |

| Wildcard exemptions add flexibility | Use the federal wildcard to protect cash or assets that do not fit named exemption categories. |

| Timing and transfers matter | Asset transfers within two years of filing can be reversed by a trustee as fraudulent conveyances. |

What I have learned from watching debtors plan their exemptions

The single most common mistake I see is treating bankruptcy exemptions as a last resort rather than a planning tool. Clients come in days before they intend to file, having already moved money around or paid off family members, and then expect exemptions to clean up the mess. They cannot. Exemption law rewards people who understand the rules early and act within them.

The second thing I have noticed is that filers consistently underestimate what they are already entitled to keep. Florida’s unlimited homestead protection is genuinely powerful. Retirement accounts are almost always fully protected. Most household property falls within exemption limits. The Chapter 7 filing process is not designed to strip you of everything. It is designed to give you a fresh start while protecting what you need to live and work.

My strongest advice: start the conversation with a qualified bankruptcy attorney at least three to six months before you plan to file. That window gives you time to document valuations, understand your state’s rules, and make legitimate decisions about your assets. Combining exemptions with broader asset protection strategies such as entity structures or trusts works best when done well in advance, not under pressure.

— Steven

Wallacelawflorida: protecting your assets through bankruptcy

Wallacelawflorida serves individuals and families in Boynton Beach and across South Florida who need clear, experienced guidance on bankruptcy asset protection. The firm builds customized exemption strategies based on your specific assets, your state’s rules, and your financial goals.

Every client situation is different. A filer with significant home equity needs a different approach than one with retirement savings and minimal property. Wallacelawflorida takes the time to understand your full picture before recommending a path. If you are weighing your options and want to know exactly what you can keep, schedule a consultation with the team at Wallacelawflorida. You can also download the free bankruptcy eBook to build your foundational knowledge before your first meeting.

FAQ

What does a bankruptcy exemption actually protect?

A bankruptcy exemption protects your net equity in specific property from being liquidated by a trustee. Exemptions cover assets such as your home, vehicle, retirement accounts, and household goods up to defined dollar limits.

Can I keep my house if I file for Chapter 7 bankruptcy?

Yes, if your home equity falls within your applicable homestead exemption. Florida offers unlimited homestead protection for primary residences, subject to acreage and residency requirements, making it one of the strongest protections available.

What happens to assets that exceed exemption limits?

A trustee can sell the asset, pay off any secured loan, return your exemption amount to you, and distribute the remaining proceeds to creditors. Filers rarely lose property because most equity falls within exemption limits.

Are retirement accounts protected in bankruptcy?

401(k)s and ERISA-covered pensions are fully protected with no dollar cap. IRAs and Roth IRAs are protected up to $1,711,975 per person as of 2026.

What is a wildcard exemption and when should I use it?

A wildcard exemption lets you protect property that does not fit into named categories like homestead or vehicle. The federal wildcard covers $1,675 plus any unused portion of the homestead exemption, making it useful for protecting cash or a second vehicle.