TL;DR:

- Most people fear losing all assets, but Chapter 7 bankruptcy often protects property while eliminating debts. The process involves filing, a court-appointed trustee reviewing assets, and a discharge typically within three to four months. Exemptions and priority of creditors determine what is kept and how assets are distributed during liquidation.

Most people assume that filing for bankruptcy means handing over everything they own. That fear stops many from getting the debt relief they genuinely need. Understanding how the bankruptcy liquidation process works reveals a very different picture. The formal term is Chapter 7 bankruptcy, and it’s built around a structured legal framework that protects many of your assets while eliminating qualifying debts. Knowing what a trustee actually does, which property you can keep, and how creditors get paid gives you real control over the outcome before you ever walk into a courtroom.

Table of Contents

- Key Takeaways

- How the bankruptcy liquidation process works step by step

- Exempt vs. nonexempt assets explained

- How creditors get paid during liquidation

- Chapter 7 vs. Chapter 13: choosing the right path

- Practical steps to prepare for liquidation

- My perspective on what most people get wrong

- How Wallacelawflorida can help you move forward

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Most cases are no-asset cases | Many filers keep all property because exemptions cover everything they own, with no assets sold. |

| Trustees manage the process | A court-appointed trustee reviews your finances, holds a creditor meeting, and handles any asset sales. |

| Creditors are paid by priority | Secured creditors collect first from asset proceeds; unsecured creditors receive whatever remains. |

| Chapter 7 has income limits | You must pass a means test to qualify, based on your income relative to your state’s median. |

| Discharge takes 3 to 4 months | Most straightforward Chapter 7 cases conclude with a discharge within 90 to 120 days of filing. |

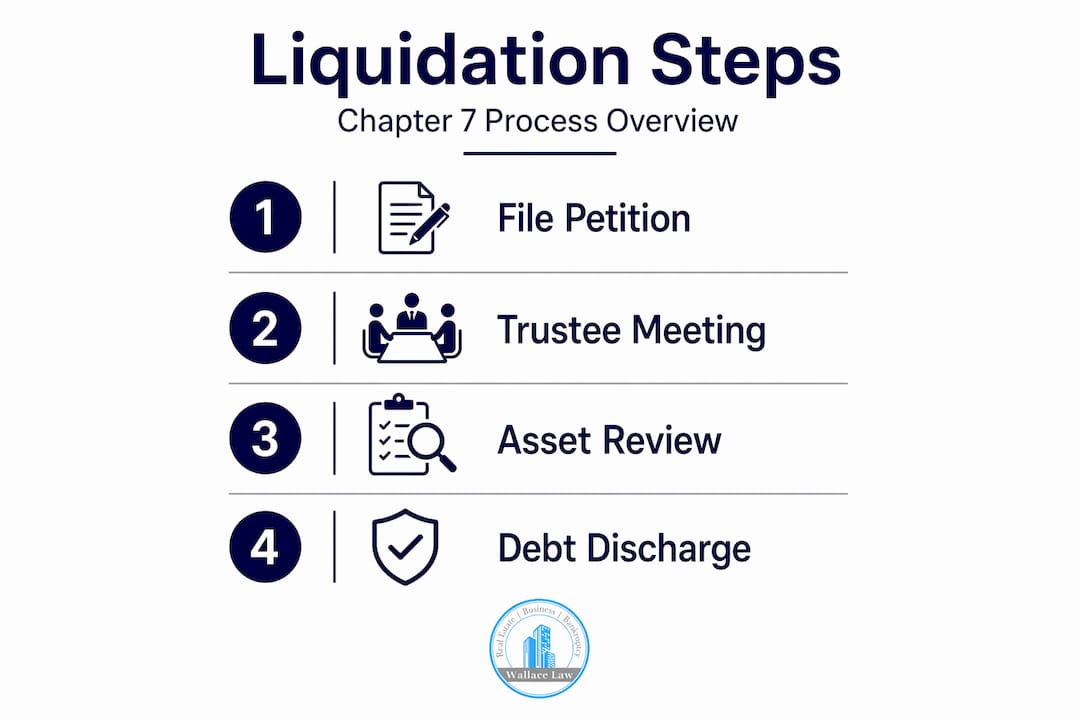

How the bankruptcy liquidation process works step by step

Chapter 7 bankruptcy is the most common form of consumer liquidation in the United States. The IRS describes Chapter 7 as providing liquidation relief for debtors who cannot make regular payments, with a trustee converting eligible assets into cash for creditor distribution. Here is exactly how that unfolds.

Step 1: Filing the petition

You file a bankruptcy petition with the federal bankruptcy court in your district. This filing includes detailed schedules of your assets, liabilities, income, and expenses. The moment you file, an automatic stay goes into effect. That means creditors must immediately stop all collection calls, lawsuits, wage garnishments, and foreclosure actions. The automatic stay alone provides significant breathing room while your case is processed.

Step 2: Trustee appointment and the 341 meeting

A bankruptcy trustee is assigned to your case almost immediately. The trustee’s job is to review your financial documents, identify any nonexempt assets, and distribute proceeds to creditors. Trustees hold a creditor meeting roughly 20 to 40 days after you file. This is called the 341 meeting, named after the section of the bankruptcy code that requires it. It typically lasts 10 to 15 minutes. The trustee asks questions under oath about your finances, and creditors may attend but rarely do in consumer cases.

Step 3: Asset review and liquidation

After the 341 meeting, the trustee determines whether you have any nonexempt property worth selling. If all your property falls within exemption limits, your case is classified as a no-asset case and moves directly toward discharge. If nonexempt assets exist, the trustee sells them and distributes the proceeds to creditors according to legal priority.

Step 4: Debtor education and discharge

Before your debts are wiped out, you must complete a debtor education course, which is mandatory and covers personal financial management. You submit your completion certificate to the court, and the discharge order follows. That order legally eliminates your personal liability for qualifying debts.

Pro Tip: File your debtor education certificate as soon as you complete the course. Delays in submitting this document are one of the most common reasons discharge gets pushed back unnecessarily.

The full stages of Chapter 7 bankruptcy are worth reviewing in detail before you file, because knowing what comes next reduces anxiety at every step.

Exempt vs. nonexempt assets explained

This is where bankruptcy liquidation explained in simple terms makes the biggest practical difference. Not all of your property is up for grabs. Federal and state laws carve out specific categories of assets that creditors and trustees cannot touch.

What you can typically keep

Common exempt property includes a portion of your home equity, your primary vehicle up to a set value, household goods and furnishings, clothing, tools of your trade, and qualified retirement accounts. Florida, where Wallacelawflorida operates, has particularly strong homestead exemptions that can protect your primary residence entirely regardless of its value, provided you meet residency requirements.

Here is a quick comparison of how exempt and nonexempt property differ in practice:

| Property Type | Exempt? | What Happens |

|---|---|---|

| Primary home (Florida homestead) | Yes, often fully | Protected from trustee sale |

| Retirement accounts (401k, IRA) | Yes | Cannot be liquidated |

| Second vehicle above exemption limit | No | Trustee may sell it |

| Investment property | No | Subject to trustee sale |

| Jewelry above exemption threshold | No | May be sold for creditor payment |

Most Chapter 7 cases are no-asset cases because filers’ property falls entirely within exemption limits. The trustee closes these cases without selling anything.

How liens complicate the picture

Exemptions protect equity, not the full value of property with a lien attached. If you own a car worth $8,000 but owe $6,000 on it, your equity is $2,000. If your state exemption covers $2,500 in vehicle equity, you keep the car. But if you owe nothing on a $10,000 car and your exemption only covers $2,500, the trustee could sell it and give you $2,500 while distributing the rest to creditors. Accurate exemption claims and asset scheduling are what protect you from losing property you could have kept.

Pro Tip: Never underestimate the value of your personal property when filing schedules. Trustees are experienced at spotting undervalued assets, and inaccurate filings can trigger legal complications far worse than the original debt.

How creditors get paid during liquidation

Understanding the payment hierarchy answers a question most filers have: will my creditors actually come after me during this process?

The legal priority order

Bankruptcy law sets a strict sequence for distributing asset proceeds. Secured creditors come first because their loans are backed by collateral. If you default on a car loan, the lender has a lien on the vehicle. The trustee must satisfy that lien before any other creditor sees a dollar from that asset’s sale.

After secured creditors, the law recognizes several tiers of priority unsecured creditors. These include domestic support obligations like child support and alimony, certain taxes owed to the government, and wages owed to employees in business cases. Trustees follow this structured priority framework, which means general unsecured creditors, such as credit card companies and medical providers, often receive little or nothing.

| Creditor Type | Priority Level | Typical Recovery |

|---|---|---|

| Secured creditors (lien holders) | Highest | Collateral value or proceeds |

| Domestic support (child support, alimony) | Second | Paid from remaining proceeds |

| Government tax claims | Third | Paid before general unsecured |

| General unsecured creditors | Lowest | Often partial or zero recovery |

Dischargeable vs. non-dischargeable debts

A bankruptcy discharge eliminates your personal liability for many qualifying debts, but some obligations survive bankruptcy entirely. Student loans, recent tax debts, child support, alimony, and debts from fraud cannot be discharged. This distinction matters enormously when you are deciding whether Chapter 7 will actually solve your financial problem or only part of it.

Chapter 7 vs. Chapter 13: choosing the right path

Liquidation is not the only option, and choosing between Chapter 7 and Chapter 13 depends on your income, the assets you want to keep, and the type of debt you carry.

| Factor | Chapter 7 Liquidation | Chapter 13 Repayment |

|---|---|---|

| Income requirement | Must pass means test | No income cap, but needs regular income |

| Asset retention | Nonexempt assets may be sold | Keep assets while repaying over 3 to 5 years |

| Timeline to discharge | 3 to 4 months | 3 to 5 years |

| Best for | Low income, few assets, unsecured debt | Higher income, assets to protect, mortgage arrears |

The means test is the gateway to Chapter 7. Your average monthly income over the six months before filing is compared to your state’s median income. If you fall below the median, you qualify automatically. If you exceed it, a more detailed calculation of your disposable income determines eligibility. People who do not qualify for Chapter 7 often find that Chapter 13 in Florida gives them a structured way to catch up on mortgage payments while keeping their home.

Practical steps to prepare for liquidation

Preparation separates people who sail through Chapter 7 from those who face delays, asset disputes, or worse.

- Gather every financial document you own. This means bank statements, tax returns for the past two years, pay stubs, vehicle titles, mortgage statements, and a complete list of all creditors with balances owed.

- List every asset at fair market value, not replacement cost. A three-year-old laptop is worth what you could sell it for today, not what it cost new. Trustees know the difference.

- Research your state’s exemptions before filing. Florida’s exemptions are generous in some areas and strict in others. Knowing where you stand before you file lets you make strategic decisions about timing.

- Attend the 341 meeting prepared. Bring your photo ID and Social Security card. Answer questions honestly and completely. Trustees are not adversaries by default, but they are thorough.

- Complete your credit counseling course before filing. A credit counseling certificate from an approved provider is required before your petition is accepted by the court.

Pro Tip: If you own property with a co-signer or joint owner, their interest in that asset may also be affected by your filing. Discuss this with an attorney before you file, not after.

How Chapter 7 bankruptcies work in practice involves more nuance than most online summaries suggest. Getting the details right from the start protects both your assets and your timeline.

My perspective on what most people get wrong

I’ve worked with individuals at every stage of financial distress, and the single biggest mistake I see is waiting too long to understand the process. People spend months dreading bankruptcy without ever learning what it actually does to their lives. When they finally sit down and look at the numbers, they realize that most of what they feared losing is protected.

What I’ve found is that exemption planning is where cases are won or lost before they even begin. The law gives you tools. If you don’t know those tools exist, you can’t use them. I’ve seen clients surrender property they legally could have kept simply because no one explained the exemption schedules clearly enough before filing.

The trustee relationship also matters more than people expect. Trustees are not out to punish you. They have a legal job to do, and when you show up with complete, accurate documentation, that job goes smoothly for everyone. Incomplete schedules, on the other hand, invite scrutiny and delay.

My honest take: bankruptcy is not a failure. It’s a legal tool that Congress created specifically for people in financial distress. Used correctly, with realistic expectations and proper preparation, it genuinely does what it promises. It gives you a fresh start. The people who struggle most after bankruptcy are those who never addressed the habits or circumstances that created the debt. The discharge is the beginning, not the end.

— Steven

How Wallacelawflorida can help you move forward

If you are weighing your options and want to understand exactly where you stand before making any decisions, Wallacelawflorida offers personalized legal guidance for individuals facing bankruptcy in Boynton Beach and throughout South Florida.

The attorneys at Wallacelawflorida take the time to review your specific situation, explain your exemption options clearly, and walk you through every step of the process. You can start by downloading the free Florida bankruptcy eBook for a plain-language overview of your rights and options. When you are ready to speak with someone directly, the bankruptcy practice page is the place to start. Real answers from attorneys who know Florida law and treat every client as a person, not a case number.

FAQ

What is bankruptcy liquidation in simple terms?

Bankruptcy liquidation, formally known as Chapter 7 bankruptcy, is a legal process where a court-appointed trustee reviews your assets, sells any nonexempt property, and distributes the proceeds to creditors before discharging your remaining qualifying debts.

How long does the Chapter 7 liquidation process take?

Most straightforward Chapter 7 cases reach discharge within 90 to 120 days of filing, though disputes over asset exemptions or complex asset situations can extend that timeline.

Will I lose my home in Chapter 7 bankruptcy?

Not necessarily. Florida’s homestead exemption is among the strongest in the country and can fully protect your primary residence, provided you meet the state’s residency requirements and are current on your mortgage.

What debts cannot be eliminated through liquidation bankruptcy?

Debts that survive bankruptcy discharge include child support, alimony, most student loans, recent income taxes, and debts incurred through fraud. A discharge order clears eligible debts but leaves these obligations fully intact.

Do I have to qualify to file Chapter 7?

Yes. You must pass a means test that compares your income to your state’s median. Only individuals who pass the means test qualify for Chapter 7, which prevents higher-income filers from using liquidation when a repayment plan is feasible.